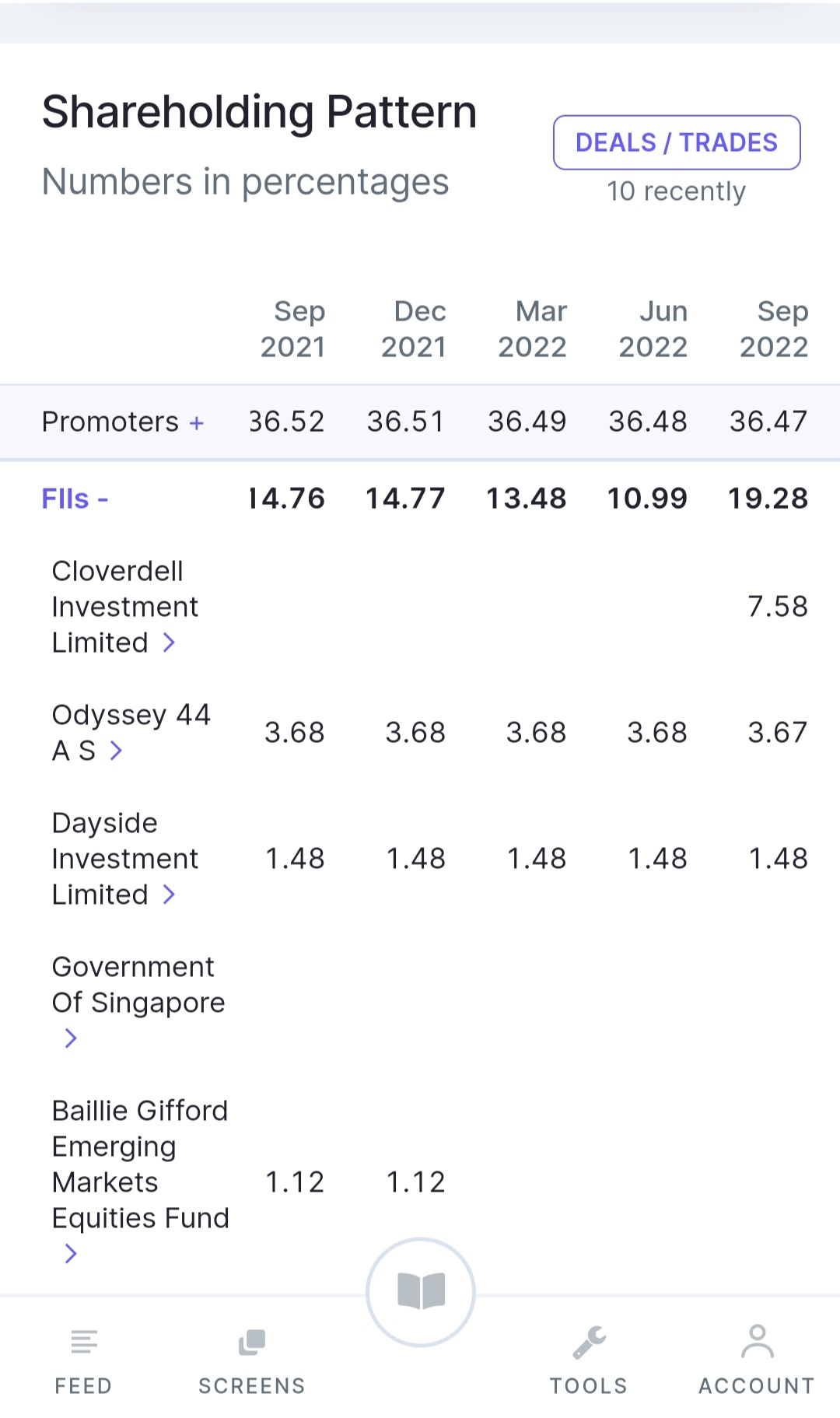

There is 0.7% increase in FII holding, if you remove cloverdell investment ltd. catagorisation.

So, actually FIIs have slowly but surely started to increase their stake.

There is 0.7% increase in FII holding, if you remove cloverdell investment ltd. catagorisation.

So, actually FIIs have slowly but surely started to increase their stake.

