Hi guys,

IDFC bank Q4 Fy22 capital adequacy ratio was 16.8% and it was at 15.77% in Q1 Fy23. I think for this quarter it should be close to 15.10% to 15.30%.

Next quarter the probability to raise money is very high , if they don’t raise money next quarter then the CAR might be close to 14.5% levels.

I have a few question would request if anybody could answer them.

Will they raise money? because they can grow this year without raising which will result into higher ROE but if they raise through TIRE 1 that would result into lower ROE than the ROE without capital raise.(this is because the money raised will not generate return immediately)

Will the management want higher ROE for this year or a good amount of capital in their balance sheet?

The CEO has been signaling that in case they have to raise money that would be through TIRE 2. Recently SBI raised TIRE 2 capital at 7.56% when the GOI 10yrs yield was 10 to 15bps lower than current levels. So if they raise TIRE 2 it would be close to 8% because the credit risk is higher here compared to SBI and yield have gone up .

Will they consider raising money at these rates?

Over the next 2yrs the inflation is expected to be lower than 6% in this case the cost of their TIRE 2 will be further high.(Interest rates going down cost of debt increasing)

Will they wait to raise money at lower rates or raise at higher rates?

If a bank expects high ROE in future which is going to be higher than cost of equity in this case they should raise money thorough equity because this prevent cash outflow.

So currently equity is favorable and debt unfavorable. Will they raise through equity?

Since they are preforming so well they should have the ability to do QIB placement in case of Tire 1 capital raise. A bank will any day want QIB placement because the price decided in this case is highest compared to preferred share or warrants.

Does the bank have the ability to do a QIB? What conclusions should we make if they don’t raise through QIB?

If they do a QIB placement in this case we get to know the price that the market(QIB) and management think as a fair price for this bank.

Just to add in the end, last year they raise money through QIB placement at 57rs and in 2021 they raise money through preferred shares at 23rs.

Clearly, Their current ROEs don’t support the growth they are witnessing in their RWA. Clearly they’ll have to raise soon.

What can they do to delay the raise?

Increase the mix of low RWA assets in the disbursement and AUM mix. This can be achieved through an increase HL share etc. - Highly likely

Decrease the mix of High RWA assets - like Credit cards - Highly Unlikely.

Raise T2 capital, IDFC is super smart in this sense and already raised T2 in Feb i.e before the reverse in the interest rate cycle- Unlikely.

Wait it out till the peak CAR levels of 12-12.5% - Risky Unlikely.

Slow down their AUM growth & Limit the growth to the extent of ROE accrual - Highly Unlikely.

If they were to raise equity?

There will be 4000cr hitting IDFC Ltd bank account in few weeks & will be available for equity infusion- Infusion of this capital into IDFC First bank at ANY PRICE ABOVE THEIR BOOK VALUE , will instantly increase the current book value of the bank, thereby giving a markup for all the existing investors. - My assessment is that IDFC Merger will increase bank book value by about 10% (Considering the merger discount).

on Paper considering their current ROE, IDFC FB need about 2k cr of new equity/T2 cap per year for the next 2 years to maintain their 25% growth & Current RW. with the current growth momentum, IDFC FB can easily raise via any channels. It is highly likely that they’ll take money from IDFC Ltd.

ROE cycle post new equity rise depends on 2 factors, ROA & Gearing. it is a matter of time before they inch up.

ROA is the better metric to assess lending institutions, ROE can always be boosted with high gearing. ROA shows the true book quality & profitability.

Effective 10th Oct 2022, IDFC First bank increased interest rates for savings, FD, RD, etc. Got the below PDF from my bank RM in whatsapp and not as public announcement email.

Above 10 lakhs, interest rate is 6.25% in savings account.

I understand it was mentioned during the AGM of IDFC Ltd that they have asked the bank if they need the capital now for which the bank will be getting back to them in couple of weeks time.

I guess we should hear something on this along with the results.

Between this transaction can only take place post the AMC sale approval which is expected in 4-6 weeks time.

