He is the master of goal setting ![]() . In Q3 2024, he stated that pain would be in Q1 2026

. In Q3 2024, he stated that pain would be in Q1 2026 ![]() , but now he is suggesting that meaningful recovery will only occur in Q4 2026 .

, but now he is suggesting that meaningful recovery will only occur in Q4 2026 .

1 Like

As of date this bank’s results should be seen on a QoQ basis rather than YoY as the bank is in a recovery phase.

RoA: .53% from .36%(q425)

RoE: 4.9% from 3.3%(q425)

OP: 2239 cr. from 1811 cr.(Q425)

Npa and Gnpa both stable

Last year september quarter eps base had become very small just .28 which shows from jul-sep 26 quarter the yoy EPS growth will be almost 100% or above(considering eps of .62 same as june 26 quartet) due to smaller base.

In my opinion this is the right time to buy this stock or stay invested

P.s. i am invested at the level of 73 since August 24

7 Likes

Although it does not make any personal difference to me as I will stay invested for at least 3 years more even if price goes further down. But I do feel concerned for those when I see some people getting jittery. In my opinion it is just the wrong time to divest. But then people should go by their own research and assessment. So far the bank has not made any serious mistake and taken plenty of good decisions. Bank has faced systemic issues on which they had little control except to take sensible steps to solve those issues.

3 Likes

As the Loan Book grows, Bank will have to increase Provision to keep PCR healthy, currently at 72.3

Loan book grew by 21% YoY

PPOP grew by 19% YoY

more importantly it grew 23% QoQ, shows a turnaround of sorts.

Provisioning also significantly up 67% completely destroying a good quarter. Due to MFI mainly. But that seems to be finished mostly due to SMA looking good.

All we need is a one good year, without MFI, and we can expect a 2x

7 Likes

Don’t know how stock will react in a day or a week, but for sure everything bad is already factored in, the stock should do well in coming months.

7 Likes

yes completely agree. I think 65 to 75 is good range to accumalate. we can see good rally in next 12-18 month period.

