While I agree that market cap will very likely increase, what matters to shareholders is price per share increase. Here, it can get tricky if credit costs continue to be high, RoE remains low and bank still wants to grow in double digits. It can only do so by raising capital and diluting shareholders…since merger, share count has gone from 480 cr to 620 cr in 2.5 years. Bank is essentially spinning its wheels at the same place…

1 Like

last quarter PPOP has grown, 12% YoY and 55% QoQ. So, I suppose PPOP is the metric by which we can measure progress. And not eps cuz legacy loan and Covid provisioning makes it murky.

Now, progress in PPOP will continue to come the same way, like it has so far, from reducing wholesale deposits and reducing wholesale loan book.

Wholesale Borrowings are still 38000Cr

Wholesale loan book is 32000Cr.

So there is room to keep reducing them for a couple of quarters and increasing PpOp without need for Equity Dilution.

I remember reading that last Equity Dilution was done to maintain a good CaR% and not for growth.

2 Likes

It is the biggest beneficiary of telecom reforms. The VI is not going to default

1 Like

Really sorry to sound like a broken record. But just wanted to check if anyone has done any scuttlebutt on the asset side of IDFC First balance sheet ? Normally in case of any bigger banks (HDFC, ICICI, Kotak, RBL, etc) there is anecdotal evidence - say people whom we work with, people whom we know, organisations that we interact with have used them to borrow funds. However in IDFC First’s case has anyone had experience with borrowers from the bank ? They have such a lot of diversified and small ticket loans that it is very surprising (atleast for me) to not have seen anyone based on a simple check. There has been loads of discussion on their deposit and credit card business which are very easily verifiable, but not on their retail assets (which comprise 64% of their total funded assets)

The reason why I am harping on this is because PMC was textbook example of how it is easy to defraud customers by showing fictitious loan accounts.

Call me a paranoid investor, but I believe it is better to be extra cautious rather than to follow the majority (which at times can be misled).

Disc: Invested and holding forms ~5% of portfolio. No transactions in last 3 months.

11 Likes

One could argue that the high level of retail NPAs due to covid second wave imply the small ticket loans are legit. The numbers reported by the bank are similar to NPA trends of MFIs most of which do cash-flow based lending.

Anecdotal evidence will not help us here, one would need to be a skilled financial forensic investigator to be sure of whether or not there are fake loan accounts. I doubt NPAs would be that high if there were fake accounts, the bank would have showed profits. Of course it could also mean the balance sheet is much worse if it turns out there are fake accounts and the bank is making loss despite that.

Unfortunately all we can do is trust the corporate governance and history of management to some extent. But be ready to exit at first sign of frauds like that if it does turn out to be true.

3 Likes

I would like to draw your attention to one thing. If you have closely noticed, in flipkart and amazon’s pay later facility the lending partner is idfc first bank.

Also they have just started their credit card business and their features are above par industry average. Let them give enough time and I hope we will surely see offers of idfc credit card on such mega sales.

4 Likes

Provisional quarterly numbers should be out in a day or two. Expecting strong growth in retail loans QoQ going by the commentary of VV in the AGM. CASA and deposit growth could be tepid as guided in the AGM( we can expect flattish growth by 1000-2000 crs). As mentioned in the AGM, from here on, the focus will now be on loan growth.

3 Likes

Sept Qtr numbers are out

1 Like

Deposits are down as per Management’s strategy of flushing out excess liquidity.Look at the LCR to get an idea about the same.

The retail loan book has grown 30% YOY which they have not highlighted instead have given a QOQ growth number of 7% !!

All in all its on right track and hope to manage the Asset Quality.

5 Likes

Card statistics out as well.

https://rbidocs.rbi.org.in/rdocs/ATM/PDFs/ATM082021A54F4D3A50C94B9BB68835EE1C36B956.PDF

Though a small base, but:-

Credit card nos: 7.5% growth (30k new cards issued)

vs HDFC flat nos (-.014% and 20k less cards MoM basis)

vs Industry (pvt sector only) growth of 0.7% (306k actual cards added)

Value of transactions: 10.3% growth MoM basis

Looks pretty good. IDFC FB is capturing 10% incremental share in credit cards.

11 Likes

When you look at the big picture it’s really hard to imagine why would anyone need to create fake loan accounts in a country like India. And co-operative banks aren’t really known for their corporate governance. Figure from this article.

There is a new partnership mentioned in the active lending partners list - Whizdm Innovations Private Limited or MoneyView, has 10M+ downloads on playstore.

Not sure if this was discussed before but demat accounts and broking were mentioned in AGM by Vaidyanathan.

Disc: Largest holding

3 Likes

Could you please elaborate on the reason for giving Idfcfirst this status.