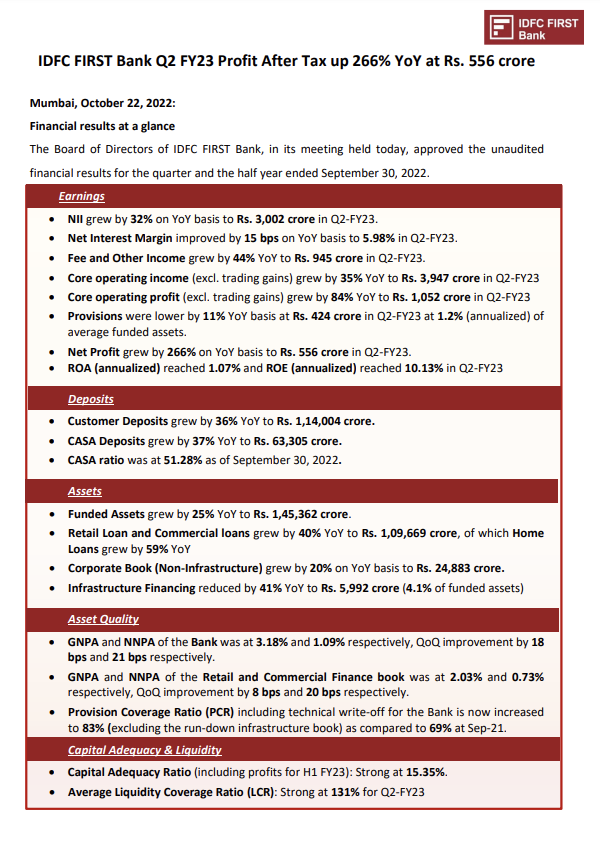

Results out now:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/11f165e8-5430-49e9-b2e1-53b8ba22dedd.pdf

Disc: Invested, biased

Some negative in the result I would like to point out, which are as follows:

(1) Increase in provision to 424 crore. Most of bank has seen decrease in provision.

(2) Profit include the more than 100 crore relating to trading gain.

Provisions were used to reduce the Net NPA which is very good.

Total GNPA increased by 41 crs during the quarter while the total NNPA decreased by 173 cr odd. This is only to increase the PCR which the bank has actively been doing for the past few quarters

In short, this is not to be taken negatively. The management is conservative and they are doing the right thing.

Next 12 months become pretty crucial in terms of how much book value accretion can happen.

Right now the book value is ~22,000 Cr with funded assets at 1.45 lakh Cr

If bank wants to be 20% credit growth, it will need to lend out ~29,000 Cr over the next 12 months. A part of that will be pulled from the excess SLR as of Sep 30, 2022 but the accretion to net worth will need to be much sharper than the current rate of ~600 Cr per quarter.

The last thing shareholders will want to see is equity dilution to fund the growth aspirations of 20%+

ROE at 10% is good but it will need to conclusively cross 15% and stay there for some time to enable the advances to grow at 20% over the next few years. Management indicates that the incremental ROE has been higher than 20% but the market cares about absolute ROE to derive comfort.

Would love to see the management accelerate their cost optimization plan and show faster than projected improvement in Cost to Income ratio. Retail book is granular and will have higher costs but we need a fine balance from here till the street derives comfort that the accretion to net worth can fund the growth aspirations without needing equity dilution.

Overall good results but more hunger on optimizing cost to income would be welcome.

HIGHLIGHTS OF Q2FY22 EARNINGS CALL:

Hosted by Kunal Shah from ICICI Securities

MANAGEMENT COMMENTARY

Vembu Vaidyanathan – MD & CEO

• Wish you all a very happy Diwali

• We have got some 5-6 quick comments to keep it brief

• From our point of view, basically we are seeing that the credit growth is quite strong - stable and strong – because we are now at 25% loan growth

• If you remember for 3 years, we were not looking at growing the loan book, as we were not strong on the liability side

• But now with a 51% - 50% CASA, we are feeling a very strong environment form the inside on the deposit side – so therefore now we are in a position to start growing the loan book

• The important thing is that we are growing the loan book along with the deposits

o Last quarter YoY loan book growth was 25%

o But we also grew the deposits by 37%

o So now we know we are entirely funded through deposits, funded through internal deposits on a strong basis

o It provides us solidity and it gives us confidence that we will sustain our CASA levels.

