I opened a savings a/c with them about 2 months back and was received very warmly/affectionately at a large branch. An executive visited me in the evening to complete the formalities like PAN card, wife’s signatures etc. I had been reading statements of VV in the media about their desire to slow down CASA , so it was a surprise. And they are following up in a very nice way on the phone, wanting a meeting, obviously desiring to expand the relationship

My interpretation of this anomaly : Perhaps, to stay at the same place, they need to keep moving forward. Market place is like a tread mill. One has to respond accordingly. My confidence in the bank went up and I increased my holding. They have designed their business well. They are implementing it well. The employees appear to be well trained and feel a sense of ownership. I was told that all of them (approx 20+) in the branch own shares purchased from the market. And they expressed confidence in the bank doing well.

Data for everyone to ponder over. IDFC First Bank ranks number 1 in YoY growth for debit cards, ranks 2 for QoQ growth(Inspite of all the interest rate cuts) in debit cards. Other banks which are very aggressive for Savings accounts are Kotak( Rank 2 for YoY and 1 for QoQ) and Yes Bank. Bigger Banks like ICICI and Axis seem to be losing market share.

Was running the YOY comparison and the growth numbers look great for the retail portfolio, even better than Bajaj Finance.

Q2FY21

Q1FY22

Q2FY22

QOQ (%)

YOY (%)

Retail Funded Assets

59,860

73,673

78,830

7%

32%

Housing Loan

10,919

12,120

11%

Mortgage Backed Loans

22,034

26,006

29,404

13%

33%

Mortgage Backed Loans (%)

36.8%

35.3%

37.3%

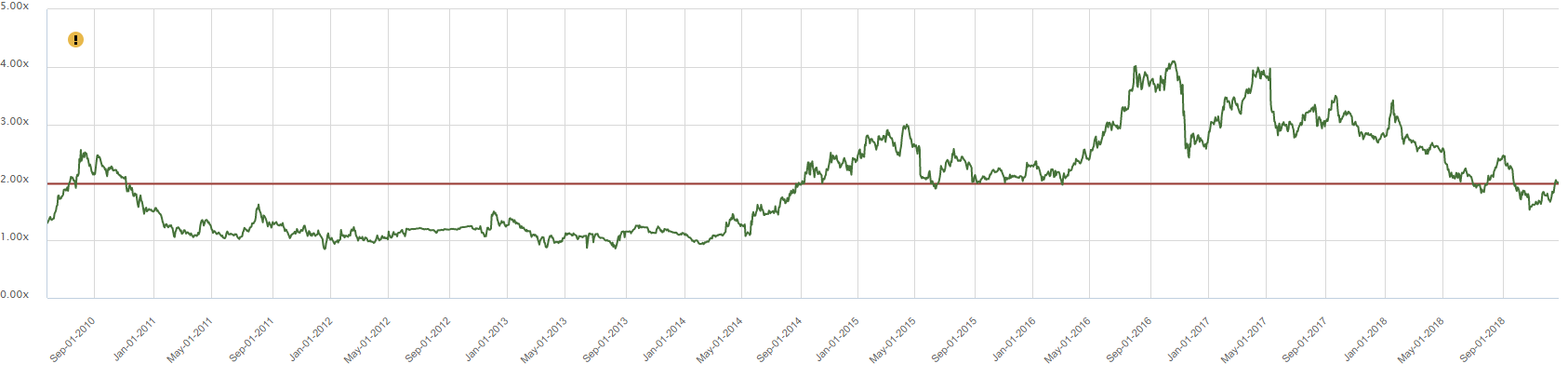

Also went back to check the historical P/B multiple progression vs ROE’s for Capital First (both charts below) and its interesting how closely it mirrors IDFCB. Till FY13 CAPF was loss making and turned profitable FY14 onwards with an ROE of around 5%. P/B multiples between FY11-FY14 were mostly between 1-1.5x. In FY15 CAPF started gaining momentum and had ROE’s of 8% and then 10% in FY16 and 12% in FY17. This was matched by the P/BV which started expanding FY15 onwards and was above 2x and even went upto 4x in FY17-18. Its clear that the P/B re-rating happens much before the ROE starts going up.