VV is guiding to a growth of 15%/20% that is done by couple of other large cap banks, where quality (and clarity) of business is far superior.

2 Likes

Simple reason is size ![]() It is easier for IDFCF to grow 5X mcap than for HDFC/ICICI/Kotak to grow 2-4X in the same time period. Turnaround story available at low prices so why not. Also I’m only 29 so my risk appetite is on the higher side. Accumulated most of my holding last year below 30Rs.

It is easier for IDFCF to grow 5X mcap than for HDFC/ICICI/Kotak to grow 2-4X in the same time period. Turnaround story available at low prices so why not. Also I’m only 29 so my risk appetite is on the higher side. Accumulated most of my holding last year below 30Rs.

The guidance is 25% growth for next “many” years, for CAGR to be that high, growth will be higher in the early years because of low base so I expect loan book growth to be higher than 25% once issues are fixed (IMO question of when, not if they will be fixed).

7 Likes

In his recent speech at Leaders of Tomorrow summit VV said 15 to 20% growth.

This will be achieved by a large cap bank like Kotak Mahindra Bank for another 5 yrs at least. Even HDFCBANK might click that much, if not more. While giving the comfort of large cap investment.

Assuming the best case, even if IDFC first grows a few percentage points more, the comfort of a large cap seems like a better investment, from risk reward perspective.

But, come to think of it, my reason for giving it this status would be that it’s cheap. In the near future, it’s PBV would be much like Kotak Banks, around 4.

Reason: The growth rate is similar.

Ofc, for that, over the next several years the quality of the business should match up, and that’s the gamble, that’s the play in this investment.

4 Likes

Could you point me to that? I haven’t watched but he could be referring to total book until issues are fixed (they still have some big loans to clean up). Please send a private message so we don’t flood the board if these things have already been discussed.

