It can take years for a business to show true colours ; When IDFC merged with capital first , nobody knew that so much of write off / provision had to be made of erstwhile loans given by idfc ; In that context and to make the retail oriented bank , VV has done a reasonably good job

There are numerous examples where many blue chip companies have remained underperformed for 4-5-6 years and suddenly in a matter of 1-2 years they cover up ; few examples

Reliance - Underperforned for almost 10 years , from 2008-18

Sun pharma / Lupin -2017-2022

ITC - 2017-2022

HUL - 2001-2008

I can IDFC laying some very foundations

No 1 banking app in Banking , features in top 15 banking app globally

Its coming out very strongly as retail first bank with great app , no transaction fees , good interest on savings etc

Created a very good brand in the market ; scaling presence in start up

Even though I am invested from last 5 years without too much of luck , I think next 5 years would be good for this bank ; it will test the patience for an investor , that’s for sure but at currency price it offers a good risk reward

I took 22 % loan growth as management has guided for this number after tapering from 24-25 %

Since I provided the excel sheet with calculation , hence I did not provided range , but if I have to give range this would be as follows for PAT in FY 25

Base Case - 10k cr of PAT with 1.5 ROA and 15 % ROE

Bull Base - 12k cr of PAT with 1.7 ROA and 17 % ROE

First - Can you please calculate Tier 1 capital ratio every year - and historically if it has gone down below 13%, IDFC raises further equity. So you cant afford to have lower than 13% tier 1 capital and have to raise funds when it goes down

Second - the ramp down of C2I is too aggressive - management guidance says 65% on a long term basis based on past 2 years of concalls. Any thing below 65% is unachievable.

Third - cost of deposits - why are cost of deposits falling down? Do you think IDFC can afford to decrease interest rates and can still garner the deposits which you have projected?

Just these 3 changes will kill down ROE third year onwards

Since as an investor, we get too biased with our assumptions, its better to take realistic scenario and worst case scenario.

The above three points are realistic scenario.

Worst case is - c2i remaind elevated at 70%, gNPA at 2%, NNPA at 1% ramping down to 0.75%. Fund raising at max 1x BV. Deposit growth doesnt catches up and borrowing starts increasing.

Then probably you will see its not a re-rating candidate actually.

To correct you, management says 65% by FY 27, not on a long-term basis. They have never said it will not go below 65%. In fact, the deposit franchise which is loss making of about Rs. 2000 cr as per their concall, will eventually come down to zero and become profitable. While at set up stage, on the expense side there will be opex, depreciation of capital expenditure etc. On the income side, there will be only a low income as deposits will be low. so with scale, it will turn the corner. We can check with the management on this quarter concall, on what the terminal cost to income ratii for the bank will be. All banks eventually reach 50% of so, or lower.

Re cost of deposits, lets check with management in the upcoming concall if they plan to drop rates. Earlier they have said “we dont commit, we could increase, we could reduce, VV quoted a cricket analogy and said we can go backfoot we can go frontfoot, we dont take a fixed position. Depending on need of funds.” For now they reduced it for below 5 lac to 3%, and increased rate for balances >5 lac. So you are right, we cant plan for rate reduction in the modeling, better to be conservative.

Can they raise capital at 1x p to b? Well hopefully they dont. They have always raised at premium, say 1.7x to 1.9X even when their ROE is only 10%.

hopefully (wishfully) stick may do better if and when ROE increase. We cant be sure though, markets are markets.

The wait is over. How long does it take for conversion of shares in the demat account after NCLT approval? Is there any other hang we should be worried about?

AUC First Bank has been a bit of a spoilt kid… Many marque investors have been betting on the company and this is reflected in price hence Price to book. I call this reflected glory. In future AU first will need to work hard to maintain this <>

IDFC First has an old book of IDFC which is like wicked saas bahu of old vintage and will take years to get rid off. Menwhile Vaidy is trying his best to grow the bank without taking undue risks … So Price reflects this …

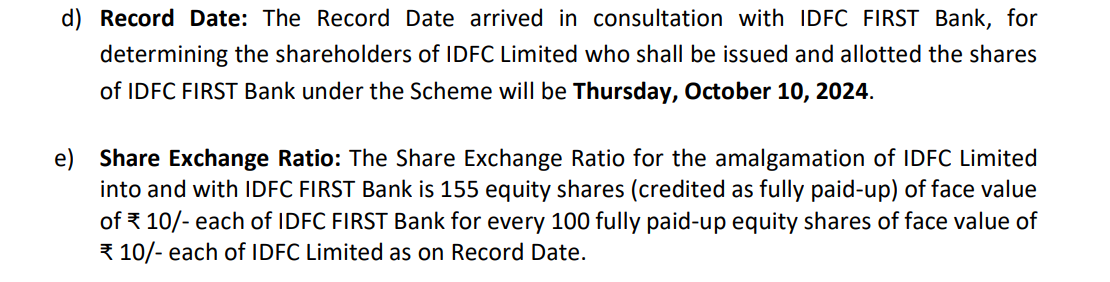

I believe you will need to unpledge the IDFC shares, or rather you should unpledge the IDFC shares before the record date to avoid any kind of confusion. Even if you don’t, you will get IDFC First shares in 155:100 ratio. But the new IDFC first shares won’t get pledged by default, they are a different ISIN so you will need to pledge them again after they are credited (if you want to). In any case my advice to you would be to explicitly unpledge the IDFC shares before the record date, which is 10th Oct 2024.