Let’s wait and see on what rationale the management has decided to go ahead with the loan (if any). It’s definitely not fitting with the strategy the bank had previously cited. Specially when they have declared the account as distressed. So let’s get this clarified in the con call.

2 Likes

I think too much has been discussed about the VI exposure in the last 10-15 days. Guys, if you have followed Vaidyanathan from his days at Capital First, you would know the following:

-

There is no scope of evergreening of loans under his lens.

-

Unlike most bankers, he believes in recognizing stress way before the regulatory requirements require him to.

-

In the case of VI, if you do study cashflows of VI after the telecom relief package of Sep, 2021, you will see that if statutory dues are deferred then VI will generate sufficient cashflows to service new loans. The problem was the sudden balloon payment of Rs 6000 cr till March, 2022.

-

I am confident about 2 things here. a) Net-Net IDFC’s exposure would have reduced drastically. b)Even if a certain amount has been lent, it couldn’t have been lent at 6.5-8.5% RoI without the corporate guarantee of the group or personal guarantee of Birla.

In my eyes, the VI issue is behind IDFC First Bank.

17 Likes

IDFCFB used to be Fintech’s darling bank but seems bank is now cutting ties with Fintechs.

May be bank is relying on its own tech and digital initiatives to gain the customer base.

Source : We have carved out fintech partnerships as a new unit: Federal Bank's Warrier

1 Like

Maybe IDFCFB was doing that to acquire more and more customers and maybe now they think they have a good base and grow without much external help

2 Likes

Groww recently started lending through its platform. IDFCFB is Groww’s lending banking partner

6 Likes

All the return ratios, eps, and multiples are skewed negatively because of the toll road provisions and if that account pays back full everything should revert to mean.

Maybe they need to read V.V’s commentary in the FY21 annual report regarding ROE.

IDFCFB is trying to be a retail funded bank.

As per Sep 21 quarterly results

Borrowings : 40,592 Cr

Total customer deposit: 83,889 Cr

1 Like

Just saw news on Zee Business that IL & FS going to return around 55k cr to lenders. Saw this on TV but for reference giving YouTube link

Was there exposure from IDFC First to ILFS in past which they wrote down?

4 Likes

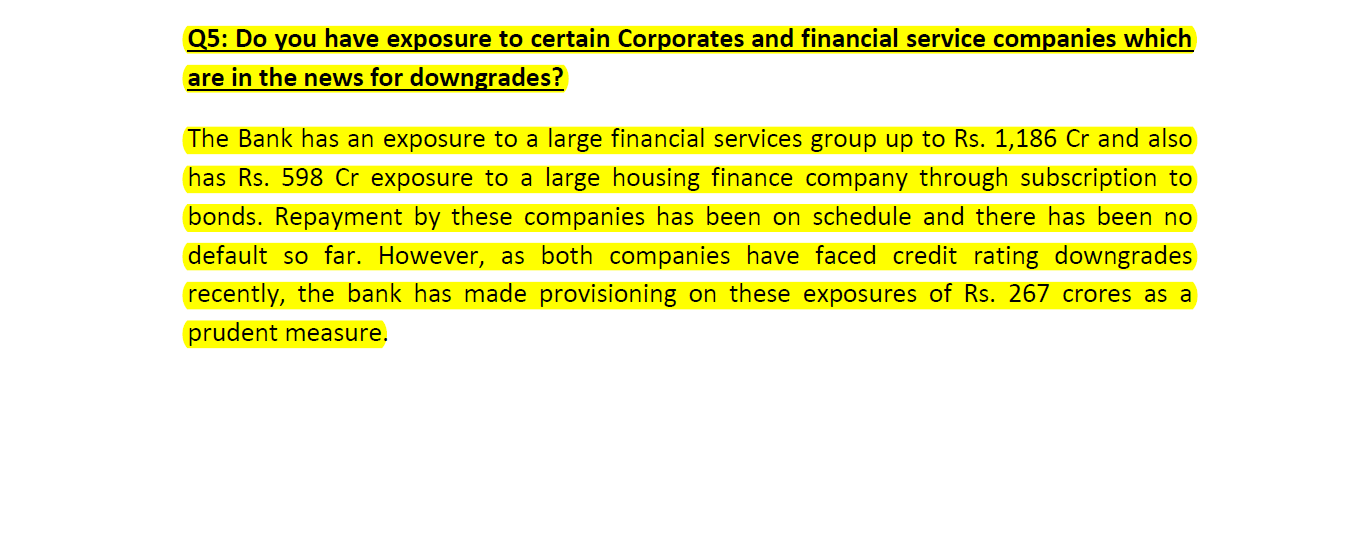

If the large financial group referred here is IL&FS then the exposure was 1186crs.