• That is very important because we need CASA for 2 reasons

o 1 is for normal growth – the 25% loan growth should go on for a while – we need deposits for that

o But for in our peculiar case, we need deposits to also pay off legacy bonds and borrowings which we need to pay – that is about 5000-6000 crore a year – we need for that also

o But the good news is that we are able to raise enough deposits for past liabilities, and also to fund our growth – so that is going comfortably

o The 2nd part is the Credit Quality. The Credit Quality front, I am happy to tell you that all the input parameters – underwriting quality is an input parameter – and frankly underwriting we have been always good – for 10 years now, our GNPA has been 2% and NNPA is 1% - and 10 years is a long time to establish a model –

But the underwriting method meaning the credit score of customers we are onboarding – continuously 85% of our customers’ credit score is above 700

So that tells you that the customer profile is very good and stable for a long time now

• Number of cheques that return is at an all-time low – it means that incremental underwriting is of good quality – much better than before

o The 1st month after the loan, you check the number of cheques that have been returned

• All input parameters, barring a few, are showing that they are doing well

• If you ask me to guess the credit quality 1-2 years from now, it’ll only be better than today

• The 3rd thing is the SMA

o The SMA is the strength of a loan book –

o It is the number of delays

o Our SMA1 and SMA2 – which is 31-90 Days Past Due - in this bucket – Our SMA same year last time was 3% of the loan book, i.e., 3% of the Loan Book could go to NPA

SMA1 and SMA 2 has now come down to 1% in retail

o If there’s not much portfolio left in that bucket only, we are not expecting much NPA formation going forward

• I am very comfortable and happy with the quality of the book; we can boldly guide for low NPA and low SMA for the future

• We had a lot of SRs that we had from the Bank from merger. The good news is that this quarter we sold some infrastructure SRs (Security Receipts)

o We had a happy outcome or so to say – many of y’all were afraid we’ll take a hit on it

o We had taken a provision of 200 crores for these SRs

o Now 200 crore has been released – as they sold well at a good price

o It is unexpected or found money

o We thought we will use it to improving the provisioning coverage ratio

o So our retail PCR has gone up to 77.6% gross of technical write-offs

Even write-off customer base we are collecting from

o That number is 77.6% - an all-time high

o So that 200 crore has been used for that purpose so it hasn’t come to the P&L in a way – but it has strengthened the balance sheet

• On wholesale side picture is not good but we don’t worry about it anymore. On infra there is no issue. It is a rundown book and will soon go away.

• On Profitability, we are very strong on profitability

o A very simple way to understand our profitability is Last year loan book has grown by 25% but growth in core operating profit – Pure NII + Fees – Opex – Core-Core profit - that is up by 84%

o Book grows 24 but operating profit grows 80, I’d say that is a bit on the higher side

I don’t expect every quarter to be such a high number but certainly this year, we should expect for YoY at least a 50% increase in operating profit over last year – but QoQ it has been even healthier than that – so you get the drift there

• We are happy with where the numbers are going – and hopefully you are more comfortable with us now.

• Because for 1st 2-3 years we have given you bad news after bad news but now we are feeling very good about the future

• In essence, I’d say that we are a very high-quality bank – our products are very customer friendly products – and any customers experiencing the products are usually very happy

• We are a customer-oriented bank, our corporate governance is very good, our balance sheet is very strong, RoE is catching up so overall I’d say things are looking good.

Mr. Sudhanshu Jain – CFO

• Balance sheet size is now Rs. 2.1 lakh crore – grown by 26% YoY

o Growth was largely driven by asset side by the retail portfolio

o Overall funded assets grew by 25% and 6% sequentially to reach 145,000 crore

• In retail class,

o Home loan segment grew by 59% on a YoY basis

o Rural loans grew 34% on a YoY basis

o And consumer loans increased by 36%

• The non-infra corporate book grew by 20% YoY and by 4% QoQ

• Infra book is reduced by 41% on a YoY basis and by 11% QoQ and is now sub 6000 crore and is merely 4.1% of total funded assets – compared to 21% at the time of the merger – so there is a significant downward move here

• Customer deposits grew by 36% on a YoY basis

• CASA deposit growth was very healthy

o CASA ratio was very strong at 51.28%

o Average CASA Deposits grew by 13% on a QoQ basis and 32% YoY

• Even on Term Deposit front, growth was strong at 35%

• Overall, Customer deposit growth came very strong in current quarter

• Bank continued to maintain excess liquidity – we don’t want to calibrate that is for the quarter it stood at 131% - this is well above regulatory requirement

• Branch count now stand 670 branches

• Bank has substantially granularized the deposits – this is reflected by the CASA and the TD less than 5 crore – 84% of customer deposits

• We have further repaid about 2000 crore of high cost legacy borrowings – the residual stand at 20,444 crore – which is still at a high cost of yield at 8% - we would sort of brim it down further

• PCR enhanced to 76.5%

• Rundown infra book’s PCR was at 83.3% including technical write-offs

• Corporate book ex infra – PCR is 98%

• The restructured book as a % of total funded assets has reduced to 1% compared to 1.3% last quarter

• Gross and Net Slippages were at similar level to last quarter despite increase in overall book.

