Someone mentioned above that provisions for 50% of total exposure has been made…how did you come to 15% of 3200 cr figure…or is above info incorrect ?

Here someone mentioned a quote that 50% of total exposure provision is made…so is it 50% or 15% of total exposure…can someone pls highlight/confirm…thanks

1 Like

According to this interview earlier it was 50 % provided for .

Earlier the provisions for VI were as high as 50%. During last year VI provisions were brought down from 50% to 15% and put into covid provisions. So currently for 3200cr loan the provision is 15%.

4 Likes

3 Likes

End of Q2-FY21-from reports on IDFC bank Q2 FY21 results.

… and IDFC First bank has Rs.3244cr exposure (Funded - Rs. 2,000cr and Non-Funded - Rs. 1,244cr) which is 18% of net worth and had 50% provision on it. However, in Q2FY21 Bank has released Rs. 811cr (out of existing provisions of Rs. 1,622cr) against a VIL Exposure based on improved prospects and management commentary at the company, and utilized it to create additional COVID provisions during Q2 FY 21. If Balancesheet of VIL improves further than IDFC FIsr Bank can additionally write back remaining provision to strengthen balance sheet for future uncertainties and built additional non-specific provision which will provide comfort to an investor.

Did they move more provisions in Q3?

“IDFC First has Rs 3,240 crore exposure which is around 3 percent of the loan book”

From the article, it seems bank has only provided for 15% of total exposure and may need to provide another 3000+ cr if VI goes under.

Now when I do a calculation of 3% of loan book at 8x debt to equity, that means 24% of equity may need to be written off in one go!

So current book value per share of Rs. 32.5 per share * 76% (24% write off) may become Rs. 25 per share in a quarter or so. Most likely bank will go for some more fund raising / equity dilution.

It’s currently trading almost 2x that book value. I may get interested again at 35 odd levels as I like the retail banking strategy and products (have both SA and credit card) of the bank which can turn this around in a few quarters.

9 Likes

Just listen to the question at 33.00 regarding write off.

I am unable to understand the need for writeoffs.

Moreover, Im perplexed why they did not disclose 1400 cr writeoff in the presentation directly akin to CSB bank. Everytime IDFC writeoffs are brushed under carpet.

To put things under perpective shareholders fund in march 2019 - 18,159cr and jun 2021 is 20,170 cr and capital raise is 7000 cr

So shareholder fund is eroded by 4989 cr + Interest rate from their assets.

Time stamp is 37.25. His question was simple why non-paying stressed account is not moved to NPA bracket ? Instead VV was talking something out of context.

June 2021

Mar 2021

Erstwhile IDFC bank assets were so much rotten, even capital first earning and cut in 2% savings rate is not helping them.

Now, Vodafone is around the corner

“Banker has to lie until they make it. Orelse, they will be forced to raise capital at huge equity dilution”.

I dont think VV or even myself (if I am CEO of some bank) will be an exception.

Moreover, if you think deeply banking/financials are none of the worst business to be in. Primary goal of investment is to hedge against inflation. Return is secondary. My money as bank equity against inflation is as poor as FD when massive note printing happens. Except during normal times, that earns coupon rate of inflation + 4%

Discl: Sold everything today after holding since merger. Lost conviction after first conference call and writeoffs

3 Likes

Important figure to focus on here is the funded exposure of 2,000cr which has 25% provision against it. From conversations with bankers the unfunded exposure mainly pertain to bank guarantees for future spectrum payments. If Vodafone goes bankrupt these guarantees are unlikely to be invoked, for example in the RCOM bankruptcy no bank guarantees have been invoked by the government till date. So at risk really is the additional 1500cr of provisions that might be required if Vodafone goes bankrupt.

11 Likes

You can always find it in BASEL disclosures.

My conviction actually increased because of a single statement Vaidyanathan made - “Our loan book is nothing compared to the big banks”, which means he has long term goals on his mind and the only way to get there is with years and years of steady growth. I can understand the short-term frustration but we should keep in mind that banks like HDFC got to where they are today after 2 decades of growth. I personally don’t find many other long term bets in companies of this size (~30K Cr mcap) so I plan to hold, maybe even add more if falls below 40. Long term story is on track, retail segment is shaping up nicely with the exception of covid related disruptions.