Bank will pay 61kcrs out of the total 94kcrs ie. recovery of 64-65%.

1 Like

IDFC issuing Tier 2 bonds upto Rs 2,000cr, will be a huge positive if this goes through as it had become very difficult for smaller private banks to raise capital via Tier 2 bonds since the Yes Bank fiasco. Will be a huge vote of confidence for IDFCB from the market while increasing CRAR and reducing immediate need to raise equity funds. Will be interesting to see at what rate these bonds are issued.

8 Likes

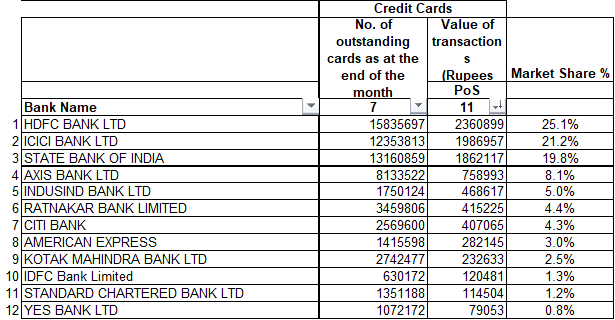

IDFC Bank added 43k Credit cards in Dec and now stands at 6.3lacs Outstanding cards.

7 Likes

IDFCB into the Top-10 this month

8 Likes

This topic is temporarily closed for at least 4 hours due to a large number of community flags.

This topic was automatically opened after 4 hours.

Looks like Vodafone issue sorted.

This statement from press release:

"Provisions were lower by 32% and 17% on a Y-o-Y and Q-o-Q basis respectively at Rs. 392

crore in Q3-FY22 as compared to Rs. 574 crore in Q3-FY21 and Rs. 475 crore in Q2 FY22.

o During Q3 FY 22 and in Jan 22, the bank received Rs. 2,000 crore towards

redemption of bonds pertaining to one large telecom account. The Bank has

released provisions for Rs. 487 crore created against this account.

"Press Release

7 Likes

Concall Notes

- A and above rated exposure is 79% of wholesale (Infra + Corporate). BBB & below is 21%.

- Restructuring is 2.6%.

- Next year we guide for credit loss of 1.5%.

- In CapF we had 2.6-2.7% credit costs on yield of 16%.

- Have taken a fresh exposure of 500cr with VI. Non funded is 1244 cr. Bank guarantee for VI should come up for release. Fresh exposure was taken coz promoters and GoI infusing equity into VI. their fortunes have changed. Would not have taken exposure to older entity but can take it now.

- Cost to income from now on should begin to come down for us.

- Slippages have come down by 25% in current Q.

- SMA as % of book has come down to less than pre-covid level. Except rural book where it has increased due to JLG.

- SA book is becoming more granular.

- Incremental yield for retail book is 14.5%-15%.

- Seeing a pretty healthy increase in spends on credit cards.

- We didnt want more deposits for last few Qs.

- “We are not in league of big 4 but we are close”

- We are seeing for the last 3 months, in JLG the SMA numbers are coming down.

- “We declare results on Saturday because generally lot of info flows back & forth whn finalising results & we feel its safer after the market hours close”

- The 2 infra accounts we are hoping to get the money back. The 500cr VI provision write back was used to strengthen the balance sheet (PCR).

- For liability, we do sourcing through employees & digitally. Dont use DSA.

- Proportion of CA has become 15% of CASA now. It has grown 65% YoY. We see good opportunity for growth.

- 2.6% of the book is restructured.

Disc: Invested, biased

17 Likes

They just informed in concall, IDFC first have taken new exposure of 500 crore on Vodafone and the non funded exposure of 1244 crore should come up for release.

Disc: Invested

1 Like

Thanks for the notes. Would like to add the following points from the investor presentation as these give an idea of what can be expected in the years to come.

- Rs 26163 Cr of legacy bonds (8.7%), when replaced after 2 years with 5% interest, will add Rs. 1000 Cr of net interest income.

- Loss on retail liabilities is about @1000 Cr p.a which will reduce/fade away as the bank ramps up its retail libailities.

- Credit card business loss is about @ 300 Cr p.a which will start reducing as its scales up.

- LCR is @ 149% is a drag on P&L and it will improve in the coming quarters.

Disc: Invested indirectly via IDFC.

4 Likes

Can someone please share link of concall ?