• PAT was highest ever at 556 crore - up 226% on a YoY basis and 17% on QoQ basis

• On a quarterly annualized basis, RoA is at 1.01%

• Strong growth was driven by steady growth in operating income

• NII grew by 32%

• NIM expanded 9 bps on QoQ and 15 bps on a YoY basis to reach 5.98%

o The increase also happened due to transmission – this happened due to the repo rate increase on the existing floating rate portfolio

• The retail fees contributed 92% - so it is quite granular

• Increase in OPEX was relatively higher due to increase in business volume in Q2

• Cost to Income improved to 73.34% in Q2 from 80.52% last year.

• Core Operating profit grew by 84% YoY and 7% QoQ to 1052 crore

• Provisions were lower by 11% YoY

• Credit Cost on a quarterly annualized basis as a % of average funded assets was 1.2% and for H1 it was at 1.1% - which is still much lower than 1.5% guided before

• CAR including profits of H1 was 15.35% with CET ratio at 33.67%

Q&A

Bhavin Gala – Marine Capital

Q: Could you please help us understand the performance in the recent quarter with respect to retail commercial banking operations? Because this segment turned profitable a few quarters back and there was inconsistency as far as the PBT is concerned – but this quarter there has been a drastic decline in PBT from this segment. If you could help us understand the reason behind this…

• It is a very important question

• You recollect that we suddenly sold SR and got 200 crore provision released

• That provision released we took it to retail

• And therefore, it is showing up there on the retail line

• For example, if we hadn’t gotten the 200 crore we would not have taken that provision of retail – it is that simple

• So if you add back that 200 crore – you know your numbers are back to the trendline

Ishaan Agrawal – Erevna Capital

Q: In your last call, you had advanced the guidance of double-digit RoE which was originally given for Q4 of FY23. If I look at core-core numbers for the quarter, excluding treasury gains and do a like-to-like comparison with Q1, the PBT excluding trading income is lower in Q2 is lower at 644 crore compared to 648 crore in Q1. And hence, RoE and RoA excluding trading gains is lower in Q2. Are you confident that the bank can touch core annualized RoE of 10% ex of treasury by Q3?

• Yes

Q: Secondly, the annualized credit loss for the quarter was 1.2% - that is less than for retail and wholesale. What is the credit loss guidance for retail + commercial book?

• We have not called that number out separately

• Overall it is at 1.2% and H1 it is 1.1%

• We would not want to call out that number

• If you take the retail credit loss, if you add back the 200 crore of extra provision – if you don’t take it as a one-time item, then it is at about 400 crore.

o 400 crore x 4 annualized is 1600 crore

o Divide that by 1 lakh crore book – you get 1.5% - 1.6%

Q: Will this get better as we concentrate more on home loans or do we expect it to be at 1.5%-1.6% going ahead?

• We’d like to be conservative on this number

• If it gets better, we’ll take it as a positive

• If you think of the bank, think of it that retail – and retail is a pretty good yielding book – and our credit controls and collections are also working well

• Otherwise such a low credit cost on such a book…I mean it’s already pretty good so I don’t want to say anything beyond this

Q: Opex for this quarter is around 8.7% higher than Q1 Which is actually higher than the loan growth QoQ. Is it because we have invested more on the tech front? What is the reason behind this large jump?

• On a QoQ it is very hard to comment

• There are a lot of moving parts – it’s a large bank

• But broadly speaking, you should expect the Cost to income to trend downwards from here

• If you take YoY, these inter Quarter up and downs gets evened out

Q: When Capital First was founded, we were quite ahead of the curve in developing an algorithmic lending model based on multiple parameters – demographics, marital status, gendee, etc. – and hence we enjoyed a niche in that segment – now that data related to a borrower is more easily available to a larger number of lenders – thanks to aggregators, payment apps that capture cash flow data, 90% of our borrower have credit history. Has the significance of the lending model reduced for the bank?

• India is just not served – Underserved would be an understatement

• This advantage we have will not go away

• We are guiding for a growth of only 25%

• Our own ability – forget what others do or don’t, I’m sure others can also use this data – but our own ability to use this data is completely getting better

• Our ability to use the data is improving

• Our algorithm is getting much more refined – it has refined since the last 10 years – it is maturing and getting more and more precise

• The quality of the algorithm is getting better every quarter on quarter

• We feel that we are very, very far ahead in this game

• We have gone through R&D ourselves – we have built it from grassroots and we know every single moving part of this machine

• I think we are getting better and will be great in this front

Q: Right now, it is helping you on the credit quality front and not as much on the yield front? Because we are also concentrating on better yield customers?