One could argue that IDFCB is today at a similar place to where CAPF was in FY15. The bank posted an ROE of 3% in FY21. If PPOP for FY22 turns out to be around 4,500cr (was 1,000cr in Q1) and Credit Cost comes out to 2,700cr (Roughly 2.5% as per mgmt estmates) then PBT will be around 1,800cr and PAT around 1,400cr which implies an ROE of ~7%. Next year as per current guidance/growth projections ROE’s shoud easily be above 10%. IDFCB today is still trading around 1.5x P/BV, so going by historical trends we should see a re-rating of the P/BV multiple soon.

PL is entitled to their opinion. But given that IDFC FB notched up a PPOP of 1kcr in Q1. Can expect QoQ gains in PPOP from here given higher advances to come in subsequent quarters. @Puch has nicely computed the potential ROE for FY22 assuming the credit cost guidance holds.

RedSeer had earlier said that the platforms will clock over $9 billion gross merchandise value (GMV) during the festive season which is a growth of 23 percent from last year.

Further, with easy credit and instant affordability, ‘Buy Now Pay Later’ (BNPL) schemes are likely to account for 10-15% of sales this festive season, said RedSeer. BNPL accounted for 4-7% of sales last year but is well-poised to command a higher share i.e. 10-15% of sales this year, according to the management consultancy.

As far as I know IDFCF is the sole partner on Flipkart Pay Later and one of 2 partners on Amazon Pay Later at this time.

As far as my understanding goes, most people would tend to honor their buy now pay later behavior. This might not be a big revenue stream. Rather, it would provide valuable data on customer behavior which could enable better product (both asset & liability) cross selling in the future. Looks like a ripe area to ask questions to management & better understand this space. Thanks for sharing the article. Will try to frame a question around this & ask in the next concall.

I’m not sure if this is currently practiced in India but BNPL companies do charge a percentage fee to merchants. If this is the case the product would be similar to credit cards.

The play in IDFC First, and emerging private banks altogether, is the imminent transfer of market share from struggling public banks to private space, teamed up with penetration due to digitization. PSU cuts started under UPA 2 and have continued under NDA 2 as well. The process is nearing completion, across sectors, it’s not just banks.

This is something Mukherjea has discussed in his EDGE Community presentation for the financial space. The rationale is pretty simple; IDFC First Bank is well positioned to make great offerings and continue to grow (comfortably) at 25% or more. Big banks have a certain advantage, agreed, but they can’t afford to be as aggressive as banks like IDFC First Bank. They don’t need to. They don’t compete with IDFC First Bank, not yet.

With Vaidyanathan at the helm of affairs, IDFC First Bank will move forward with what can be termed as ‘responsible’ aggression. One can already look at provisioning and ascertain that the bank doesn’t wish to get ahead of itself while trusting its process at the same time. IDFC First Bank investors have a massive risk appetite and they should. Big Bank investors are not the tribe you’ll find here. Anyone without a sizable risk appetite should exit IDFC First Bank since the financial space is never risk averse.

