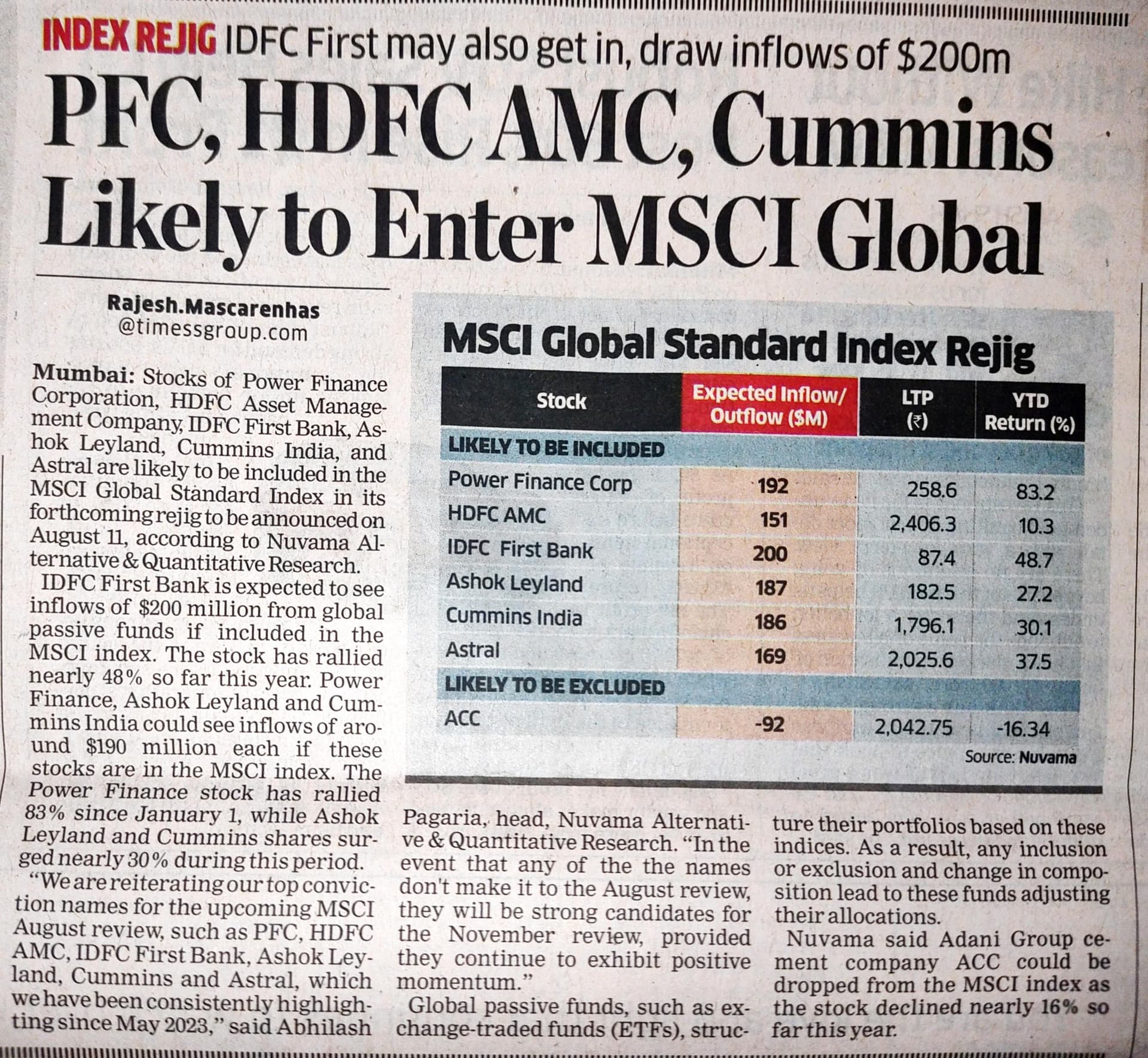

IDFC First Bank likely to be included in MSCI in its forthcoming, i.e. August 11, rejig with like 200 milion $ inflow as per Nuvama. Source today’s ET.

8 Likes

Its book value → shareholder’s funds ÷ no of shares

26,531÷663 = 40.012 Is it correct for banks ?

1 Like

yes that is correct. BV is also mentioned in latest investor ppt for june qtr

1 Like

This may not on a fully diluted basis, which is what we should be looking at.

Expecting a dividend from IDFC first for next 3-4 years will actually be hurting ourselves. Since dividend comes straight from Teir 1 capital, if we look at June numbers carefully, despite raising equity from IDFC ltd, their teir 1 has fallen substantially (this is primarily because of weights being re-assigned in first quarter every year to risky assets). a dividend distribution policy will not only accelerate the equity dilution in IDFC first but will also be detrimental to shareholder wealth creation.

in my opinion, major pain points in IDFC first is Cost to income ratio - which even if 65% is achieved (since the target of FY 25 has been increased from 55% to 65%), the bank will continue to raise the funds from market and hence it might end up with largest equity base bank in some years where bank will continue to make money, while shareholders wont be able to make much of it.

I feel the P/B of 2.2 is very richly priced with whatever current metrics we are operating on in IDFC first.

Please dont count me as nay sayer. I am just pointing the facts.

18 Likes

The sole raw material of the bank is money. If the bank starts distributing the raw material itself at the first sign of initial stability, then the earning capacity will be proportionately reduced. Banks should consider dividends only when they have excess cash and they don’t know what to do with it.