A lot has already been discussed about results so won’t add more. But there was something interesting in the latest RBI ATM debit cards data release.

| month | total | change |

|---|---|---|

| january | 2773581 | 107530 |

| february | 2858871 | 85290 |

| march | 2935878 | 77007 |

| april | 3003620 | 67742 |

| may | 3038754 | 35134 |

| june | 3109070 | 70316 |

It is surprising to see a jump of 70K in June after repeated reductions in savings rate. I think the bank is back to actively pursuing customers and lower rates don’t seem to be an issue in getting new customers. Last year average monthly increase was ~65000 when the rate was 7%.

Disc: largest holding, no transactions in the last 9 months, not a recommendation

8 Likes

Government has provided moratorium on spectrum payments in past, so we should check if bank guarantees pertain to future payments and won’t be invoked…

Some insights on work culture at IDFC First.

5 Likes

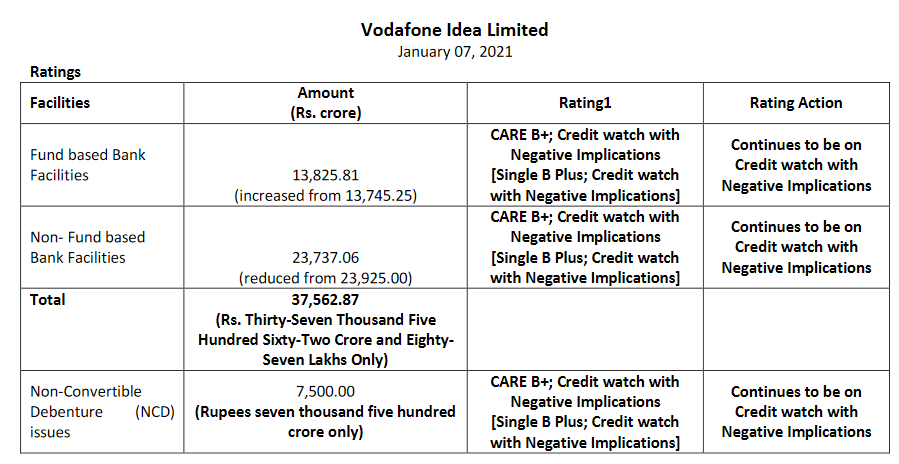

I was trying to get details on the exposure that IDFCB has to Vodafone (VIL); now Vaidy has confirmed that the banks entire funded exposure of Rs 2,000cr is through bonds and specifically NCD’s but hasn’t given any further details.

A Care Ratings report from Jan, 2021 shows that Rs 7,500cr of NCD’s are outstanding-

The breakup of the NCD’s is as follows-

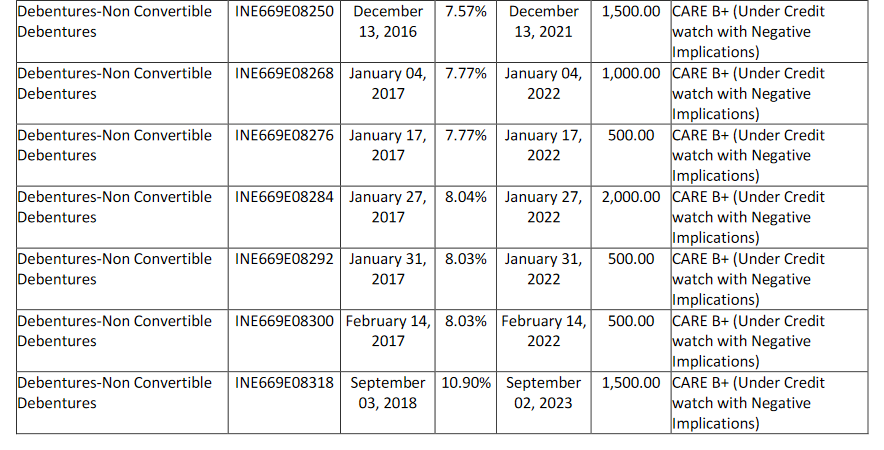

So out of the 7,500cr of NCD’s 6,000cr is maturing befrore 14th Feb, 2022 and the remaining 1,500cr is maturing in Sep, 2023. Now IDFCB has exposure of 2,000cr as mentioned above so its very likely that they own NCD’s that mature in 2022 simply because of the amounts involved. Furthermore the 1,500cr NCD’s that mature in 2023 were only issued in Sep, 2018 which was very close to the time when the merger pocess of IDFCB and CF was completed so its unlikely they would have bought those NCD’s.

The NCD’s which stand out for me as the one’s likely owned by IDFCB are the one’s maturing on Jan 27th and of the matching amount-

So if the above is accurate then the relevant question for IDFCB shareholders isn’t if Vodafone will survive but rather will VIL survive till Jan 27, 2022 and will they have the funds to pay back 5,000cr of NCD’s (the amount needed to be paid by Jan 27).

