here is the recording of the concall…

.

https://drive.google.com/file/d/1ja_4cKtUNIRasP805jKZCGH5akt1mh-w/view?usp=drivesdk

6 Likes

One more important point. At the end of concall, Vaidyanathan sir made a statement that the bank is expected not to post any loss in the future. The operating profit will be more than the credit cost as there are no more issues expected from the legacy book. This is a huge statement.

17 Likes

Made 3-4 epic statements during the call:

“Barring any unfortunate account, our bank is set to never make any losses from here on out”

“We are at an inflection point, either you believe us now, believe us tomorrow, or believe us after 4 quarters, but believe us you will”

“Revising credit cost guidance to 1.5%”

“Cost to income will start declining from here on out”

Let’s see whether they can walk the talk. Until now the have imo.

33 Likes

Investors like me holding their breath since Q1 FY22 results, can finally let go and breathe out. Hopefully the new Q3 NPA and the previous one of Q1 will turn out to be benign and go away without causing much damage. There is no reason to disbelieve the management’s assessment. In fact one can only empathise with them as they have faced the discovery of a continuous string of nasty, well hidden NPAs. Apparently there is nothing left on the canvas now, to discover. Next feature to cross will be the reverse merger. I am sure VV and team have got sufficient experience by now to do proper due diligence to ensure that there are no further unpleasant discoveries in the shape of legal and financial issues. I don’t know how open/assertive the management can be in dealing with a shareholder and promoter, holding 37%.

Scaling up the loan book, liabilities, card operations etc should gradually position the bank to a decent position within the next 2 to 3 years. The execution performance of this management has been excellent and is a very good reason to feel confident. Investment thesis remains intact although slightly delayed. First reason of delay is inadequate ‘due diligence’ at the time of merger and the second is the emergence of Covid crisis. Those wanting to exit should be able to do so with respectable returns after another 2 years.

Disc : Highest Investment.

12 Likes

IDFCFB seems to be very comfortable on the liability front. They invested considerable amount in the opening of new branches, ATMs etc to raise liabilities. As per the bank, they are making a loss of 325-350 cr loss every quarter on retail liabilities business segment. Even the Op-ex for the bank increased 30% yoy (quarterly basis) and 41% yoy (9M basis). All these investments enabled them to raise deposits as and when they want.

However, the irony is that the bank doesn’t want to increase deposits in the short term. They have 17,567 cr of cash and bank balances with RBI which is earning low yields I.e even lower than the interest they pay on deposits. This shows that the loan book size has not kept up with liabilities.

The bank needs to increase the size of the loan book and particularly the retail component. Although the bank managed to grow its retail assets at 25% CAGR, the decrease in wholesale loan book has offset it . The ticket size for the home loans is larger and time period is longer. This should probably help grow the retail book quickly. Also the bank is willing to lend to corporates when they find an opportunity. Hope they put more efforts in this direction. Even the credit card business is gaining momentum which should help. It is to be noted that the bank recently proposed to issue 2000 cr of Tier 2 bonds which also indicates that they are ready to grow their loan book size.

Since the legacy loan book issue is behind us, growth in loan book (retail/corporate), reduction in opex are the key monitorables for me going ahead.

Disc: Invested and biased.

9 Likes

Overall the results seem good esp the GNPA and NNPA of retail+consumer and Corporate numbers are good. Infra seems to be going to hang around for some more time. The infra loan book being <7% is good.But the GNPA has now jumped to 20% because of the one toll road project. The good immediately reducible infra book is all cleared up I guess. The not so good ones will be around for some more time. Any worst case estimates on the provision coverage for this was discussed in the call?

@sahil_vi How much is the funded and non-funded exposure to VI now? Any ideas. other than VI what is the total non-funded exposure and whom is it?

1 Like

Hi @sahil_vi,

These results really looks good and i think in next 3 to 5 yrs this stock should get re rated. Just one thing keep coming in my mind that after struggling with vi so much they have again given 500 cr to vi again in same month. Isn’t this one kind of ever greening ? Wanted to ask this in concall but did not got chance.

Disc: Invested and highest allocation.

2 Likes

- The situation is different now than it was 4 months ago. They would not have lent to the vi of the past but this vi got equity infusion form government of India & it’s promoters.

- The exposure now is 1/4th of the earlier one.

- Banks are part of consortium and i think to some extent have to take on such risk in the broader context of being a bank.

- Key will be to lend in proportion to net worth. Which they are doing now i think.

Is this a move that i love ? Absolutely not. From concall it felt like they had to do it, and didn’t have too much of a choice.