With all due respect to your experience, I would like to submit a few counter arguments. These are as follows -

IDFC First reported an advances growth of 24 pc in Q2 disclosure to the exchanges which is 1.5 times the Industry growth.

It reported a deposit growth of 36 pc in Q2 disclosure to the exchanges which is almost 3.5 times the industry growth !!!

Their CASA has grown from 10 odd pc to north of 50 pc in the last 3 yrs.

The Bank enjoys very good customer feedback and reviews.

Once the gross NPAs come down to 2 pc range and Net NPAs to 1pc range ( if it happens ), the bank may be in for a structural re-rating and may start to command PE multiples in the 20s… provided the credit and deposit growth sustains.

By the looks of it, IMO most of the pain should be behind and the bank may be staring at a very bright future. Such solid deposit, credit, CASA numbers sustained over a period of time can potentially be a recipe for a multi bagger.

Just wanted you and others to keep this in mind before making a buy/exit decision.

Thank you for the thesis. I agree with most part of your post. However, i think the bank can still raise Tier-2 capital which is just 2,618 cr as of now.

I think it can raise 2,400 cr more without any issue. I know the interest rates have increased quite a bit but if it doesn’t want to dilute equity, this can be a solution.

If the bank feels reverse merger will take time or if it wants the share price to appreciate before further equity infusion, it can still raise Tier-2 as it did earlier this year.

I’m guessing that reverse merger will happen only in Q1 FY 24. V.V might want the bank to hit the ROE target for FY23. Equity infusion before the FY23 end might only reduce the ROE figures for the whole year. And the last fund raise also took place in Apr’21 i.e at the start of a new Financial year.

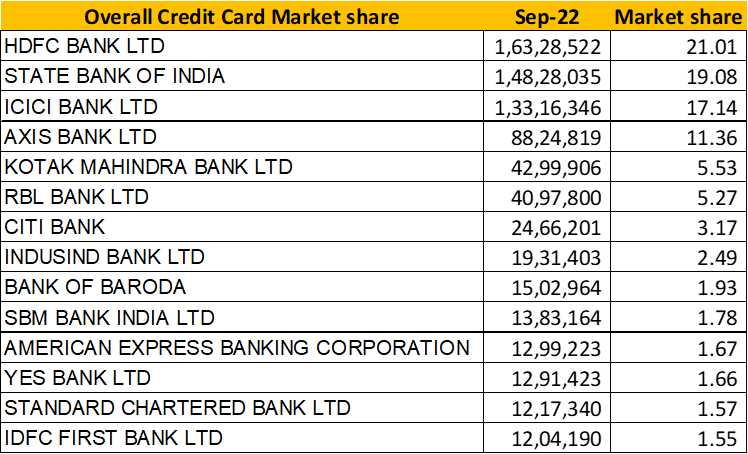

Spend Share for IDFC has decreased MoM, something to look into

October Data will give more insights on Spends, given the festive offers

In absolute terms, Total Spends have increased, but they have lost some market share

