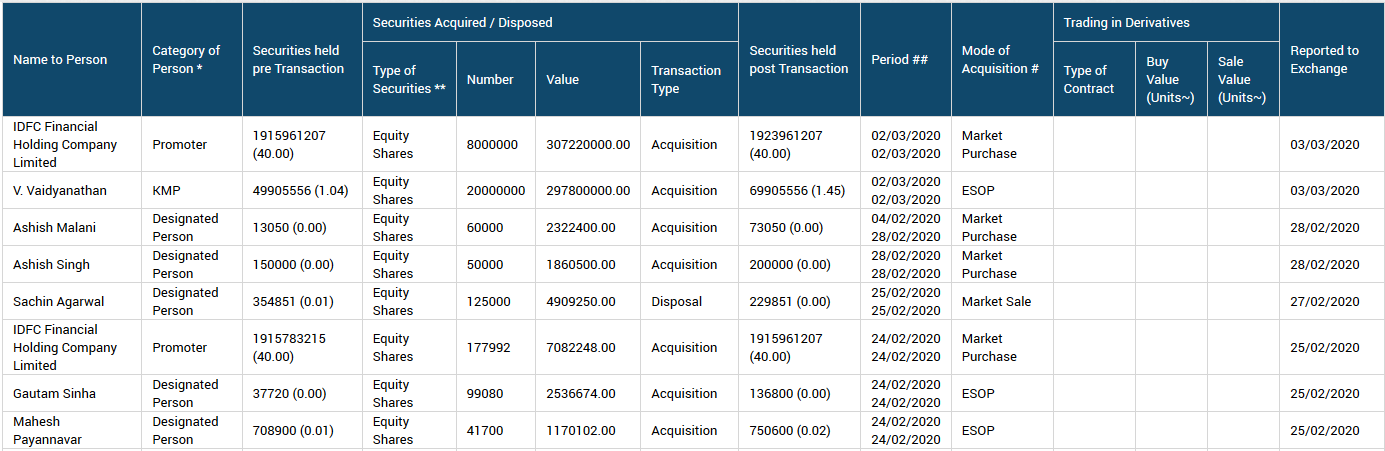

Looks like promoters are loving this volatility and using it as opportunity.

6 Likes

They have to keep shareholding at 40pc so whenever ESOPs are issued they need to buy

3 Likes

Vodafone has paid 3000 crores to govt today making it 3500 crores so far. Now the possibility of Vodafone going into liquidation is almost zero. So IDFC first should be able to get the entire principal amount and at least some part of interest.

2 Likes

Thats the maximum they can keep, not minimum.

It has nothing to do with it i think. Although they must have got the shares at a very cheap rate in esop than 38

There is a 40% minimum lockin for the first five years of the bank, so minimum and maximum are both 40%

1 Like

Vaidhyanathan has got the shares @15 rs. Thats too less. Generally esop are issued at 20 to 30 perc discount from current price. I didnt liked it

1 Like

Sorry but I am not able to understand linkage of voda paying license /spectrum charges and it going for liquidation.

Would really appreciate if you can help share more details on it please.

True it is at Rs 14.89, could we drop a note to the company secretary asking for clarification. The total equity is now 480 Crores

Nothing will happen, they will tell that it is approved by board. ESOP is general practice, what i didnt liked is the price. Although everyone is doing it. May be i am biased because i am holding it at higher price

These ESOP’s are from his Capital First days and converted at the time of merger into IDFCB ESOP’s.

What is the necessity to convert it into stocks now? I don’t understand how this works

Kumar Manglam had stated that if AGR charges are insisted upon then their operations would become unviable and the company would cease operations. Since they have started making serious payments and the govt is also cooperating to keep them alive, IDFC can hope for write back of 23 billion provision they have made.

1 Like

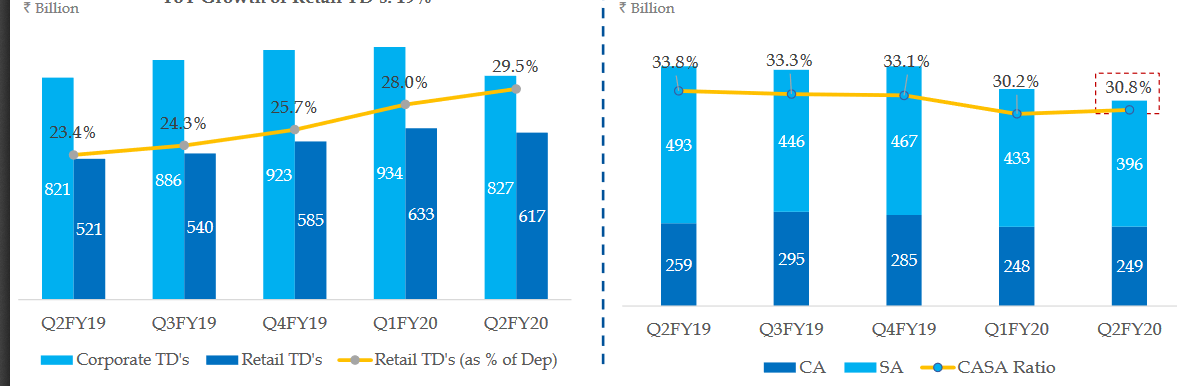

Rs 2000bn of deposits in YB that might move to other banks. IDFCB with the most competitive TD and CASA rates in the industry by far now.

2 Likes

My dear friend, people will not look at interest rates in this panic situation. They will not find a bank safe with higher rate of interest. Instead they will find solace in psu banks

4 Likes

Absolutely agree, I was observing the situation at my work place and the immediate solace everyone was looking for is to open account with SBI bank (Govt. will save it is their comment)

2 Likes

It will take some time for people to again start banking with smaller banks.

IDFC promotors are credible unlike yes bank’s promotors so they should not face much issue after while things will settle down and should get normalised.

They spending and focusing on brand building currently and once it starts delivering media too will start doing Tom Tom about it which inturn can help in confidence building.

It’s a testing phase for CEO , let us see how manages this phase with his team

1 Like

I could be wrong here but I think there are clearly two types of bank customers. One are PSU types - wants govt security. Others are private bank types who wants more features, online banking, RM etc etc. Since Yes bank falls in second bucket, I feel those customers would move to safer, bigger and better pvt sector banks like HDFC, ICICI, Kotak or maybe Axis.

Banks like IDFC First, RBL, Indusind, City Union etc are good pvt sector banks but in this scenario, I doubt anyone would be ready to take risks with smaller pvt sector banks.

6 Likes

Question is how long ?

We saw what happened to hdfc NetBanking and mobile banking between 2nd to 7th Dec ?

In short term there will be an impact of this back to back incidences of PMC and yes but over little longer term …can it have same level of impact ? And influence ?

Yes bank depositers would most likely shift to either PSU banks or HDFC bank. IDFC first bank has however a rich field to harvest from the lakhs of borrowing clients of ‘capital first’ who can easily be made depositers also. The FM and the RBI must make sure that the common man does not lose trust in private banks. The deposit insurance should go up to 25 lakhs and Govt should not wait endlessly for intervening. Yes bank intervention has come very late. The writing on the Yes bank wall was very clear six months back.

1 Like

The whole yes bank fiasco has resulted in fear, where other banks will find it difficult to raise money through AT1 or T2 bonds. Idfc first bank is also pirsuing to raise funds