I think VV has a different game plan when building a Business which is not traditionally followed by most of others and hence not understood well or accepted Initially by the market.He did the same in Capital first.

His Style is build a sustainable model which is scalable for a long period.This model requires front loading of cost and it creates temporary depression in the profitability numbers.

This also creates doubts in the minds of many and the environment around is negative which I presume is the reason many leaders dont want to follow such models which creates lot of pressure for them.

The real product will only emerge later once the Model is built and ready to fly.

The Bank has completed the pain period and the journey has just began.The profitability numbers will surprise many since the Operating leverage has kicked in.We need 2-3 quarters of results for all to believe.

Interesting times ahead !

I am not a believer of predicting future in numbers …We should keep an eye on direction and momentum…and if any one of these go wrong then we can always exit the stock…

.

but still if we want to get a rough idea then my assumption would be like this,

going by current QoQ growth and applying a 25% growth on that IDFC First may increase its AUM by around 1.20 lakh crores in next 3 years…considering a conservative profit of 9000, the bank will need to raise 6000-7000 Cr. …at average price of 100 Rs number of shares will increase to 690 crores…

With a profit estimate of 4500 Cr. for F.Y. -25, EPS would be 6.5 rs and with a P/E of 30, stock price can be 195-200…

.

Bank can also use Tier 2 capital and AT-1 bonds to raise capital adequacy levels if I am not wrong, V vaidyanathan has mentioned it in recent past.

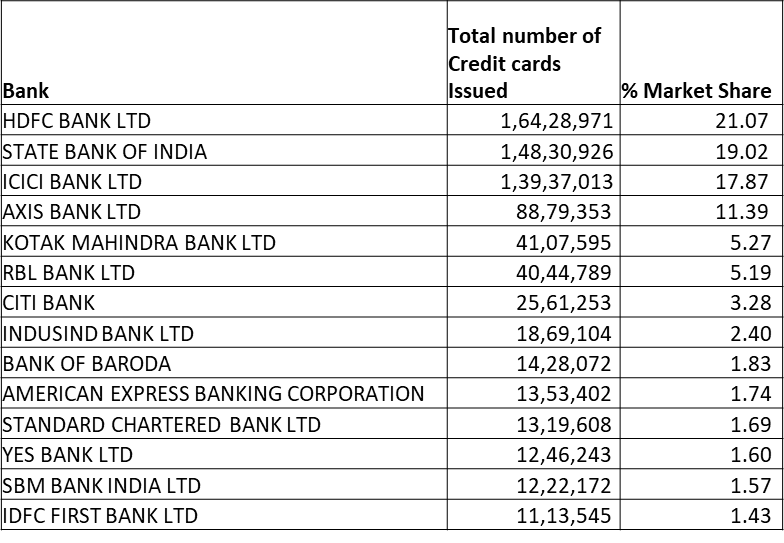

Bank Monthly account data is out.IDFC has continued his growth in both Credit and debit cards. Interestingly many banks have seen a month on month degrowth on both Debit and Credit cards.These includes some of the top banks.

Implementation deadline for above is extended to 1st October.

Some prudent banks might have already gone live with those rules and might have absorbed the impact.

October ending disclosures should give a better picture on #Cards market share for banks & True Average spend per card numbers.

For now, it makes sense to track growth based on spends market share.

I think, the icing on the cake has been the surge in Deposits ( up 36 pc YoY !!! ) for IDFC First. This in an environment when most banks are struggling to match deposit growth with credit growth. This to me is a very very encouraging sign.

I am invested since 2 years now and am very confident of its performance.

The real challenge/quest is that the future cash flow and revenues are never in sync hence either thing will slow down gradually or go to the moon, we never know.

Please note there is a good amount of visibility to IDFC First Bank CC business as well and they are competing well with ICICI, HDFC, and SBI in this space. Soon we should see some contribution from this side to the top line.

My real question is, given the conviction, when to add more qty? Is 30s level a thing of the past so we should accumulate more in 40s? or anyone feels, the worst is still not over and we can see 30s level again sometime in future.

Going by the business momentum, I think its headed north. The joker in the pack shall be the figure of fresh slippages. If fresh slippages are under control, then combined with scorching credit and deposit growth … 30s and even mid 40s should be a thing of the past.

But the final verdict will only be out with Q2 numbers.

During the Amazon, Flipkart sale, we saw offers from SBI, ICICI, Axis Bank Cc. In the second leg of sale, the offers are from Citibank, RBL and hdfc bank. So this month we can see these bank CC gaining more mkt share than IDFC first.

So how does IDFC First increase their CC issuance? Is it amplified due to low base? Can it grow the same % once it achieves bigger scale?

As a idfc credit card holder and a credit card fanatic,i dont use my idfc bank card at all ,the rewards have reduced and now there are redemption charges as well starting this month.

I have the card only because it’s free and there are offers once in a blue moon.I also don’t understand there current strategy of credit card business of offering lower interest to high cibil users as they really don’t care about interest rates because they always pay on time, to me it feels like a classic example of if it ain’t broke why fix it!