• Yes and no

• One definitive advantage that we have as a bank – we may be new, we may not be as profitable as others, all these issues – but the one very unique thing about our bank is that our book itself has been created in an era where cost of funds was 9-10%

o At least the models were built for that kind of cost of funds

o So therefore, we were specializing in lending at 14-15%, probably more

o And you know the credit quality numbers

• Therefore, now suddenly our cost of funds have come down – but our capabilities haven’t gone down

• The mix of the book would probably be better yielding - but that doesn’t mean we are taking riskier yields – it just means we are more specialized.

Q: You have been maintaining that India is underserved – unlimited credit demand for the next at least 10-20 years – so in FY24, for XYZ reasons if GDP growth stagnates, then because of our small size, will we still be able to grow our loan book by 20-25%?

• Yes.

• We come from a small base

• To give you a small idea, supposing our LAP or take any business, say you are booking x amount of business a month – say 500 crore a month – if we increase it to 600 or whatever it is – we don’t have to do anything – we don’t have to change credit criteria. We just have to open 5-6 more locations – and lo and behold we will get it.

• We have base effect

• Big players at 7-8-10 times our size

Q: So, if I have to put it that way, HDFC Bank is adding an IDFC First bank every quarter, then.

• Yes, absolutely.

Nitin Agrawal – Motilal Oswal

Q: How are incremental spreads are moving? And how to do you see margin trends in coming quarters? And if you could share the proportion of loans linked to EBLR?

• 38% of the funded assets – linked to benchmarks – which could be MCLR, or repo or T-Bills

o Out of that 60% is linked to repo

o And the rest to other benchmarks

• With respect to margin expansion, as we have guided earlier, we feel that we will be able to comfortably maintain at the 6% mark – this quarter we are very close to that - we are already at 5.98% this time

• We of course had the benefit of some reset – as RBI has increased rates by another 150 bps

• Benefit should be slightly higher in Q3

• Even though Cost of Funds are going up – Even for us Cost of Funds on a blended basis went up by 25 bps – but since this reset kicked in, even for the new loans we have increased the pricing a bit

• So, a combination of this led to a higher yield on advances which are interest earning asset – which led to an increase of 9bps

• We feel that both things do sort of work in tandem

• We could be a beneficiary as the rate cycle plays out

Q: The consumer loan portfolio has been growing every quarter and the YoY growth now is 35% - but this quarter it was essentially flat. We have seen stronger growth from other banks in the consumer loans – so any specific reason that has cause this?

• 19600 crore book we are talking about…

• We have sold 333 crore during this quarter

• Plus, Q1 was relatively a strong quarter, because it was summer and consumer durable sales were also equally strong

• So hence these numbers are the way it is

• Not only consumer, all our lines will grow.

• Our home loan book is 15-16,000 crore, Large banks’ home loans is 4-6 lakh crore. Can’t even compare.

• We are relatively smaller player than the 4-5 banks in the market – but we will keep growing.

Lalit Dev – Equirus Securities

Q: On Borrower side, our refinanced portion has increased to 35% - if we include the market borrowings - what is the broad range of interest we are paying on these refinanced borrowings? And also, if you could tell us about what is the average tenor of these borrowings?

• We don’t do much borrowings anymore, in the sense that I think you must be talking about treasury market borrowings – they are not the big items

• We keep evaluating various funding opportunities

o We see the prevailing rate, the average tenor of funding which could sort of come in

o So, we have done some sort of additional refinance because they were at a longer tenor and the rates, they were at were at a better level

• Legacy Long-term bonds and Infra bonds – these 2 items are continuously coming down

Q: On Fee Income part, we have been going strong on our credit card business. But on quarterly basis, Fees from credit card and toll business has declined. What is the reason for this decline?

• That is essentially the decline in the toll business

• There has been restructuring done in the NBR on the issuing side

• On issuing side, there was a notification that came in on April 1 of 2022 and hence that re-adjustment has happened at that line item

• And credit card, fee has gone up on a sequential basis.

• All Our fee businesses are doing very, very well

• Cash management, toll, wealth, credit – every product is turning out to be a big success – so nothing to worry.

Q: Wanted to know if you could share the portion of salaried customers in the home loan portfolio, and how has it changed over the past couple of years?