9 Likes

When the bank raises capital at 2.5 times P/B which is very likely, the book value will increase just by the capital raising exercise itself.

What we need to watch out for in the next two years is the increase in book value due to

1.) PAT increase due to operating leverage.

2.) Capital raising. IMO this is not bad if not good at 2-2.5 times book value. Although the equity will get diluted, the bank will raise capital at a premium to book value.

I agree that cost to income ratio is a pain point. But this is coming from it’s business model itself. Vaidyanathan sir clearly attributed the high NIM to their operating expenses. Also costs will stabilize over a period of time when they have good no of branches and when the new businesses they are establishing start becoming profitable.

Disclosure: Invested in IDFC Ltd which is my largest holding.

8 Likes

What if ROE continues to increase with time on operating leverage ? Most multibaggrrs come from rising ROE, increasing sales and profits give only compounding. Fact is fact but what one derives is different for different people. This is the market.

ROE 10 percent, next year sales growth 20 percent, ROE 11 percent, profit growth will be 30 percent. I think this way. How much ROE is inbuilt in business, Vaidyanathan has said many times i.e 20 percent. This shows the operating leverage tenure this company has to show in its results in future.

2 Likes

Cost to income ratio is not a pain point.

It’s an opportunity.

All depends on your investment horizon.

IDFC Bank is building a bank…and they need to spend all this money to build out the bank. And don’t forget presently they aim to set up 150 to 200 branches. In future, as they grow, the need will be for a lot lot more branches to make an impact. All this is cost…but as the base grows, this will moderate (as a ratio). But it’s possible not to an extreme level.

And this cost to income ratio saga at the set up stage may not be the end of it anyway.

The one other bank which has ramped up investments in current times? An old, very well established, HDFC Bank. They opened appx 1,500 branches last year (on a base of 6,000+ branches - that’s HUGE). This year, it will be another 1,500 to 2,000 branches. All guns blazing.

Why? Because they do not want to miss out the opportunity that lies ahead.

This hurts near term ratios (like ROE) and profitability. But as these branches turn profitable, I think in two to three years, they have a sling effect on the business (and this will reflect in ROEs).

If you are a long term investor, this is good. Near term investments (reflected in among others in the cost to income ratio) set you up for even bigger long term gains.

If you are a short term investor, however, you are in trouble (kind of).

Having said that what could go wrong for long term investors is if the execution is not up to the mark, or if in the quest for growth the quality of the book falls. So keep a keen eye on that.

Discl: Interested

15 Likes

Current book value is about 40. Merger with IDFC adds about 5% to the book value so it will go to 42. Profit is about 10-12% ROE so that gives earnings of around 4-5/year. Let’s say bank sells 30 cr shares in the market to raise capital, which will raise ~2500-2700 cr at 2 P/B. So excess of 1250-1350 cr above book value which will increase book value by another 2/share. So I see path for the bank to go to book value of around 50-55 by Dec 2024.

Buying bank via IDFC leads to ~77/share (120/1.55) valuation. So bank will be back to 1.5 P/B ratio if stock price remains stagnant till Dec 2024. If it continues to trade at 2 P/B then it can go to ~100/share which will be returns of ~30% in next 18 months (from purchase price of 77 via IDFC). I hope that bank can continue to do well in next 2-3 years which should help maintain high ROE, 2+ P/B ratio and some capital raises at that P/B ratio. This depends on merger with IDFC going through.

As bank’s capital structure gets simplified that should increase free float in the market as 40% of shares owned by IDFC will be considered free float. Rising free float and market cap will increase bank’s weightage in indexes and hence ETF. Passive investing is increasing in India which will push more money into ETF and hence IDFC First. I can see bit of this playing out already with MSCI inclusion.

Interestingly analyst covering bank at Morgan Stanley has changed and that has changed their position on the stock as well. Analysts are always prone with anchoring bias but that changes with new analyst. I won’t be surprise if rating changes from Goldman too with carrot of IB fees from capital raise. Goldman analyst hasn’t updated stock rating since 7th April 2023.

I am expecting 15-18% lumpy returns at least for next 3-5 years.

14 Likes

I think other streams such as fast tag, credit card will become profitable and will add to the PAT.

1 Like

Its all captured in the high cost to income ratio today.

When it’s built out…when the business on the books far exceeds the new acquisition and build out…that’s when cost to income ratio will moderate…

,…And profitability will kick in.

Its a process. Will take time.

Again, good for long term investors.

6 Likes

6 Likes

India’s retail credit is growing - Can it be a problem_ .pdf (249.4 KB)

India"s retail credit growth, interesting read…

2 Likes

I have a question and need yours valuable input, should not be all be shifting our investment from the Bank to the holding company ? Its giving a straight 12-14% of profit ? Am I missing something in this theory ?

We have to look into tax implication (LTCG or STCG) plus there is a remote possibility that the merger might fail.

4 Likes

1 Like

As of today Aug-10

IDFC price - 118.35

Idfc first Bank - 87.5

The switch will cost only 14.7% gain as on today. So if we include taxes on this some might gain and some might not gain on this.

But if we add fresh onto IDFC it will be give you additional gains once merger happens since the swap ratio favours IDFC holders

Disc : Invested in both

4 Likes

thanks, Sharvan for your input. but buying fresh IDFC is more risky , as price erosion can happen in future and even though we get the 1.55 shares of the bank the overall value will be depleted , however shifting from bank to holding negates that risks …i think…invested in both

3 Likes

Idfc first bank included in MSCI index. Hopefully it will lead to a good amount of inflow in stock

8 Likes