Capital First prided itself on growing dividend per share year on year. There was a regular chart on that in all the presentations which continued into the IDFC First presentations as well.

A maiden dividend, even if small, under the new management would definitely be a good sign of their confidence on the ability of the bank to now remain sustainably profitable after the clean up of legacy issues.

Yes, that’s my thesis as well. If they maintain their asset quality, they should create a lot of wealth. The key metrics to track in that regard would be the NPAs, the Special Mention accounts as well as the collection efficiency. Along with that I would also track the deposits growth, especially CASA. I feel that banks whose deposits are growing faster than loan book will likely be more profitable.

Disclosure - invested

Why should a bank pay dividends (when it can afford to)? For various reasons.

Other than the positive signals it sends out, one technical reason is that it attracts a whole new class of investors. The ones which like to earn a dividend.

Generally speaking, let’s take pension funds. Often pensions like to have a portion of their portfolio to yield annual income so that they can meet their annual commitments (and not wholly rely on debt). And not surprisingly, in the US (where some of the large pensions reside), from what we hear and see, dividend policies are very clearly articulated. Many companies even pay quarterly dividends. Cutting back or cancelling a dividend is a super big deal.

(Before it’s pointed out that big tech does not pay dividends…They buy back stock, which has the effect of giving back some money to shareholders. Kinda).

This is not to say that this idea is necessarily true in India too. But then we attract foreign monies. Some of it from pensions and other (partially) income seeking funds.

I would offer that a dividend paying stock has a potentially broader investor base that is interested in the stock.

Whether IDFC First can afford to pay or not is something that will need to be worked out (my gut feel is that it can, starting FY25).

To add further, dividends is the only real return realization for any investor and a proof that the company generates positive cash flow (in most cases). Any appreciation in share price is only theoretical/notional profit and can vanish when there is a market turmoil.

Profit booking on selling shares attracts just 10 or 15% capital gains tax. Whereas dividends is added to other source of income for which one has pay at their peak tax slab rate.

Moreover many companies’ share price falls more than the dividend declared on the ex dividend date. On any day I would prefer share price appreciation to dividends. But that’s just me.

Earlier DDT was at source given by corporates and that time investors used to feel dividend is tax free and liked it.

With DDT removed and dividend taxed as per slabs at hands of investors, perception has changed for many.

But fact remains same, dividend was always taxed. Now, no tax is deducted at source but yes investors pay different tax as per their slabs.

IMO paying taxes should not be criteria to like or dislike dividends or to consider it superior or inferior to capital gains.

Dividend plays a different role than capital gains and both are equally important aspects…

Just for example, in this highly uncertain markets, when business is doing well and promoters are ethical, we cannot be certain of capital appreciation over short/medium term because that depends on a lot of other factors…The only closest thing to certainity in such cases “maybe” dividend…

Above is just my opinion and i feel each can have their own in this regard…

For a shareholder holding Capital First shares, which then got converted into IDFC First shares after merger, how is the cost of the acquisition to be computed in case you sell and book gains/losses. Can someone explain this in simple terms please.

Query - what will be the impact of entry of jio financial services on overall financial sector ? (Of course on idfcfb also ).

Please share your opinions …

In this regard, we would like to inform you that during the aforementioned meeting, the Board will discuss and consider a proposal to raise funds in the next 1 (one) year from date of ensuing Annual General Meeting (“AGM”) of the Bank. This will be achieved through the issuance of equity shares or other equity-linked securities using various permissible modes, in accordance with the provisions of the applicable laws.