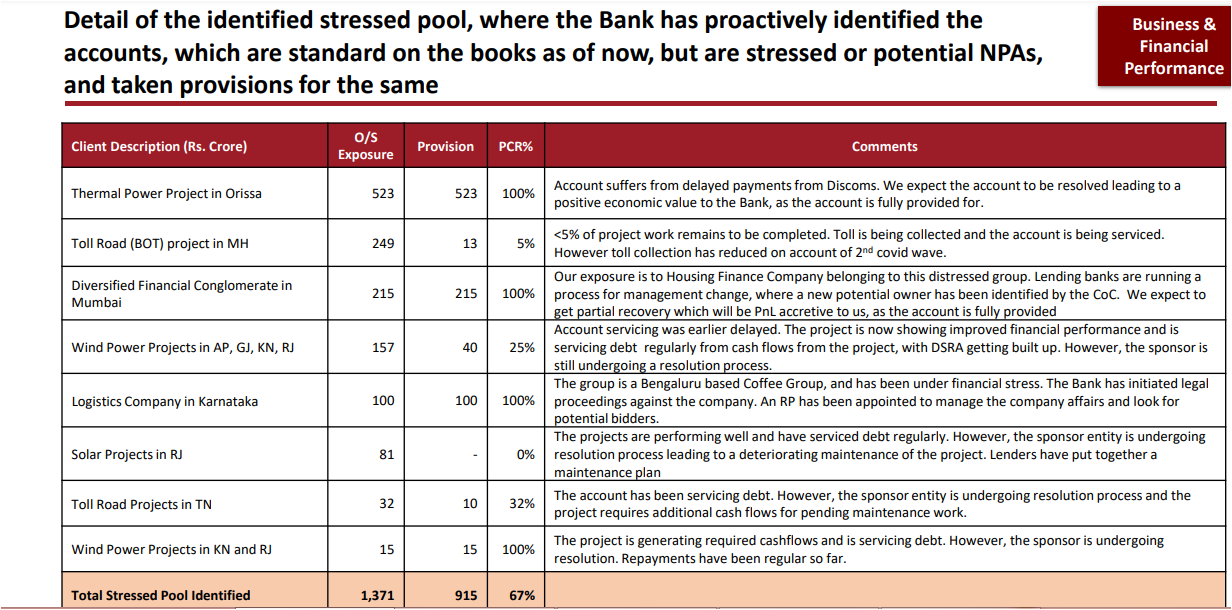

Hello everyone. I’ve been following this thread for almost a year now and this is my first post here. I like the narrative of this bank i.e retailization of assets and liabilities and also the way V.Vaidyanathan is leading IDFC first bank. However, still I’m relatively new to banking stocks and trying to gain competence in evaluating them. I have a basic question. What is the purpose behind giving the details of identified stressed pool in every investor presentation? Are these stressed assets not covered under NPA bucket? If they are not covered, why are they providing for these stressed assets? Are they doing it a part of good corporate governance?

Not part of the NPA provisioning norms legally but the bank is aggressively providing for based on the business analysis. Provisions for identified stressed pools hence could be reversed depending upon changing business dynamics. For eg: i reasonably expect the MH Toll Road provision to be reversed in Q2.

I think mostly stressed assets are not marked as NPA because declaring NPA has negative implications on the borrower. Also, there are various regulation which determine classification into NAp which includes 90 days delinquency, bankruptcy, unlikeliness to pay, sale of credit obligation at material loss, etc etc. However, as a prudent management, a bank should not only declare such assets but also well provided for.

Thank you for the clarification. The identified stressed pool is not part of NPA but it is potential NPA which the bank has identified. This is done only for Wholesale book right. What about retail book?

I think cost to income ratio is operating-expenses/operating-income. I checked HDFCB latest figures and it seems to include all other income to arrive at 37% (someone correct me if I’m wrong). Whereas in the case of IDFCFB if we exclude trading gain in the operating-income it is 77% (2032/2634) but if we include it is 67% (2032/3034), calculated from the above slide.

We are yet to see operating leverage play out for the bank. I think new branch opening has stopped or significantly slowed down. If they don’t start expanding aggressively again we should see improvements in cost-to-income sooner rather than later. Maybe good to check with management about future expansion plans during concall?

CEO had guided for similar level of Cost-to-Income for rest of this financial year during the AGM as operating leverage will take time to play out. They have slowed down branch expansions but still intend to have between 800-900 branches by 2024-25. They now have 600 branches.