9 Likes

I started studying IDFC First Bank a few days back. I have kind of a basic question about the bank, would appreciate an answer to this please.

IDFC First has a cost of funds greater than 6% (Maybe closer to 6.8%) due to legacy borrowings which are at 8%+. It still manages to earn NIM of 5-6%.

Banks like HDFC, Kotak and ICICI have cost of funds < 4% but still make NIMs between 4-5%. ICICI and Kotak’s retail loan book %s are comparable to IDFC First’s at around 60%. So how does IDFC First manage to earn higher interests on their loans while ensuring asset quality?

Thanks to all contributors in this thread for providing so much information and commentary on the smallest of details regarding the bank. Really helps new entrants get up to speed!

11 Likes

Lenders work on the law of large numbers. The aim is not to make money on each & very loan. The aim is to model cohorts of lendees & charge each cohort based on 2 aspects :

- The opex of the loan (some loans are inherently higher cost structure. Eg : business loans, gold loans. Compared to home loans which are lower opex. Since, once you give a home loan the customer is tied up for 15-30 years & thus after front ending of the costs, the interest income is back ended.

- The credit loss of the lendee cohort. Again, experience in lending enables lender to model each cohort for credit losses.

This modelling of opex costs & credit losses enables lenders to price loans appropriately. The question you are asking has indeed been asked 10000 times on this thread. Answer is very simple :

- Each lender has its inclusion & exclusion criterion. Each of them has its own catchment area. They decide to operate in certain sections and NOT operate in others. This exclusion criteria creates opportunities for their peers. If i decide not to lend below the age of 25 then my competitor can make a buisness model operating in that niche.

- Entire banking system is the organized part of credit system. They are not competing against themselves but rather against the unorganised lending. Informal lending. Sahukaar & loan sharks. Ones giving 50% interest rate & 200% interest rate. So the 14% might seem like a lot, but no, it isn’t. In fact you have answered your question on your own. That high interest rate enables the bank to operate even with high credit costs. THAT IS the business model. In a function economy, everyone needs credit. You need credit. Your driver & your house help also need credit of course the rate of interest is not the same for both of you. While kotak bank might make money lending to you. There is still space left for others to lend to your driver & house help & make money as long as the credit risk is priced correctly.

I consider the duration of lending operations as an important competitive advantage in lending. For evaluating the bank, you need to read the capital first vp thread first since that is the management in control of the lending now. You need to see their yields their credit costs, their cost to income ratios & ask yourself whether there is a business model there or not.

Finally, Lookng at the average cost of funds is a misleading way to interpret & evaluate the bank. While the average is 6.8% what one needs to appreciate is 2 things :

- This average contains the high cost of funds like 8-9% borrowings. These are what were used to fund the high yield higher risk lendee. But there is a business model here. This is what Bajaj finance & capital first have proven to us.

- This average ALSO contains the casa funds which currently are costing the bank around 4.5% or lower (15% ca and 85% sa with sa rate of 5%). This 4.5% cost funds can be used to do prime home loan lending. Even at 7% roi bank can still make tons of money because home loans are low opex low default product.

If you go through the presentation you will see that the incremental risk taken by the bank has been going down over time. If you go through the thread (feel free to only go through my posts if reading all the 1900 seems to be too much work) you’ll also see that the % of loan book which is focussed on mfi has been going down steadily. Being replaced by safer lending areas like consumer finance (this is the main reason Bajaj finance has done well) & mortgages (home loans & loan against properties).

At end of the day, evaluating a lender canot be done by reading the numbers. We must evaluate the management & their conservatieness by evaluating their actions in times of stress. By evaluating how they treat NPA recognition. By evaluating to what extent they are able to walk the talk. By all of those metrics, my invested & biased self finds this to be a conservative bank. Whether a bank is conservative or not does not depend on the gross yields. It depends on little actions in recognising stress early, in provisioning on time. In recognising pain instead of sweeping it under a carpet. Which bank was the 1st to call out Vodafone Idea as a stress ? Which bank was the 1st to provide provisions for vodafone even at the cost of totally demolishing their own P&L.

Do your own due diligence & make up your own mind. Conviction canot be borrowed. It must be earned individually by studying a good selection of banks deeply & making up your own mind.

52 Likes

Where did you get cost of funds at 6.8%?? In an earlier call VV had mentioned its below 5% now, do check your numbers.