Now these two articles from BS and CNBC suggest that the Inflows/Outflows will be as follows-

Total Annual inflows

—4QFY21 annualised EBITDA post lease payments Rs 8,700 crore

—Incremental cost savings as per guidance Rs 1,400 crore

—Monestisation Rs 3,000cr

—Due from Parent Rs Rs 6,400cr

— GST Refund Rs 8,000cr

—Total Infows Rs 27,500 crore

Annual commitments

—Annual AGR installment Rs 9,000 crore

—Spectrum dues, payable in FY2023 at Rs 15,900 crore

—Interest cost on bank loans Rs 2,500 crore

—4QFY21 annualised capital expenditure Rs 6,200 crore

—Total annual commitments: Rs 33,600 crore

The important point on the above is that all the statutory dues (AGR+Spectrum) only need to paid by 31st March,2022 which is after the NCD’s payment dates. So in likelihood VIL should be able to pay back the outstanding NCD’s due in 2022. Furthermore if the Govt announces a relief package and most of the inflows come in then they should be able to see out atleast FY22.

Sources:

24 Likes

The price of IDFC First Bank has corrected from 68-69 levels to 46-47 levels in the last 5 months(a correction of 33%) in a roaring bull market of midcaps and smallcaps and justifiably so with concerns around Covid wave 2 Provisions, Vodafone Idea and a potential Covid wave 3.

While I had turned pretty cautious in this forum in the month of May, my view @ 46 is that even if we assume a default of VI on the Rs 2000 cr funded exposure, IDFC First wouldn’t have to provide for the entire 2000 crs as there will be 30-50% recovery via the resolution process. Worst case, say IDFC First has to provide the entire amount(additional 1500 crs), my March-2022 book value estimates still leave me with a clean book value of Rs 32.4. When ‘clean’ earnings start showing up, my estimate is that a consumer bank like IDFC First will conservatively command a P/B of 2.5-3x which will further be rerated with earnings acceleration.

Please note that we have assumed the worst case(default) scenario above. It is highly possible that a moratorium on spectrum payments for another year or 2 will enable VI to honour the entire 2000 crs.

Risks to my assessment:

- Any threat from a potential wave 3.

- Various reverse merger scenarios that can play out

P.S: IDFC First has started falling on thin volumes. Accumulators know that sentiment is bad and it is easier in such a market for retailers to drop their holdings.

4 Likes

How is clean book value estimated at 32?

My core PAT(without trading gains/losses) estimates(based on the concall guidance and trends) for Q2,Q3 and Q4 are 330 crs, 420 crs and 500 crs respectively. On this PAT number of 1250 crs in the next 9 months, take a provision of Rs 1500 crs. You will arrive at the estimated book value

2 Likes

Core Pre-Provisioning Operating Profit is 600cr in Q1 2021. The 2.5% net credit loss should be minimum with the COVID situation and legacy loans. I don’t expect the company is profitable in FY21. If Bank needs to add a provision for Vodafone Rs. 3244cr exposure, then they need to raise the fund with equity dilution.

The book value is 20,170 (Rs 32 per share) in Q1 2021.