Spends per card is also marginally down month on month, from 12.7K to 12.3K

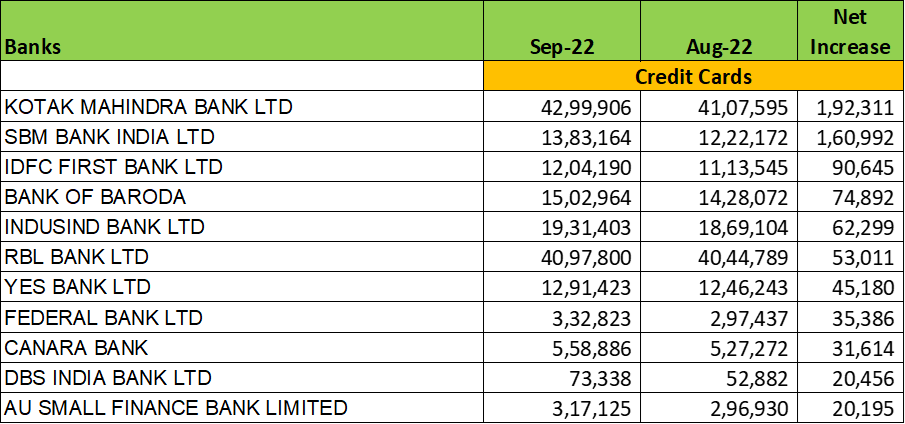

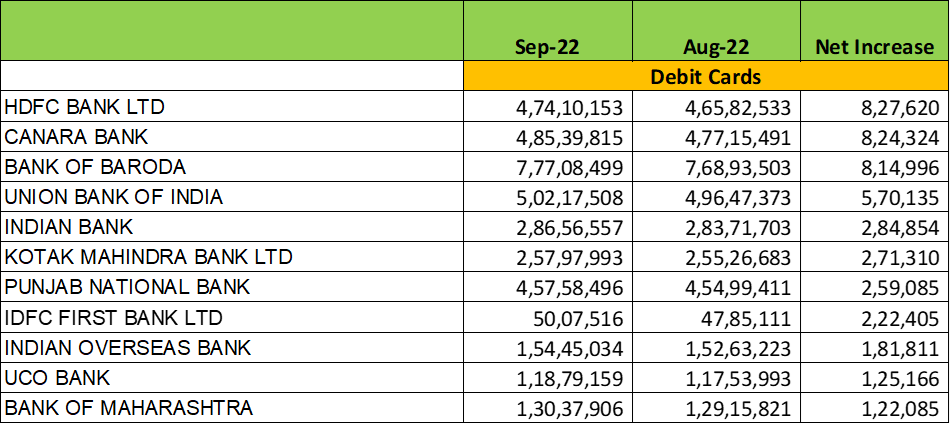

In terms of number of credit cards, debit cards, CASA growth, overall deposit growth the bank has surpassed my expectations. The speed at which the bank is scaling up is really commendable.

Q2FY23 numbers are around the corner and my estimates for the same are:

NII: 2920-2940 crs

Core Fee Income: 960-980 crs

Opex: 2775-2795 crs

Core PPoP(ex-treasury): 1090-1115 crs

Provisions: 355-370 crs

Core PAT(Ex-treasury): 540-570 crs

Core EPS(Ex-Treasury): 0.87-0.91

Core RoE(Ex-treasury): 9.9%-10.3%

In my view, the markets will be very positively surprised with the Q2 numbers and if the bank beats my estimates then we can see it crossing 70+ soon.

I’ve been through a few messages here and there on this long thread and I believe this has not been discussed. If it has been I apologise in advance.

Disclosure: I do have a small position in IDFC First bank.

The bank and its CEO first came to my attention after its merger. The bank looked decent and the CEO even more so. It is during COVID that V.V got a margin call. He did an interview at the time and that is when I realised that you rarely find people like that. Anyways I haven’t been able to go into much detail as many of you have, but I managed to do a back of the napkin 5 year valuation which is given below. Now, I’m aware many of you might not agree with the method I used and that’s fine by me.

I waited for a while before I made a position here to see if the management walks the talk. Found them very reasonable and bought a part of the business about 3 months ago.

My thoughts are in two parts:

PART 1

Does this bank have the potential to be the next kotak bank?

If yes, can you please share your (personal) conservative estimates both for the bank and the industry? (I would rather not take the estimates in articles written either by journalists or sell side analysts)

If not then why not?

What would be the reasons or circumstances under which the bank may fail?

I do believe the management has a long term approach - shooting one bird at a time. The addressable market in India is fairly big yet competitive. I’m unaware of the behaviour that is incentivised and penalised in the culture of the bank. I am strongly biased here, so feel free to go the other way.

PART 2:

I certainly am not an expert/veteran on Indian banks as many of you are. However, I did start to do an apple for apple comparison of the important parameters between IDFC First and Kotak (this is almost done I think). I only know of Aditya Puri and Uday Kotak so hypothetically speaking, let’s say VV is 75% or UK. So I could be dead wrong here as well for comparison. To be added for comparison were Federal bank and a few other banks who has funded assets of about 100,000 Cr – 150,000 Cr. Attached is the excel for the same. Would anyone be willing to develop this any further and share?