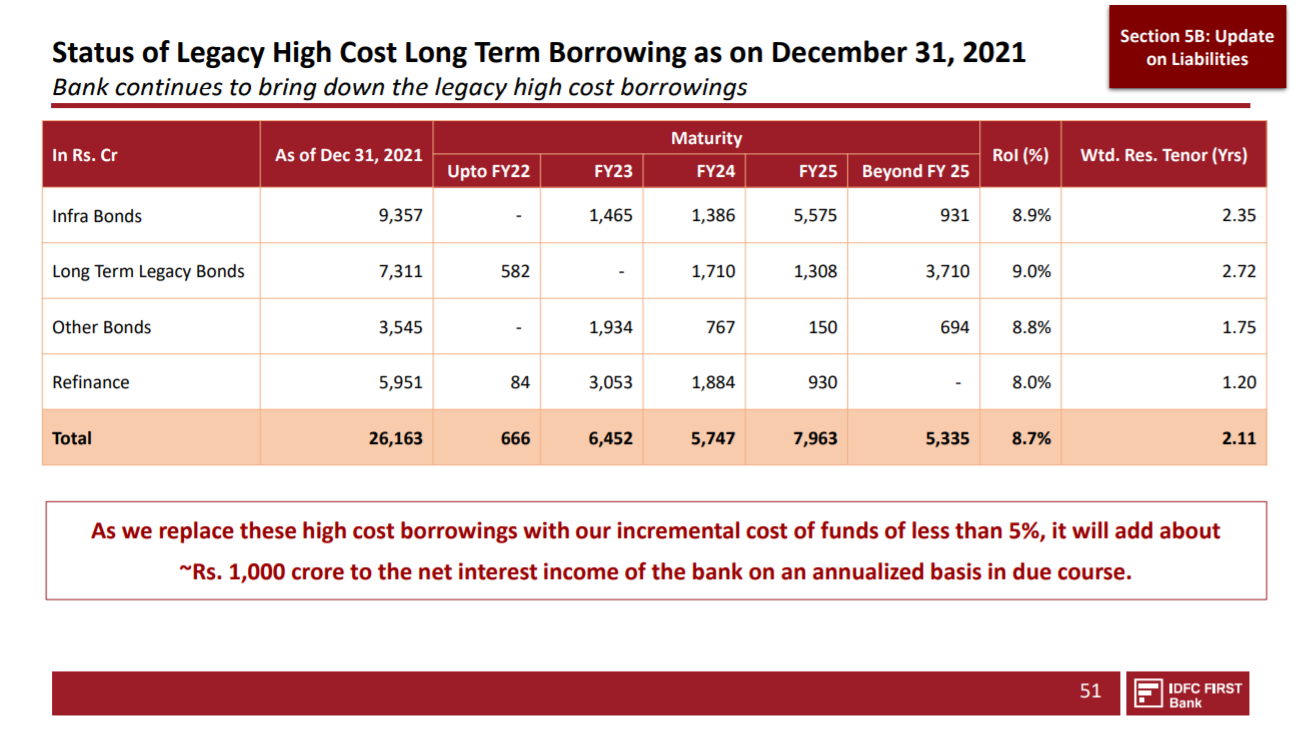

The 5% number you are mentioning is for incremental borrowings. But they are carrying 26000 Cr of legacy debt which is at 8.7% (which they hope to retire within 3 years). The blended cost of funds is likely to be around 5.7-6% (Assuming 26000 Cr at 8.7% and balance 117000Cr at 5%).

6.8% might be an inaccurate calculation on my part (I was considering 26kCr at 8.7% and 50kCr of deposits at 5% for a total of 86kCr; But I realize the additional borrowings of 58kCr on their balance sheet via Refinance, Other borrowings, Certificate of deposits and money market borrowings are also likely to be at 5% as per Management commentary)

