In general banks have a secular growth story in a country like India. Key monitorables for investors are the soft aspects of the bank. For example, if we carefully observe IDFCF bank, the risk on balance sheet has been completely transformed and reduced in last few years. Earlier MSME and MFI were huge part of the balance sheet. Now, mortgage and consumer loans are a much larger part.

See this part of this post.

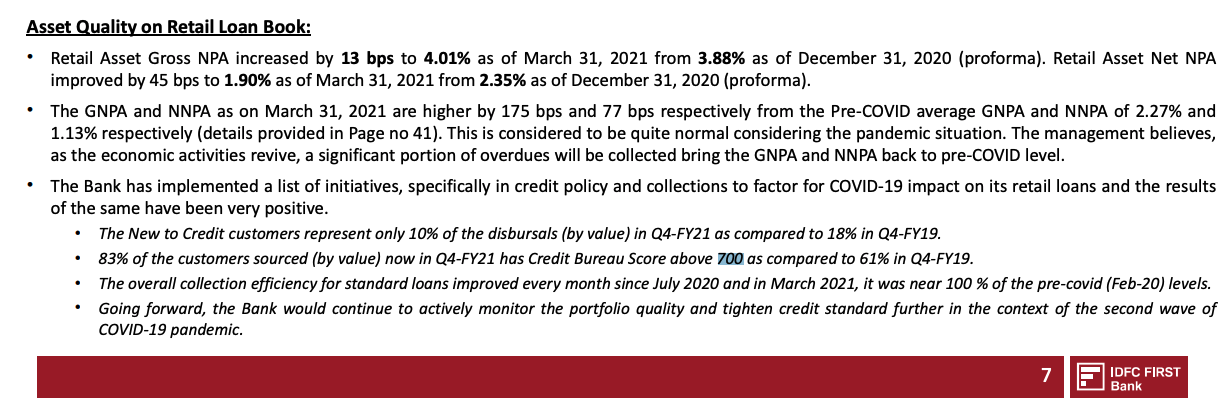

In addition everything they have said this quarter wrt how they have increased lending standards, more loans to 700+ credit score, less loans to first time lendees,

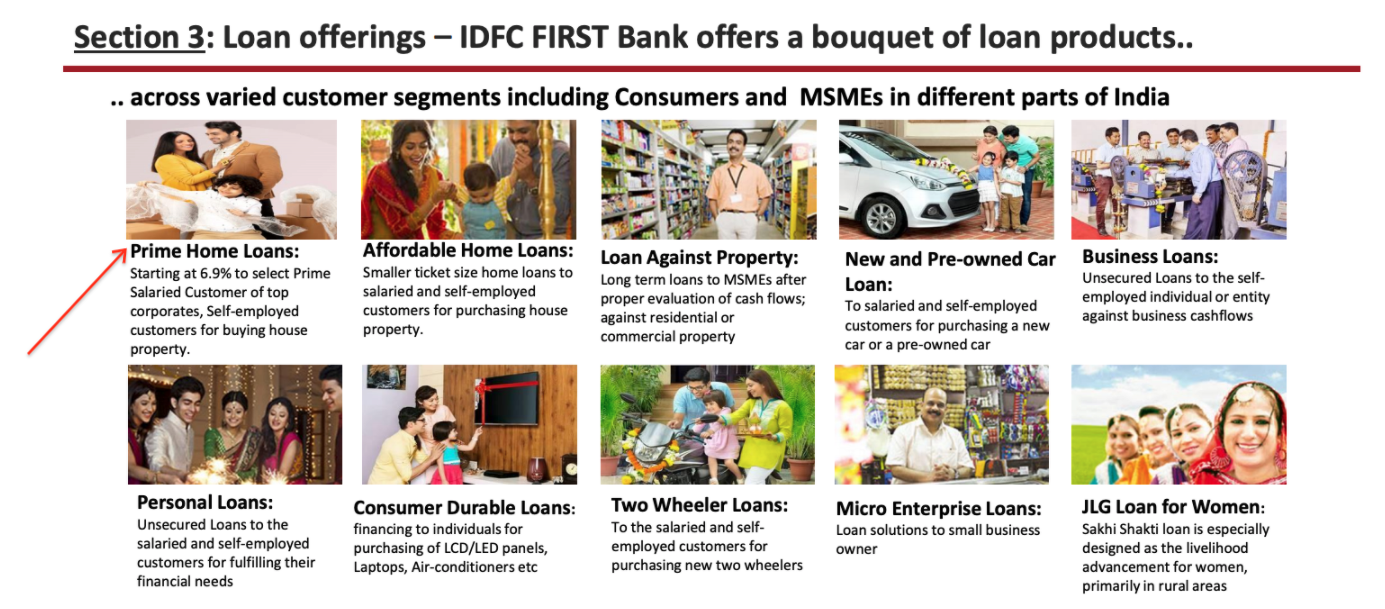

home loans to top corporate clients at 6.9%,

cred tie up (see post quoted below), are all steps towards reducing the risks.

One has to understand the transformation of the balance sheet to see where the puck is moving. NPA numbers trend has to be understood. Not just this Q and next Q.

I have been tracking and been invested for more than a year. Conviction and research was also there for more than a year. Since Dec-19. My only regret is I should have loaded up more in Mar-20. Did that too, for many months my average buying price was 23-25 rupees. But second round of large loading up I could only do in 50s. Should have loaded up lot more in 30s. So if there are many gap downs and stock price tumbles next week because GNPA did not improve as much as investors were expecting this Q, that would be a buying opportunity for a long term investor for me.

Coming to Rafi’s questions:

I don’t understand how provisioning can worry anyone. Banks got covid shock which only revealed itself in 1 Q due to moratorium. Provisions have to be created slowly, over time. More provisioning is good. It reduces the NNPA number and cleans up the balance sheet. The gap between 4% and 2% is the provision. The 2% NNPA will move to 1% as they provision more and more every quarter.

Banks have very broad leeway when it comes to the P&L statement. The Bank P&L statements are quite useless IMO. Profits are only an accounting item. How bank treats standard assets is up to the understanding of the bank. When they took 50% provision proactively for VI, did investors cry about it? They did. Now that VI looks much more set to not go under, is still a current account and hopefully their bonds are trading at a higher market value (haven’t verified this), bank is reducing that provision slowly (and also adding larger covid provisions). I see absolutely nothing wrong with that. In fact all the VI provisions have been repurposed for covid provisions which is very healthy IMO.

This has always been the case. I have explained in detail in the SIP document post what is happening in the retail segment.

Please read this part carefully.

In summary, I think if someone were to ask me top 3 most important things to track in a bank, they would be:

- management

- management

- management

Numbers are only a way to judge whether management is walking the talk and hence secondary in the case of banks. If someone were to put a gun to my head and force me to track numbers, I would track the NPAs, the NIMs and the Cost to Income Ratio. The trends in all 3 are positive IMO and hence this remains an investment for me.

Disc: largest position in PF and so I am heavily biased. This or any of my posts are not investment advice.