There is a time for equity and a time for bonds. Both have a role to play.

IDFC First raised equity at Rs. 57.35. Today the share price is much lower which would mean more dilution. Tier 2 bonds will enable the bank to shore up total capital ratio which will in turn help it to grow the loan book and still meet the capital adequacy requirements.

HDFC Bank is trading at a higher P/B (4) compared to IDFCFB (1.5) . When you dilute the shares at a higher value, it is good for the existing shareholders as the book value of the share also increases. This concept is well explained by SOIC in their video on IDFCFB. Please watch it. So, when market starts to give good valuation to IDFCFB, the bank may think of diluting equity. As of now, they can raise tier-II at 8.42% that too 10 year bonds which is a very good move btw.

It makes no sense for a bank to dilute equity at 0.5-0.6 P/BV. If a bank is raising capital that way, it is not good for the existing shareholders. Please don’t compare the borrowings with Tier-II bonds. Both are entirely different.

Raising equity is necessary only when loan growth rate is higher than ROE of bank.

Amount of equity raise per year required is = (Loan growth per year-ROE per year).

In this case capital adequacy remains constant with time.

Equity raise can be partly by dilution and partly by raise of tier-2 bonds.

Guidance given by VV on ROE is 16-17 %.

In last two years ROE was negative and hence large dilution of the bank took place.

If one is confident that the share price would go up because the return ratios are on the rise, one would want equity dilution at a higher price only. Moreover there is call option for the Tier-II bonds at the end of 5 years and every year from there on.

At the end of five years let us assume the price doubles from the CMP (conservative in my opinion) and the bank manages to raise equity at double the CMP, and uses the call option for the bonds. You do the math and tell me which option is better. This is the conservative case.

In the best case scenario…if the bank delivers on its guidances and delivers ROE> 15% and ROA> 2% and keeps growing loan book at 20% which means double the existing loan book size, the share would be a multibagger.

Therefore, many of the existing shareholders don’t want dilution now. Raise Tier-II bonds upto the maximum limit and raise equity when share price goes up. This is like a leverage as far as shareholders are concerned.

Latest news is that IDFCF bank has pushed up the ‘normal interest’ ceiling of 2 crores deposit in the savings account and made it 100 crores ie 5% saving rate is available upto 100 crores. It is a clear attempt to increase the CASA at the cost of diluting their earlier policy of removing the concentration of high deposits. They seem to have reached the conclusion that at this stage, the bank can manage the volatility caused by sudden movement of these funds moving in or out. I agree. The larger the size of CASA pool, the more would be its ability to withstand large withdrawals.

The issue of tier 2 bonds also gets explained. At least I think so.

It also sends the signal that the bank is now moving seriously into expanding their loan book and branch utilisation.

One of the reason for raising tier-2 now can be that they they can raise issue equity if the reverse merger with IDFC materializes. Hence focus on tier-2 today and raise equity by issuing shares during reverse merger

What a badly written article, whole street and their uncle knows that the sale process for the AMC is underway and four bidders have been shortlisted with the final buyer expected to be announced next month. RM process will speed up once that is out of the way. UTI AMC is nowhere in the picture and if you see their latest AR they dont have the funds to be able to buy IDFC even if they were interested!