Attaching relevant screenshots from their Q3 presentation

3 Likes

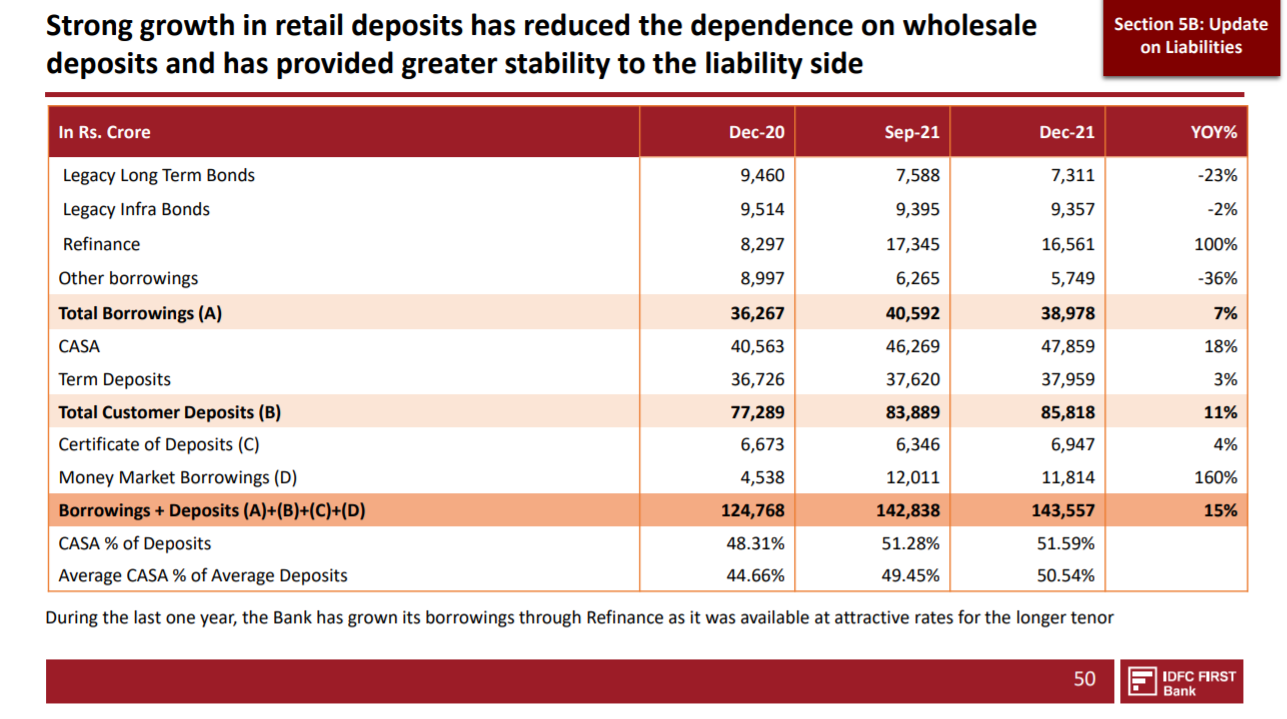

Interest Expended in Q3 is 1,849cr. Total Borrowings + Deposits are 143,557cr. So interest cost for the quarter is 1.28% and if you annunalize this number its 5.1%. That is the current COF for the bank.

8 Likes

There are few points which are slight negative for banks:

- Very high equity i.e. more than 600 Cr

- High Income from treasury or interest from RBI ( Rs 481 Cr in Dec 22 Qtr compared to 214 Cr in Sep 22 Qtr).

- Still Retail banking not showing profit. ( Loss widens to Rs. 187 Cr from 129 Cr. from QoQ)

Since VV intends to make bank a retail bank, so the point to be observed is (i) when retail portion will show turnaround, and quality of earnings will improve.

Disclosure: Invested from lower levels

4 Likes

3 Likes

and

Why the bank needs to raise funds with Tier 2 bonds when they’re not able to utilise the CASA? Is there a asset liability mismatch (ALM) happening?

Disc: Invested; Have SA and credit card with them.

6 Likes

What ever bank lends as per the asset category and in proportion to total asset bank has to keep Tier1(Common Equity) and Tier2 (Debt) so bank keeps raising this capital as per growth of assets.

17,567 cr is money with bank which it uses for lending (to build assets) comes from (CASA, Deposits, CP etc). This is excess with bank so in near term CASA is less required.

I hope difference is clear.