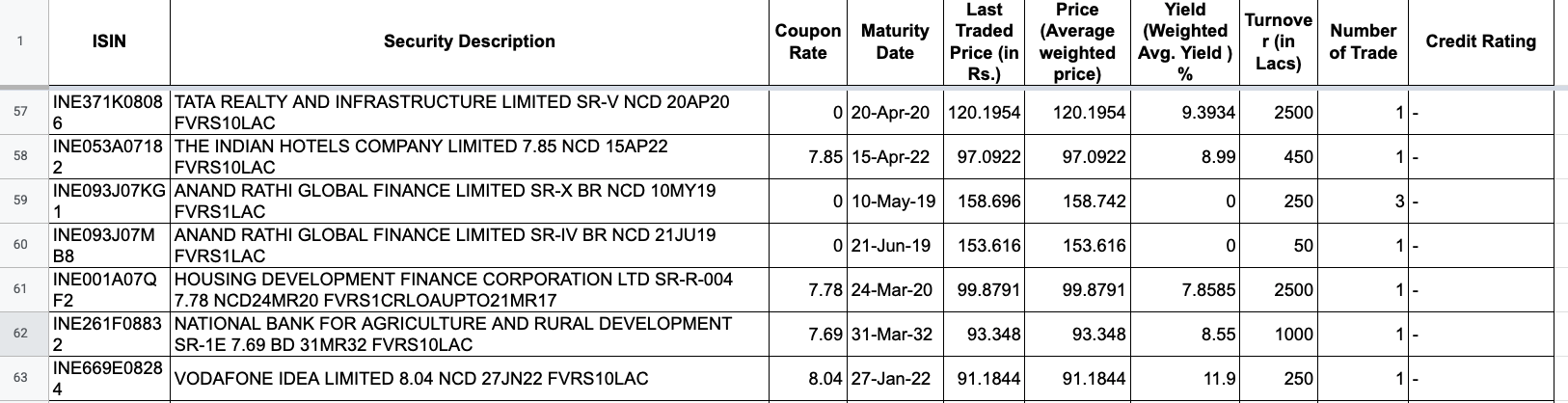

Thanks for the wonderful deep dive. I just wanted to add 1 limited point. Lot of people have asked why the provision was reduced to 25% of funded exposure. People are missing an important part which is that provision has to be somewhat in proportion to tangible evidence of risk. Now, these bonds trade on the market just like other instruments. Let’s pick one at random, I picked the Jan 27 FY22 one: Google for:

“INE669E08284” last traded price

This gives some links from msei.in. The latest data i could find was for april 16 at this link:

https://www.msei.in/SX-Content/daily/Debt/2019/April/16/Trade-Repository-Secondary_16042019.xlsx

So admittedly this data is old, but what it shows is that the VI bond was trading for 91 rupees:

See the last row. Now a bond trading at 91 rupees for the value of 100 rupees, does it deserve a very high provision? I dont think it does. Bond market indicates the trust in management to repay the principal. This context is important to understand why they provisioned how they did. Admittedly, bond markets might become illiquid right before a default so in the limit, this level of monitoring does not work. Also if someone has latest data for last trading price of this (or any other VI bond) that would be superb. Best I could find is current YTM on indmoney:

https://www.indmoney.com/bonds/INE669E08284/idea-cellular-limited-804-bond-yield

but i am not sure how to relate this to how much anticipated loss of capital (and this prudent provisioning) should be. If someone knows this, please do contribute.

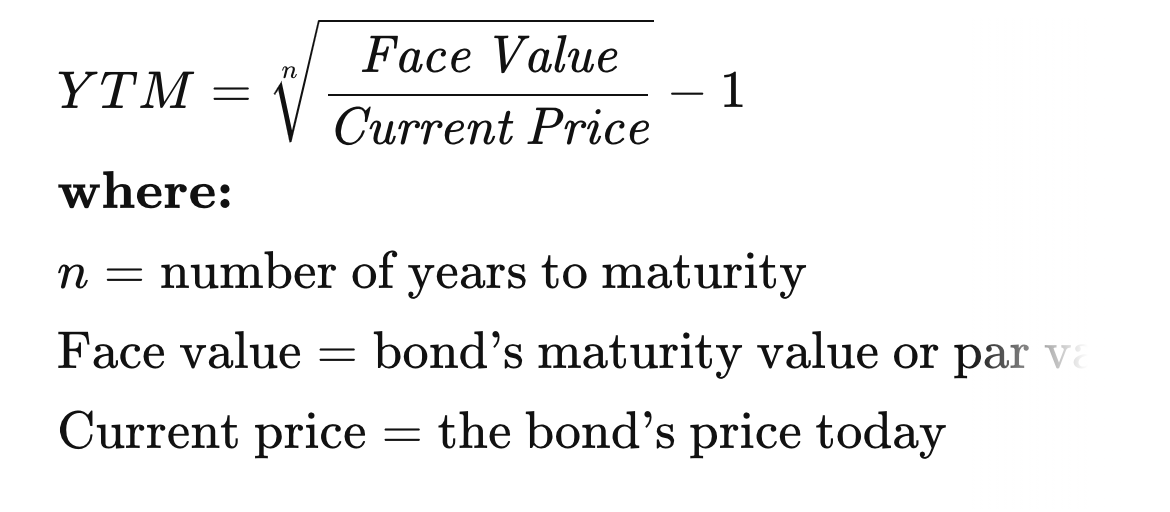

Edit: If i understand the formula from investopedia correctly

then this works out to Last traded price of 92 rs. Someone Please correct me if i am not applying the formula correctly.

Disc: invested, biased

8 Likes

Coupon payments may muddy the pitcure. Attached is the excel to compute YTM (both by using XIRR function in excel and from first principles) for bonds where price was known (16 April 2019) and discovering the price when YTM is known (16 Sept 2020)

VI Bond Pricing.xlsx (11.2 KB)

Disc: no holdings

2 Likes