That he is aware of the cost to income ratio although it did not merit any concern as everything is going as per plan. To assuage the concern he says Growth in number of branches will be as per deposit requirement and branch target may be scaled down.

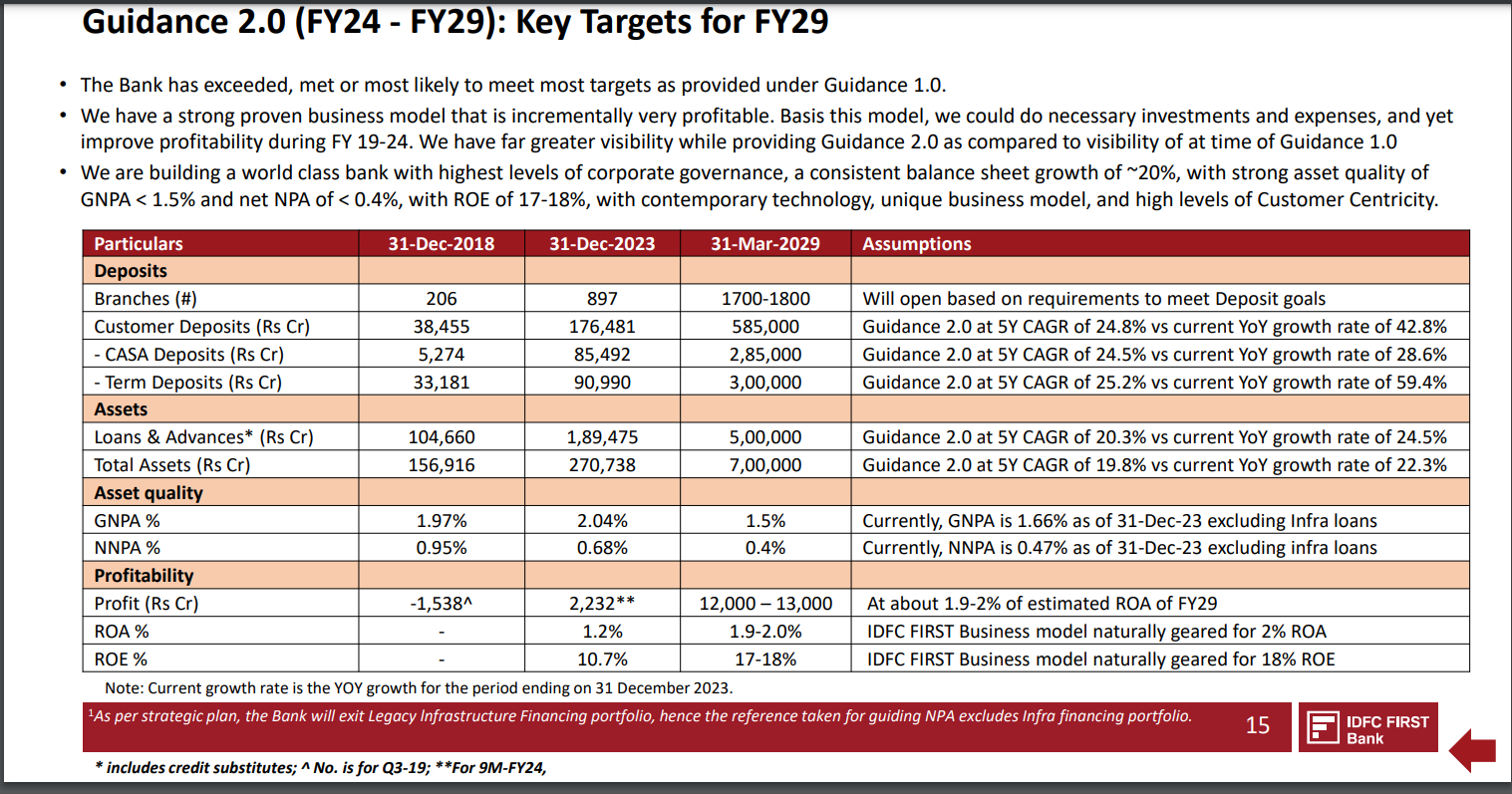

The next 5 year targets of liability and assets are conservative targets and easily achievable keeping past performance in mind. Some of these targets like asset quality, recoveries, GNPA etc are already achieved and bank has to only strive to improve further.

No worry on sustainability of High NIM of 6.3% as it is primarily due to business structure, and faithful implementation.

Completion of reverse merger, expected by June - July.

In my opinion, banking sector is a reflection of the state of economy and governance. As the economic performance is continuing to give positive surprises, good banks should perform well in the next five years. As usual, Private banks will perform better and out of these, smaller well run banks like IDFCF should do even better.

The monitoring by the regulator RBI is better than I have ever seen in last 30 years, which is a big comfort.

Checked with ir whi checked with cust service and reverted that the bank has some 15 million fastag and over 10m digital bnpl customers whose complaints are also added to total complaints and divided by number of branches for purpose of this calculations. Also compared to most othet banks whoae books are made of HL or autoloans, the bank has millions of consumer durable customers. Its for us all to agree or disagree, sharing what i picked.

.

Don’t want to speculate but strange to see warburg pincus exiting when it seems next 3-4 years will be great for the bank, specially after staying invested for so long…

Private Equity players have fixed timeline of 8-10 years for the entire funds and hence they would be selling irrespective of the fundamentals. Retail investors should understand working of market player like PE and use it to our advantage if we can.

