Disclaimer

Based on public information, mostly available in prospectus

All analysis is pre listing (a year back)

Mostly focussed on creative accounting pre/post IPO than on business.

Not having a Position / Not a recommendation

It appeares that Blackstone acquired IGI primarily to capitalize on the IPO wave rather than for long‑term strategic ownership.

The company was founded by the Lorie family in Belgium in 1975, with its India division likely established in 1999. In 2018, the majority stake (80%) was sold to China’s Fosun Group through Alpha Yu Holding, while the Lorie family retained a 20% share. In mid-2023, Blackstone acquired the entire company for approximately USD 569.65 million (₹4673 crore) including the separted and later acquired original divisions of Netherlands and Belgium.

According to the prospectus, the India division, along with its Turkish subsidiary, was valued at ₹3328 crore, with the payments split 80:20 between Fosun Group and the Lorie family. The remaining ₹1446 crore was allocated to operations held through IGI in the Netherlands and Belgium. Over the 15 months since acquiring IGI (India), Blackstone has taken out around ₹217 crore in dividends from the Indian subsidiary (Pre IPO).

Blackstone appeared to have readied the group for an IPO by emphasizing headline accounting growth and structuring exits by listing divisions rather than the entire company at once. The India entity proceeded with an IPO comprising an offer for sale and a “fresh issue.” However, the “fresh” proceeds were primarily earmarked for acquiring IGI Netherlands and IGI Belgium from the promoter group, which were separate before IPO, effectively routing IPO funds back to the promoter.

If the prices go high, They are likely to exit with a much high payout . It seems like a major win for them. That’s how you make money out of bubble, if you are as big as blackstone.

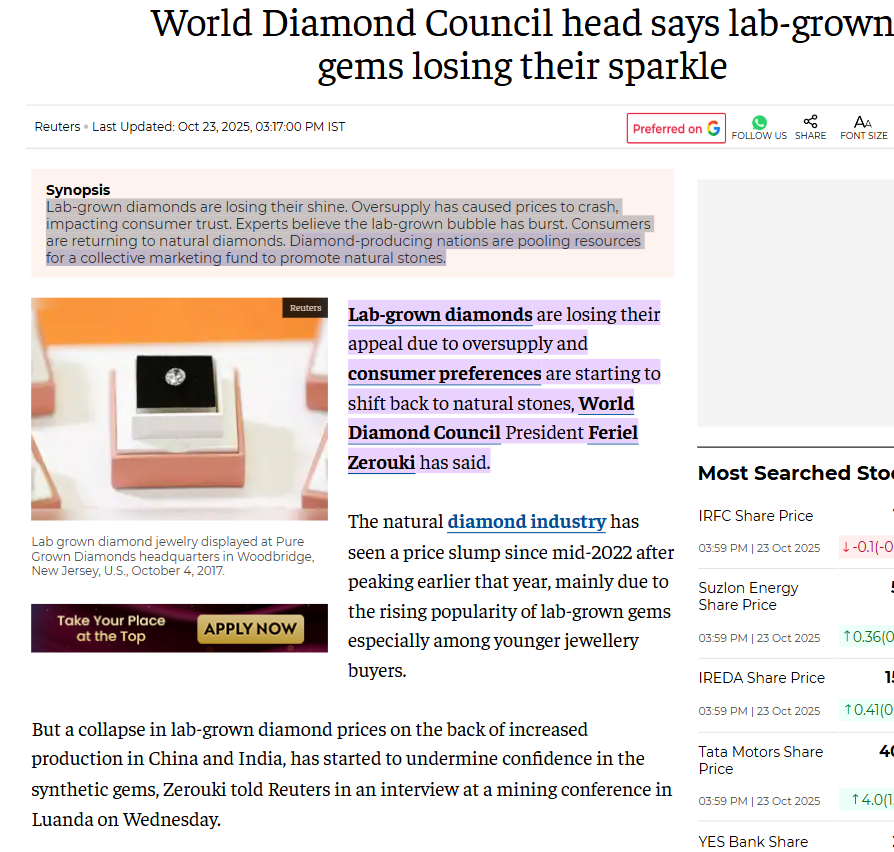

Diamond industry growth has been primarily dependend on exports to US/Europe and it was already struggling for multiple reasons including but not limited to slowdowns, restrictions on russian origin diamonds etc, and the problems accelerated with Trump Tariffs.

In summary,

acquire a European entity with India subsidiary, separate the India subsidiary and list at very high valuation given the mania in name of growth, acquire the rest of company by Indian subsidiary to show high growth for a year or two (depending on how it is structured) and make a handsome profit because Indian investors (including institutional ones) were/are ready to pay any price in name of growth. Basically Blackstone bought 76% of company for free.

It also begs the question, how a business becomes worth multiple times just because you list in India, without any signficant real improvement. How did something worth ₹ 3228 Crore became worth ₹ 16546 Crore (@417 per share), or even worth more (if taking listing/post listing prices) after taking out 217 crore as dividend in one year only? [There is another embedded assumption that Fosum group sold the belgian (original) company at fair price given they are also a big PE invester]

Blackstone acquistion accounting split

| Entity |

Total Consideration (U.S.$ M) |

Total Consideration (₹ Crore) |

| IGI (India) |

393.45 |

3228.05 |

| IGI Netherlands and IGI Belgium |

176.20 |

1445.64 |

| Total |

569.65 |

4673.69 |