3 Likes

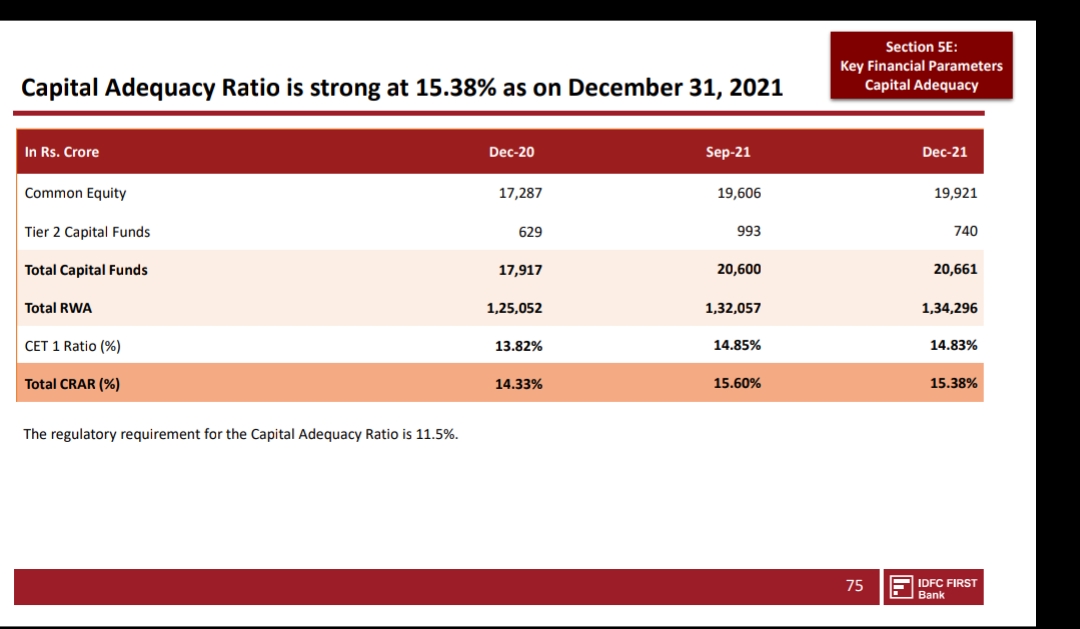

Please refer to the picture above from the presentation.

Banks need to maintain a minimum capital to mitigate the risks and reduce the risk of insolvency as per Basel-III norms. IDFCFB bank at present has a CRAR of 15.38%. The RWA are 1,34,296 cr. Bigger banks such as ICICI and HDFC Bank have a CRAR of around 19%.

The minimum CRAR to be maintained by banks is 11.5%. The max RWA upto which the bank can go with the present capital and maintaining 11.5% CRAR works out to 1,75,660 cr which is only an additional 45,364 cr. However, it is advisable that the bank maintains CRAR above 15%. If the bank raises Tier-1 capital, it would dilute equity.

So raising Tier 2 capital is better in the present situation. I feel that bank would anyway get Tier-1 capital through reverse merger.

CASA is again different which is not the bank’s capital and is only considered as a liability. To lend more the bank has to raise more capital apart from the liabilities.

13 Likes

Economic Times: IDFC First Bank earnings income to grow faster & credit cost to come down this year: V Vaidyanathan.

2 Likes

Key takeaways and my openion from Q3 FY 2022 Results and presentation.

- NIMs at all time high of 5.9% ex of Voda-Idea Interest payment. (6.18% including VODA-Idea Bond).

- Next year provisioning of bank guided at 1.5% with earlier guidance of 2% which is a significant upgrade of 25% reduced Credit cost that will directly hit the bottom like in a positive manner.

- Last 2 quarters Gross NPA and Net NPA went on a downward trend even after two infrastructure accounts slipped into NPA which will have almost no credit loss. Retail Gross and Net NPA guidance of 2% and 1% for next year.

- Vodafone idea Funded exposure reduced from 2000 Crores to 500 odd crores and non funded exposure remains same at 1244 Crores. I am Expecting 75% non-funded exposure to get returned soon and finally will get back 100%.

- Legacy exposure is thing of past as per management and the infra book now is all clean.

- Next Year total loan growth will be 18%-20% and retail will about 25%, but with raising capital in form of tier 2 bonds in tune of 2000 crores they seem to be understating growth as per my opinion.

- Core Operating profits excluding any trading gains reached approximately 745 crores which is more than adequate to cover credit loss and in normal course of business is an infliction point as per my assessment.

- This quarter had 100 Crore odd of interest income of Voda-Idea bond so numbers should be adjusted accordingly and ex of that Core operating profits increased almost 13% Q-o-Q and with the 100 crores it is 30% Q-o-Q growth. I expect the rate to be between 8-12% rise each normalized quarter.

- IDFC First bank credit cards are one of the most preferred cards as per spends per card and already breached into top 10 within just 1 year of launch.

- They are not heavily looking for deposits as LCR is already high and having negative drag on approximately 7500 Crores of excess liquidity at -1.5% annually which used even for prime home loans can generate additional interest margin of 560 odd crores annually.

- IDFC first bank hasn’t opened even a single additional branch in Q3 2022 indicating they are now rationalising physical expansion and focusing on operational efficiencies like deposit per branch, loan per branch and unit economics as their worry of chunky deposits is solved beyond their own expectations.

- Bulk of branches will mature this year with around 18-24 months in existence and start achieving unit sustainability. I will compare unit economics next quarter when yearly results are presented.

22 Likes