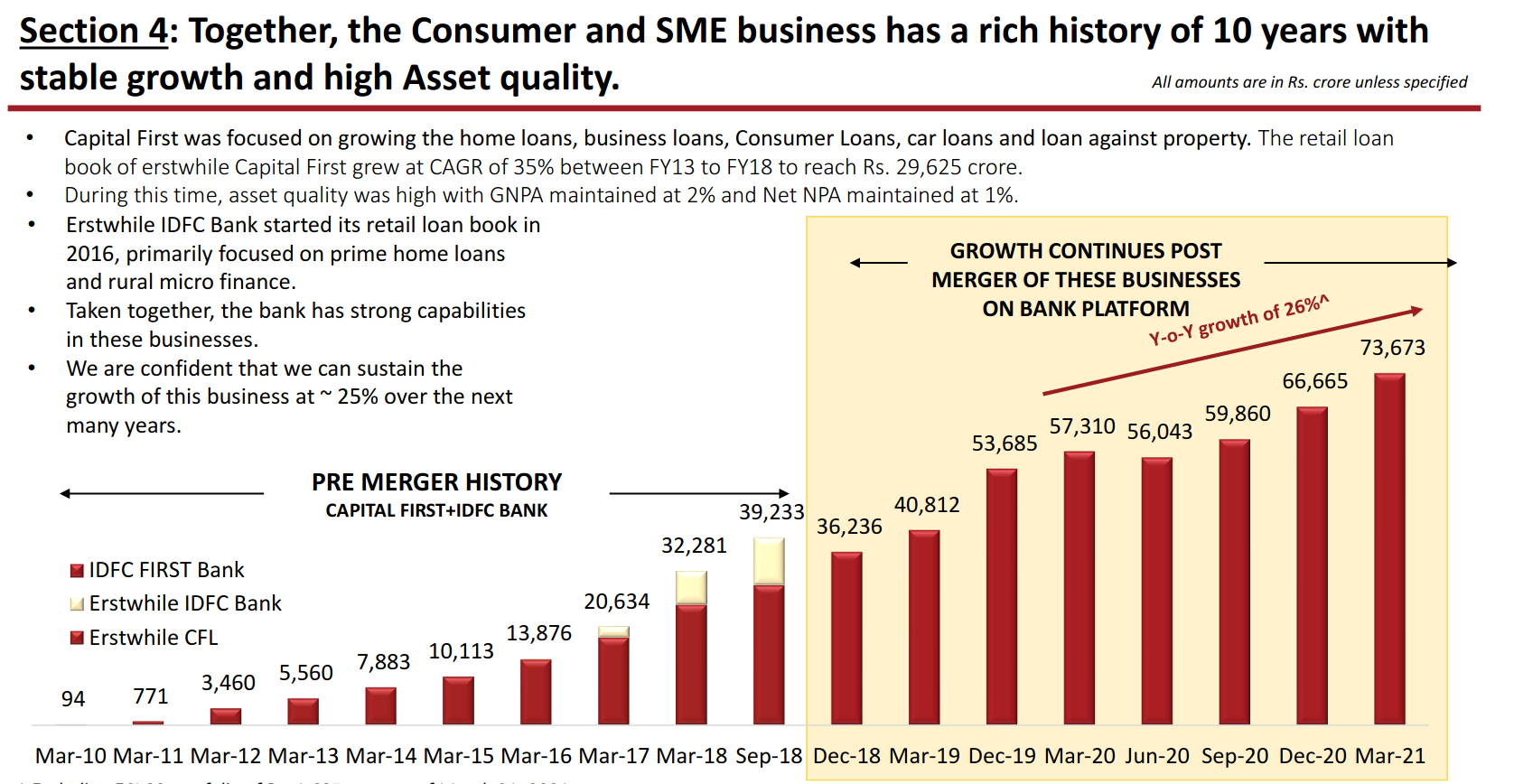

I was referring to retail book over long term based on this slide from Q4-FY21:

Because corporate book has been guided to be maintained at 40K Cr IIRC.

At this point in time, I have no reason to believe it won’t match but this is my personal view.

In any case, I would have gone with index funds if I wanted to reduce my risk. Also my stock investments only form about 60% of my net worth so I’m comfortable with this level of risk. For my financial goals IDFCF makes a lot more sense than other larger banks.

Disc: not a recommendation

3 Likes

The CEO mentioned that they can get larger incremental CASA if and when they require and currently it is their strategy to not increase it much in the next few quarters.

Can someone pls help me understand how CASA sales work? I mean the bank won’t be refusing anyone if they come for opening an account right?

Or does he mean the savings rates would be increased in the future- that seems unlikely.

How does a bank do push sales for CASA.

INV.

1 Like

If you look at the RBI cards data for June and August, the number of debit cards in force have grown from 31.09 lacs to 32.79 lacs. This translates to a sequential monthly volume growth of 2.70% and sequential quarterly growth of 8.3%.

In my view it will be fair to assume that the increase in debit cards in force data is a proxy for number of accounts opened. If this assumption is true it means that there is very good volume growth in CASA accounts opened but high ticket CASA has moved out in the last 2 quarters which has led to flattish value growth. We can draw 2 conclusions from this:

-

With high ticket CASA moving out and new smaller accounts coming in, CASA deposits have become more granular in nature which is good for the bank.

-

Once the drainage of high ticket CASA fades away, we will again witness a growth in CASA.

3 Likes

No matter how big a bank becomes, it would always welcome CASA, but at what cost.

Now that the initial target of 50% CASA ratio has been met, and they are in the green, with NIMs becoming comfortable, there is no need to give a higher interest rates in savings. Currently at 5%, they are still giving 1.5% more than Hdfcbank. Instead, they’d give these schemes, which don’t dent the NIMs as much.

Schemes like 1% cashback on debit cards only, for which Bank account has to opened, and AQB has to be maintained. Leading to higher CASA.

Or monthly interest instead of quarterly. This barely dents profitability, and differentiates them from big banks at a very low cost. Very smart. Idfcfirst was a pioneer, AU bank, Equitas followed. But, HDFCBANK, Kotak Mahindra Bank can never do that, with the number of accounts they have.

In summary, they will continue to introduce low cost schemes that differentiate them from the big banks and continue to attract CASA. He ought to, that’s why VV even wanted the banking license.

4 Likes

CASA is increased by banks through various means. It may undertake measures like opening new branches, incorporating salaried accounts, offering higher interest rates on savings accounts (and term deposits) to boost their CASA (which has been the principle strategy followed by IDFC).

An interesting (but yet small avenue) is also tie-up with Fintechs and Payments Banks. The Neo-banks in India are not actual banks and they need someone to hold the CASA book…banks like ICICI, Equitas and even IDFCF have been using this strategy. Similarly, Payments Banks have a restriction of not allowing more than 2 Lakhs EOD balance in CASA. To counter this they offer a sweep-in account where any money above the limit is parked there (Eg FINO PB has a similar arrangement with Suryodaya SFB). Besides the above there are also cross-sell and upsell opportunities like pushing credit card and BNPL accounts to also hold a Savings account through a sales effort (again the Bank can choose to ramp up and down the efforts here).

Discl: Invested

1 Like

Not a banker but one effective way I can think of is offer custom higher rates to HNIs. There was a user who mentioned last year that there were offered 7.5% for SA for to keep come crores (don’t remember excat amount). This way if RMs reach out to even just a 1000 HNIs and they keep 1Cr each CASA will go up by 1000Cr just like that.