Thanks for this explanation,

But can those timelines be so strict that they push a PE player to sell at a worst possible time and price…UNLESS they know something which we don’t.

To clear your doubts . I will give an example of the same investor’s( Warburg Pincus ) investment in Laurus Labs . Warburg bought a 32 % stake in 2014 at a 1700 cr valuation. They sold some stake when Laurus went public in 2016 at 5000 cr valuation (Stock price of around 100 )They sold the remaining stake ( around 20%) in May and June of 2020 at 5000 cr valuation( Again stock price around 100) . By the end of September 2020 Laurus was trading at 250 per share. By July 2021 Laurus was trading at 650 per share . They made 3 times their money in 6 years , but missed 6.5 times rise in the next one year . Once their selling was done , there was no stopping the rise. Remember they were on the board of Laurus too.

Fun Fact : Warburg Pincus invested in QIP of Idfc first bank in May June of 2020 at around 20 Rs per share . We cannot say for certain , but some money from Laurus sale might have been used for Idfc first QIP. Even after waiting for 4 years , they could not get the 6.5 times return in Idfc first that Laurus got in next one year .

Conclusion:

Even the biggest investor , with access to CEO and the board information can make horrible calls.

If you are right in the fundamental analysis of the company , the exit of the biggies is often the best time to load up .

It’s not a recommendation to buy Idfc first , but according to me it is definitely a good time to look at it more closely .

This observation on PE players is unfortunately a by-product of buying what I felt were fairly cheap companies and then to notice a big investor exiting . I had the same doubts. But this has happened a few times now that I feel confident in sticking to and continuously re-evaluating my original hypothesis. Sorry but there is no specific study on PE players.

Did they give specific data? Because this sounds rather hand wavy to me. Most of these places like Croma have other bank personnel too, not just IDFC First. So they should have as many complaints too right?

I haven’t seen such branch / shop board outside any retailer let alone a bank. Most I have seen are designer lights, not a fully functional LED screen where you can advertise actual products.

Net Profit for Q4 FY24 stood at Rs. 724 crore as compared Rs. 803 crore in Q4 FY23 - 10% Decline.

PAT increases by 21% YOY to Rs. 2,957 crore for FY 24 (PAT increased 28% YoY excluding trading gains)

Asset quality continues to be maintained at all-time best of GNPA and NNPA of 1.88% and 0.60% respectively.

All legacy infrastructure loans are fully factored into the above NPA. Excluding infrastructure loans, the GNPA and NNPA is only 1.55% and 0.42% respectively

CASA ratio continues to be among the best in the industry at around 47%.

Yearly:

Net Interest Income (NII) grew 30% YOY from Rs. 12,635 crore in FY23 to Rs. 16,451 crore in FY24.

Net Interest Margin increased from 6.05% in FY23 to 6.36% in FY24, based on AUM.

Provisions increased 43% YOY from Rs. 1,665 crore in FY23 to Rs. 2,382 crore in FY24.

RoA stood at 1.10% for FY24; RoE stood at 10.30% for FY24.

Quarterly:

Net Profit for Q4 FY24 stood at Rs. 724 crore as compared Rs. 803 crore in Q4 FY23.

Net Interest Income (NII) grew 24% from Rs. 3,597 crore in Q4 FY23 to Rs. 4,469 crore in Q4 FY24.

Core PPOP (Pre-Provisioning Operating Profit excluding trading gain) for the quarter grew by 22%

from Rs. 1,342 crore in Q4 FY23 to Rs. 1,632 crore in Q4 FY24.

Provisions increased 50% from Rs. 482 crore in Q4 FY23 to Rs. 722 crore in Q4 FY24.

Deposits & Borrowings:

Total Deposits of the Bank increased by 38.7% YOY from Rs.1,44,637 crore as of March 31, 2023 to Rs. 2,00,576 crore as of March 31, 2024.

CASA Deposits grew by 31.7% YOY from Rs. 71,983 crore as of March 31, 2023 to Rs. 94,768 crore as of March 31, 2024.

CASA Ratio stood at 47.2% as of March 31, 2024.

Legacy High-Cost Borrowings reduced from Rs. 17,673 crore as of March 31, 2023 to Rs. 11,809 crore as of March 31, 2024.

The Bank opened 135 new branches during FY24 to reach branch count of 944 by March 31, 2024.

Loans and Advances:

Loans and Advances (including credit substitutes) increased by 25.1% YOY from Rs. 1,60,599 crore as of March 31, 2023 to Rs. 2,00,965 crores as of March 31, 2024.

Infrastructure Project finance now constitutes only 1.4% of total funded assets as of March 31, 2024.

Exposure to top 20 single borrowers improved from 7.0% as of March 31, 2023, to 5.7% as of March 31, 2024.

Total Credit to Deposit Ratio improved from 107.0% as of March 31, 2023 to 98.4% as of March 31, 2024.

Asset Quality:

Gross NPA improved from 2.51% as of March 31, 2023 to 1.88% of March 31, 2024.

Net NPA improved from 0.86% as of March 31, 2023 to 0.60% of March 31, 2024.

Excluding infrastructure financing, the GNPA and NNPA of the Bank is 1.55% and 0.42% respectively as of March 31, 2024.

Provision Coverage Ratio (including technical write-off) has increased from 80.29% as of March 31,2023, to 86.58% as of March 31, 2024.

Net Stressed Assets as % of total Assets improved from 0.84% as of March 31, 2023 to 0.56% as of March 31, 2024.