Tier 2 bonds are best way for IDFC first bank to raise capital at this stage as their cost of capital is 8.42% and the reason why I am making this statement are as follows.

8.42% is almost same as Capital First Cost of borrowing.

This 1500 crores is considered as equity for lending purposes hence growth can be funded through this.

This 1500 crores is not considered as core equity and hence ZERO dilution in share holding as ZERO new shares issued.

This 1500 crores will help bank to leverage upto 5-7 times which will earn an incremental NIM of 6% which means it will add approximately 275 crores of profit annually including credit cost to the PPOP with ZERO dilution.

This additional capital will add approximately 1.25% additional ROE to the core equity shareholders every year.

The flip side is that if the credit quality deteriorates more than the NIMs it will have exactly opposite effect to ROEs.

this is a pretty good interview. Normally, TV anchors ask generic questions without understanding the company.

Interviewer here was quite thorough. There wasn’t much new for anyone on this forum. Only take away for me was company thinks 16-17% will terminal ROE.

Another small new info : current credit card book is 5 lakh. Looking to expand that to 2m to 3m in near term. Mostly cross selling to existing customers.

For growth of 19- 20% per year with ROE 16-17% dilution of the bank for current shareholders per year will be 2 -3 %. If this dilution happens at 3 to 4 times of book value, it will be great for current shareholders.

Disc: Invested at average price of 30/- rs.

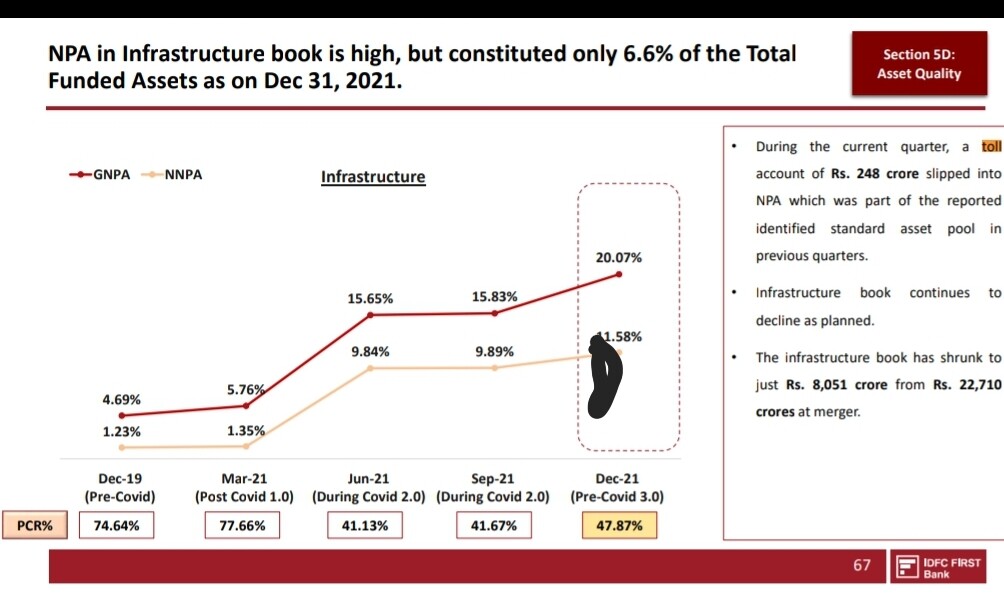

Regarding both toll accounts what they have said is that they expect to recover full money & not incur any economic losses. We have to see whether that happens as economy continues to open up. Investors should probably ask questions about both these toll roads in upcoming calls.

Btw many of these toll roads put up their monthly collections & the money they Re paying back debtors so this part of the pie should be easy to track & analyse.

We have to monitor these accounts like a hawk. When economy specially travel & transport has not picked up yet, it’s not unexpected to see the toll account still remaining NPA

Btw, it is not like these accounts are not paying. Rbi guidelines mean that unless they pay back whatever is due to the banker, they remain an NPA.

Supposing my emi is 100 rupees. I miss 3 of them due to COVID stress. I need to pay back 300 rupees + interest on it + all emi due until date for me to stop being an NPA & become a regular account.

It’ll take time for toll booths to comeback to that level of liquidity. These accounts don’t carry a lot of risk of impacting the terminal value of the bank Imo.

I am not able to understand something. The logic behind Tier2 bonds @8.42%. On one hand in the IP, the bank keeps saying legacy bonds have high interest rates and again they are issuing bonds. Why not just increase the savings interest to say 7% and attract more CASA? CASA is not counted as part of the CRAR? Is that the reason?

But growth capital can come with these kind of deposits than say bonds right?

I know that collecting 2000Cr via CASA will take time say a quarter or sth, but still I am not able to understand this Tier2 bond issue

The bank should now focus more on cost to income ratio. They seem to have got over bulk of the expenses on branch expansion and tech backbone. Perhaps only more hiring may be needed. They should go slow on new expansions for now and concentrate on improving utilisation. This would improve cost to income ratio, pushing up the share price which would give them head room for additional resources. The drop in the share price seems to be the biggest problem. It would certainly affect negotiations on the merger ratio. VV becomes visibly uncomfortable when he is asked a question about the merger . Maybe my perception is incorrect.

Rbi has written down tier 2 bonds in LVB. had requested yes bank to not pay interest to tier 2 bond holders.

In today’s Day a banks ability to raise tier 2 bonds shows that it is able to win trust of the bond market.

The alternative to raising tier 2 bonds is to raise equity. Equity is generally considered to be costliest form of funding since the ownership of bank is permanently diluted.

You can borrow more against tier 2 bonds.

When calculating capital adequacy tier 2 bonds & equity are taken as sort of “banks own capital”. Due to the risks associated tier 2 bonds are always going to be priced high BUT enable higher borrowing of the primary kind.

Raising 2k cr tier 2 bonds enables bank to raise say 15k to 16k cr more casa as an example & use it to lend

It is not an to comparison to compare tier 2 bonds with casa. Right comparison is with equity which is a permanent dilution of ownership.

175% liquidity coverage ratio is a statement about the here & now. The raising of tier 2 bonds is a statement about the future. In all interview now a guidance of 20% aum growth has been given. That means around 24k incremental loans to be given in next 1 year. For that 24k incremental loans they require around 3k to 3.5k cr of “capital” that bank owns (generally idfc first has been Levered around 7 to 8 times) in order to not dilute the capital adequacy ratio.

This 3k cr could have been through equity dilution which would have meant permanently 15% lower ownership of bank for all of us. If you think about it, cost of equity is around 15-18%. Instead of that bank was able to raise tier 2 bonds at 8.4%. This will enable future lending against the bonds.

There should be more than what your explanation is. Why should someone like HDFC bank raise via issuing shares than just Tier-2. Would HDFC bank be able to get Tier-2 more easier than idfc first? I can be sure it will be the case

Any bank will consider raising via shares vs raising via Tier-2. In this particular case how is it more advantageous is what needs to be discussed. You always ask me to read previous posts and one generic explanation. I would be happy to discuss a case in point with proper dissection