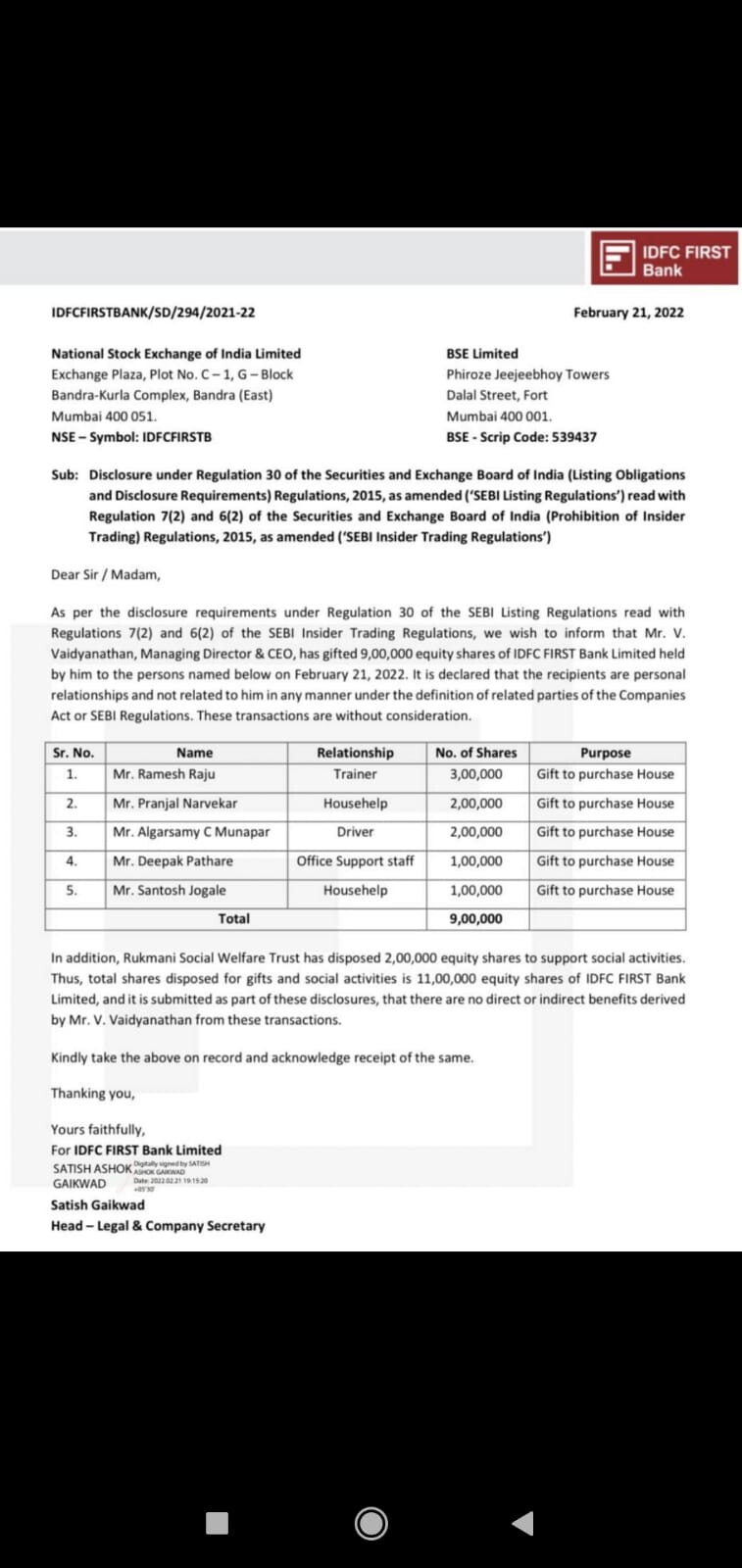

Gifting them shares is tax effective for both VV and the gift recipients.

The recipients have to pay income tax at their peak tax slabs in case of both cash and shares (not LTCG but as “income from other sources”).

So from the recipient side the tax implication is same.

However for VV, if he liquidates his shares he has to pay LTCG which may be quite high (last time when he sold his ESOPs he said it got liquidated close to his acquired price of 15 or some price closer to that). So he has to pay 10% of (43 - 15) per share as LTCG.

So I feel what VV has done is the right thing to do. Why pay govt LTCG when that amount can be passed on to his workers without any further tax implications.

I respect Mr V V and his Charity, but my question is why he always gives in form of equity ? Earlier also he gave some equity to his teacher. Aa per my knowledge he has 0.39 % equity.

Note - i am not against any charity or good thing. But I cannot decide whether it is good or bad.

Please experts discuss this. As this is confusing.

I think he has clarified this in the annual general meeting, the only form of wealth he holds is Equity apart from the regular salary he earns which is enough to run his house, also has a housing loan for which he needs to pay EMI.