• It should be 55%-60% that are salaried

Ashutosh Kumar Mishra – Ashika Stock broking

Q: On cost to income, We are guiding for cost to income of 55% by the end of FY25. What are the levers for this strength that will help us take it there from the current level?

• Our Cost to Income was 74% for this quarter

• We have always said…but for clairity I will repeat, that there are 3 lines of income that are going to improve our cost to income – they are very precise, defined items – they will play out.

• #1 is Paying off legacy liabilities

o We have contracted on 8-8.5% - we will replace is at around 5% - there is a lot of money to be made there

o That will give us on a quarterly basis about – if you do the differential of 8.8 minus 5.5 and multiply you will get the number of 150 crore

o If you think of it, it will come to us, there is nothing to be done

• #2 is Credit Card business where scale is coming up – 75 crore numbers round-off

• #3 is 300 crore from retail liability side as new branches come up

• In this Quarter’s P&L if you add these 3 numbers – 150+75+300 > this works out to ~525 crore

• If you the PAT impact of the number – if you take 75% of that amount – it will come to 390 crore

• You divide our expenses of 3895 crore by 4472 crore – that is this reported number that is 3950 crore of income and then you add this number – it’ll come to us and play out in the next 3 years

• Then that number you divide 2895 crore and you divide by 4472 crore – you will get to 65%

• In my mind it is a pretty simple, straight forward proof that we will easily get to 65% Cost to Income simply by paying off liabilities and making credit card business profitable and making liability profitable

• We feel that it’ll happen. In our mind there is no doubt at all.

Q: So because of what has been happening on the cost of fund space since the last 2 weeks we have seen Larger banks are increasing term deposit rates. You see some of these things impacting…?

• The calculations already account for rising interest rate

• If you think of large banks – none of them is carrying borrowing at 8.9%

• We aren’t borrowing but we have 8.9% sitting in legacy on our balance sheet

• Therefore, you can’t really compare us with big banks

• I will show you my cost to income in 15 years – I will show you what our cost to income will be - you will rub your eyes

• You cannot compare a 3-year bank’s Cost to Income with a 25-year old bank

• Something very important for you to note, if you go back to the numbers on the presentation – CI was at 92% at the time of the merger – now it is at 74%

• So that is a major decrease

• This tells you that incrementally you are building the bank at a very good cost to income and as and when the story plays out, it will come down

• So don’t worry about the cost to income

• I just have to play a normal game and it will come down

Q: The liability franchise we have built over the last 3 years…how many of them have we breakeven on? Can you give more clarity on new branches…what we have opened and how we will come by?

• No real benchmark about how to compute this

• Maybe close to 450 odd branches on a variable basis would be profitable

Sahil Sharma – SS Capital @sahil_vi

Q: We are building a bank for the next many decades – and I’m sure you are hiring with that in mind. Can you please talk a little bit about the credit risk team we have on the retail side? Because in banking, the most important thing is getting the money bank - not just giving it out.

• Absolutely, I agree with you.

• The people we are hiring – it is not so many credit managers as before as 5 years ago

• Earlier, managers used to go over files in detail and evaluate and all. Of course, we still need to do it – in product, home loan, LAP and all that – for them to look at some of the files – but incrementally a lot of people – a lot of machines are doing all this work

• Our focus is on developing good, high quality algorithms

• The skills levels we are looking to hire are at a very higher order – not the traditional people

• We are hiring that kind of people who can build this high-quality tech, AI, ML, Etc

• As a bank we provide a really good working environment

• We have very proud employees as they can see from within the quality of the bank we are building, the ethics and all that

• We are able to hire really quality people – any position we are on the lookout for, we have 100s of applications - we are spoilt for choice for openings that we have, really

• We are looking for a Head of Design to build really good interface and UX, in case someone listening has that skill set, we’re looking for a Head of Design and I’ll hire you.

• High quality technology, coders, DevOps people and all that…

Q: What we as investors really appreciate – I’ve been with the bank for around 3 years now roughly - is that we have really turned around DSI institution + NBFC into a retail bank – and that has been a long and strenuous journey – and on most fronts there has been a tremendous turnaround – the last remaining thing now, which is at the top of the mind for most investors is cost to income – I think you answer on the income side, on how it will expand is brilliant. If you can also share on the cost side – is this the correct leverage for the cost? For example, if we double our AUM, our costs won’t double from here. So, if you could give some Rough guidance for cost to income for FY23-24?