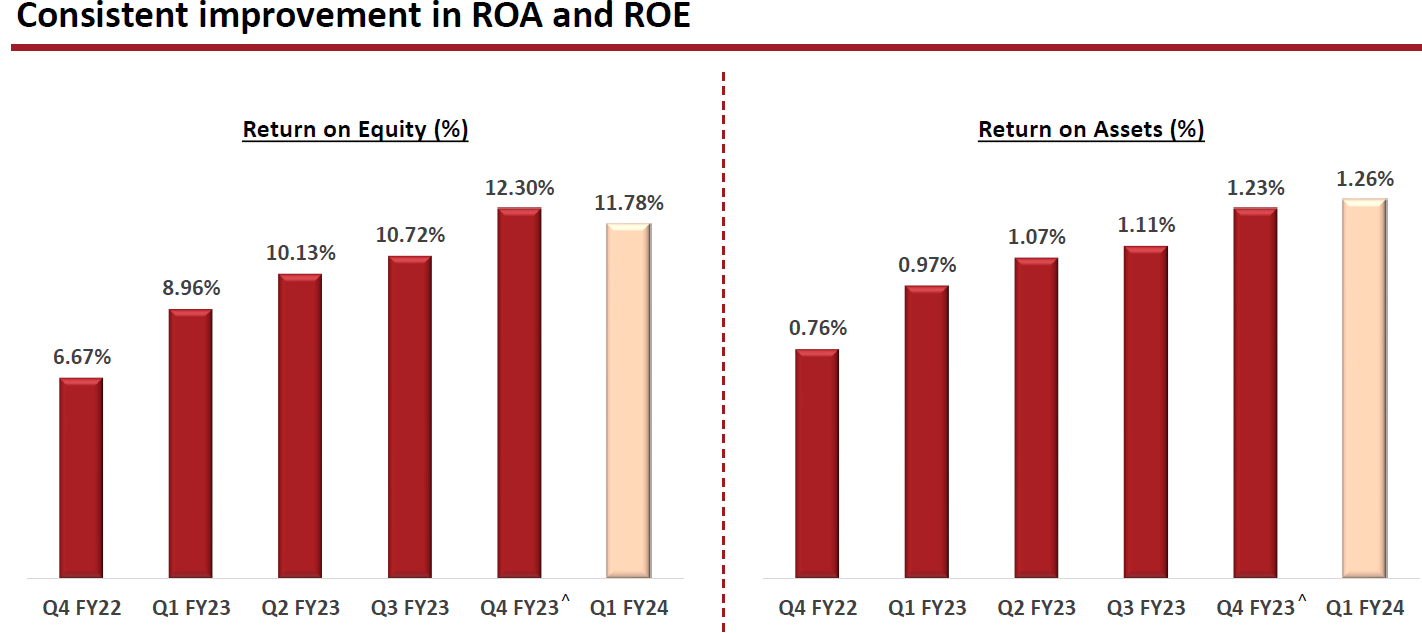

ROE impacted due to fund raising in March, and another fund raise will impact this qtr too. ROE for Q1 FY24 impacted by ~60bps on account of equity capital raised of Rs. 2,196 crore during last week of March 2023.

IDFC First bank has continued delivering good set of results as per previous management commentary. Broader market has noticed IDFC First bank now and stock has run up sharply.

However, I am expecting continued (a) good operating performance and (b) valuation expansion.

As per Q1 ppt, the current net worth is Rs 26,531 Cr and book value is Rs. 40.

So at Price / Book of ~2.1, there is room for valuation to expand.

At the same time, book value is expected to increase by 11-12% year on year.

Expecting more good times ahead.

perhaps more than valuation expansion, one needs to bank on growth in good quality business.

the easy money has been made (valuation expansion now that the story is widely known). now comes the part about the bank delivering results, year after year.

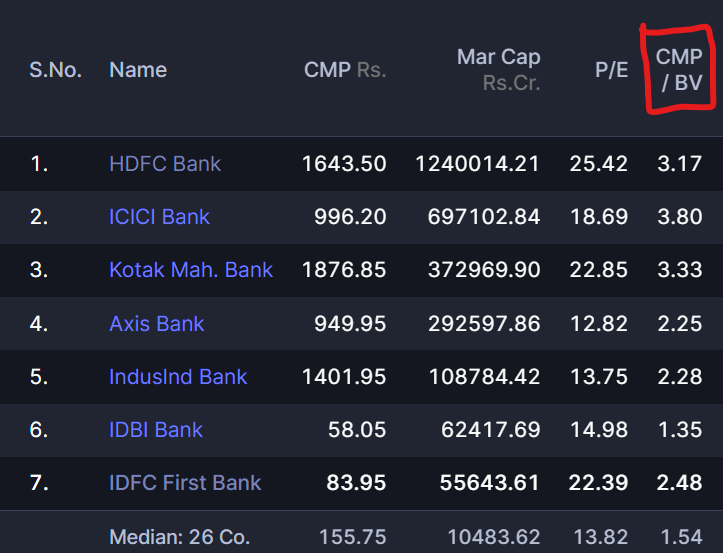

Screener has still not updated the book value. Total networth reported this quarter is around 25118 crores. At the current market cap of around 55644 crores, it’s trading at a price to book value of around 2.2. Book value per share will also get a small boost after the merger. All in all, not cheap, but still room for some valuation expansion over the long term if good performance continues.

Disclosure - Invested, added the holding company recently.

yeah, screener data is for FY23.

if we use june 2023 data, it will lower the ratio.

but it will lower it for the others too?

so perhaps in terms of valuations, IDFC First will still be in the middle of this group when it comes to PBV. just behind HDFC, ICICI and Kotak. but ahead of Axis etc.