• We are building for the long term

• We are not doing a shortcut

• 3-years have gone by there is not 1 item that is a shortcut

• It’s hard but we are very proud of the clean, ethical culture we have – it is from within

• In terms of Cost To Income, you reconcile to previous question – you add those 3 items of legacy, etc - Within 3 years, you will see…you watch this story and you will also see that it’ll come down

• You just watch the story year after year and we will go there

• As an insider, I can see it – you will also see it

• As the scale plays out, automatically the cost to income will also sort out

• I’m going to share some data points with you and that will help you understand how the bank has progressed

o If you take the core PPOP of the bank - in FY19 it was 1100 crore annualized for the H1 after the merger (Capital First and IDFC put together – 1st half year after the merger)

o Now if you assume credit cost at 1.4% on the whole book –which is a very reasonable assumption - that will come to 1300 crore

o Pre-merger income was 743 crore – Assuming credit cost 988, it was a loss situation

**o FY20 when you do the same calculation – it has become 250 crore positive **

o FY21 has gone to 400 crore

o FY22 has become 1079 crore

o We have already guided for over 50% over last year that is about another 4200 odd crores of PPOP

o If something is rising from minus to 1000 crore in FY22 - You can see how this chart is rising

o We as insiders can tell you that the core is delivering very strong

o Core is rising sharply

o You watch at FY23, 24, 25 – I don’t think this is changing

Q: On Capital Adequacy, we are at around 15% - are you comfortable with this or would there be any fund raise in the next 1-2 years to support 20-25% loan book growth that we want?

• We’ll evaluate from time to time

• Internal accruals are strong now, growth is also strong – so we’ll play out this equation

Sagar Shah – Phillip Capital

Q: We have already reached about 10% ROE in this quarter itself – instead of Q4 you had guided for - we are early in the game – going ahead what are the key drivers for further traction on ROE and ROA? We are expecting traction around 13-14%. So, what are the drivers in this respect?

Q: Going ahead, we are having a very good run as far as the economy is concerned – the corporate credit growth front would it go up faster than retail?

Q: Have we seen the average cost of deposits and borrowings – that is coming at around 6% - compared to this quarter? Are we peak-ing out on average cost of borrowings at least for this quarter and going ahead?

• On average cost for Q2 was at 5.5% - which was 25 bps higher than previous quarter

• And many of the Repo increases are priced in the market rate

• No Substantial increase going forward

• Offset of this, even loans get repriced – so both should change in tandem – so we are not too worried on that front

• We don’t take any fixed positions on interest rates in the market

• We are paying only 4% upto 10 lakhs and frankly, we are not planning to change that currently.

• We have enough margin but we don’t need to slow down the pace of deposits

• Scale and operating leverage is all that is needed to RoA and RoE

• Income, we expect to grow at 30% on a larger base and 25% on a smaller base – you know how scale plays out

• And of course, there are so many other product lines likes fees and all that stuff – so many new business lines we have launched, all that will grow

Franklin Morias – Equintus Wealth Advisory

Q: From the time of opening the branch, till the time all costs are loaded, what is that period, how many months does it take?

• It is hard to give a standard number for these things

• The time would vary on the variable you consider

• It could be 18 months, 24 months depending on how you load the cost

• We look at it in the way that we don’t want to give Reasons for each branch – as only people who will bend their back over understanding this, like you, will get it

• Most people will just look at the ROA and say, are you improving?

• All costs put together; we are committed that ROA will go up YoY here on – it is already going up – but we feel that it will go on

• You take this quarter’s PAT of the bank:

o The 3 well-know items: Credit cards, legacy liabilities, set-up cost of a branch – 525 crore or ~500 crore

o Now you take post-PAT impact of the number, that will be around 375 crore or 380 crore

o Give it 3-4 years, and then you find that this kind of money will start coming to the P&L hopefully

o Now this quarter’s PAT was 555 crore – so you add this to 375 you will get to 946

o You add 946 x 4, that is 3800 crore

o What it’s the equity base today? 22000 crore

o So now you are nudging 60-70

o So now do you have any doubt in your mind that these 3 items we can’t turnaround?

o Of course we will

o In my mind, even if it were a simple playing math of just add these numbers and do it, the bank is heading to a very healthy RoE

o So, for those of you who are willing to wait, and give us the time, you will see the numbers. We have no doubt.

X.

Ps. There have been certain omissions/paraphrasing in these notes. It is not a word-for-word transcript.

Did anyone asked around reverse merger with IDFC Ltd? As IDFC in their AGM told that they have asked IDFC first for their future capital requirement.

I did catch that undertone that hint when VV said he isn’t strapped for cash as CASA growth is good. He is constantly giving hints that he is not interested in RM at these rates. I could be accused of reading too much between the lines. With both managements making it a point to not show their hands, this is the best I can do.

I totally understand VV’s pov. His supporters were with him in the worst times, when he was given a tough hand. He turned it around, and now early investors want their returns to be commensurate with the risk.

Parent company also understands this, and is therefore playing along. The talks have not progressed as price as moved from Rs.30 to now Rs.60

I feel, RM won’t happen till the market sees the complete potential of the bank.

No one asked a direct question and when asked about the capital raising plan, VV answered that it will be evaluated on a ongoing basis or something to that meaning

RM will happen at a better rate is my take as already market understand that 1.4 is minimum RM

My two cents based on the management commentary and results:

Management has tried to make good use of the trading gains this quarter by spending more on opex. I believe some part of the opex is quite discretionary for the management and they will undertake it based on other moving parts of the income sources.

Other Income is up 5.12% QoQ which is good but could have been much better if MDR(Merchant Discount Rates) for issuer banks for fastags were not revised downwards by the Govt. Since the effective date for this revision was 01st April, 2022, there was reversal of toll income in Q2 which was booked in Q1, loss of income in Q2 and high base of Q1 made the growth look lower. If not for this factor, other lines of the fee income(Wealth Management, banking, Loan Origination, credit card, trade forex etc) registered excellent growth(double digit QoQ). Dec’22 Quarter is going to be bumper for fee income and we can see a 10-12% rise QoQ in fee income in Dec’22 as compared to Sep’22.

Markets will see a much stable sequential performance from the bank every quarter atleast for 2.5-3 years. Any exceptional, one time gain that the bank makes will be used for discretionary opex or strengthening the balancesheet.

Reverse merger will only happen when the bank wants it to happen and the valuation at which it wants it to happen. IDFC Ltd may be the one holding the golden egg(AMC Cash and IDFC First shares) but the egg can only be hatched by the bank. In my view, the bank would want to be fair to its investors and the QIP investors who poured money at 57.35. Any RM will only happen after capital raise at a significant premium(in my view upwards of 75/Share). IDFC Ltd should continue to trade at a premium of 27-42% till merger is announced.

For anyone who wants a stable growth portfolio company with minimal turbulance and air pockets should seriously consider this bank for the next 3 years in my view. By my projections, Bank will deliver 15%+ RoE and 65% Cost/Income by Q4FY24.The trajectory and pace of expansion in RoE and RoA will leave almost every analyst startled

.

[Donation of entire equity stake held in IDFC Foundation by IDFC ] www.bseindia.com/xml-data/corpfiling/AttachLive/ec851632-fa39-4c8c-9edb-b6896dc59729.pdf

With this step, I think, IDFC has ticked all the boxes necessary to seek approval of RBI for the reverse merger with IDFC First Bank. AMC sale just needs the approval of SEBI which may also come through quickly.

Disc: Shifted entire investment in IDFC first bank to IDFC and app. 10% holding

Srinivasa

Kindly suggest your rationale of moving out of IDFC first bank. with all the ticks as you mentioned, is IDFC bank not good to hold anymore or what is your thought process.

Thanks

The value of IDFC’s holding in the bank (36.52%) is Rs. 12725 Cr and the sale value of AMC business is Rs. 4500 Cr. As against this, the mkt cap of IDFC is only Rs 12175 Cr, an implied discount of some 41%. While the IDFC shareholders may not be able to get the entire upside of 41% as when the reverse merger happens, it is a reasonable expectation that one can get at least half of it ie 20%. It is my belief that the bank will do very well in the run up to the merger and its performance will get reflected in the IDFC market cap. Only when the implied discount goes below 20% or so, I will think of switching it back to the bank.

If and when IDFCFB share price crosses 80, the equation would start changing and the arbitrage available now, will dissipate. It doesn’t look like that VV is in any hurry for the merger. In fact he should delay the issue of Tier 1 capital as much as possible to get a high price for shares to push up the book value as well as minimise the equity dilution. That would be in the long term interest of the bank.

Too much is speculated about the merger. The take is that the merger is a given as the shares already exist and no dilution will happen. So all this talk of book value, ROE etc. is futile. The only matter of importance is that does he want to raise more equity from the Rs 4000 crore odd cash balance on books of IDFC. VV will be making an honest mistake if he does not… But in any case there is just going to be a slight difference in taxation. From a capital gains in our hand ( on shares received after merger ) or dividend taxation. So rest your horses…It is not a material difference !!