4 Likes

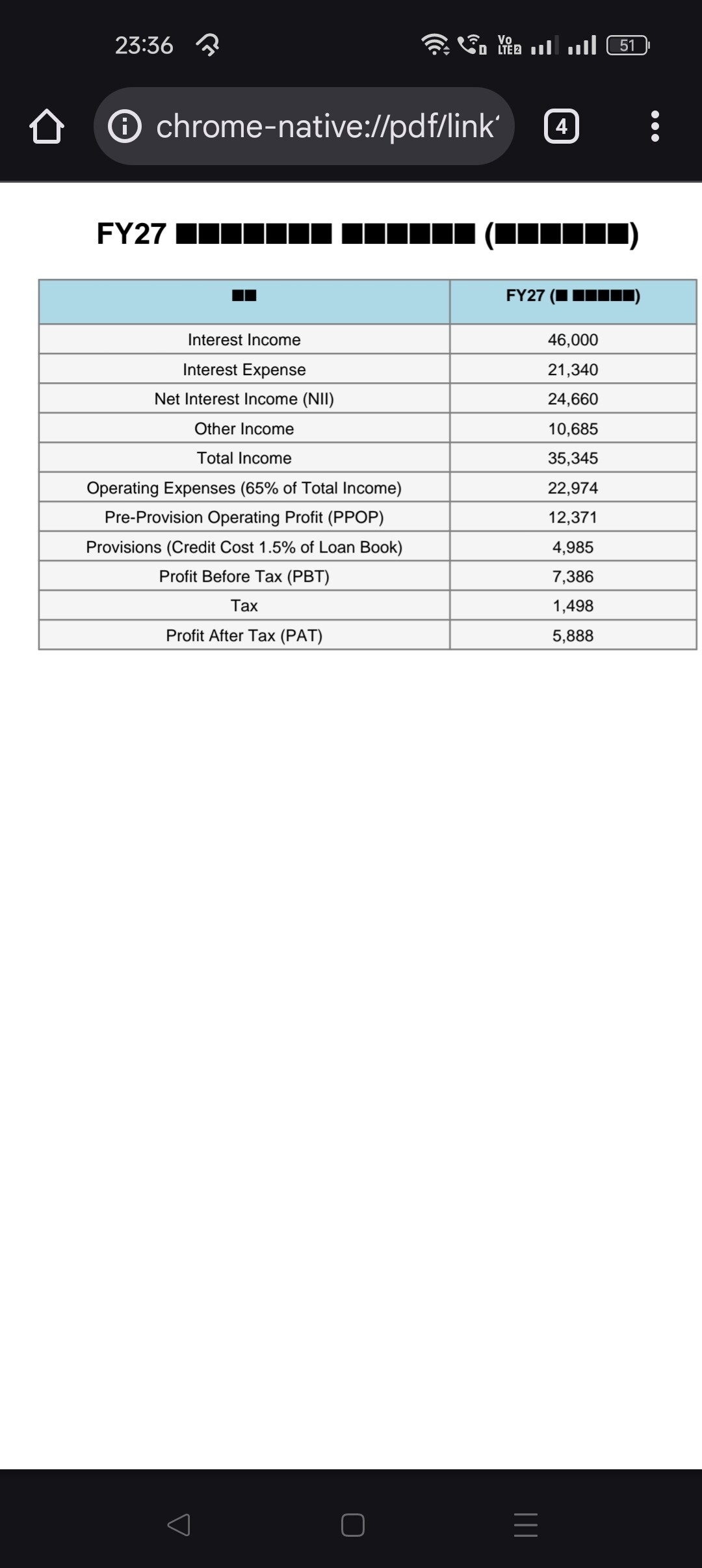

Yea we can expect PAT in range of 3k-4k for FY27

1 Like

The bank has been given a profit target of 12000-13000 crores by FY29, if it will be at a profit of 4000 crores till FY27, then how will it reach a profit of 12000-13000 crores in the next 2 financial years

it won’t reach that target. if you noticed, they have removed that guidance 2.0 from presentation when this microfinance issue started. By FY29, i think maybe we can reach 6-7k PAT.

Disc: Invested

1 Like

That’s right, I believe that microfinance issue has come up…but in guidance 1 also there was problem of Covid 19 but except cost to income.all other parameters were achieved If cost to income were achieved then ROA and ROE would also have been achieved… yes, guidance 2.0 has been removed from presentation but loan book growth and deposit cost are running as per guidance 2.0… if bank cost to income is brought down to 55% and credit cost to 1.5, then as per my calculations with 20% loan growth, PAT can be reached up to 10,000-11,000

3 Likes

Yeah loan book growth can be achieved by anyone..thats y we are suffering now. I can’t imagine how VV such a season banker never thought of CGFMU when giving out these micro loans? i mean what was he smoking? …all he said was he made a mistake and never thought of it. Anyways don’t even imagine of a cost to income of 55% until maybe after FY 32 ( wild guess). That’s why he keeps peddling story of we are in for the long term. Anybody guess what will be the equity share capital in FY32? i guess maybe around 1000 crores…

3 Likes

It is correct, VV has admitted that he has made a mistake… it is a mistake but he has also accepted it… can you tell why it is seeming that by FY32 the cost to income will be around 55%… because I can see some things clearly in the next 3 years, firstly now the branch does not have to be made 4-5X, so a good cost cutting can be done from here.

secondly, the credit card business had started from 2021, it has now come into profit, so from there instead of loss there will be a contribution in the profit and the last banking operations and fixed cost will not jump as much as it happened in the last 5-6 years… in Looking at everything, it seems to me that cost to income will easily come down to 55 by FY29 or FY30 … plzz share your view??

4 Likes

I think since they’ve had a good track record in meeting guidance 1.0, and even managing capital first before that, there is a good chance we will see them hit guidance 2.0 around FY30. (Could be 12-24 months late as well). Opex growth will come down as you pointed out, credit card biz and other new businesses will start showing good profitability, which will also aid in PAT growth. With the deposit growth at good rates, the cost of funds is likely to go down, which could help them make more money and also give loans at lower rates, leading to less NPAs. Additionally, if I’m not wrong, they are planning to extinguish the bonds in the coming years, and if these provisions (MFI) aren’t recovered, CGMFU will cover for 70% or smth, which will directly flow into PAT.

5 Likes

In 2018-19, a garbage bank has been taken in such a situation today. We should have a little trust on VV… I may be wrong but we should not look into the track record of its capital first company. In the same situation, they had taken it to a very good level…

disclaimer- I have invested from the low level in 2020

2 Likes

Yes Ravi, your right but i want to keep myself little more conservative and had come up with those numbers. Usually he will miss some parameters of his guidance by a year or so as they are guiding for C2I of 65% in FY27 which i feel they might miss and from there to 55% in another 3 years i doubt. I am no financial analyst and i want to keep myself grounded. And like you i have invested from lows of 2020 and i have good margin of safety and i am happy with it. What do you think of the equity dilution? and large shareholder base? due to these last two reasons, i doubt i want to be invested in this share after FY30..

2 Likes

I also started investing from lows of COVID. And still holding…From 20s , it came to 90s and now consolidating. There are two things…VV definitely has changed things here, but also there are things that he comes up with time and again… excuses which even for investors who regularly follow can’t predict. My take would be to be in the boat , but not booking too many seats here. Will be very cautious on the allocation here. Thats the only thing retail investors can do.

1 Like

The activity in this thread is quite telling.

I believe that banking is a game of survival. If you survive and grow, you tend to make good profits.

From close to nothing, this bank is bigger than Kotak was in FY21.

2.5 Lcr advances vs 2.3 L cr or so, with higher CASA but lower C/D

If advances, and more importantly deposits continue to grow AND the bank continues to survive; we are looking at a growth similar to business growth.

Terminal Value and blowups matter.

Ask Yes Bank or Indusind shareholders.

Essentially, the banking segment peaks out at 15-18% ROE; and hence, the odds of making more than that are low.

3 Likes

I am not a financial analyst, but as far as I have been observing the bank from last 5 years, I feel that the bank has crossed many big hurdles - legacy loan, initially operating expenses, then MFI problem… We people have been seeing the same problem from last 5-6 years, for this also we have become very hopeless…Mr. Raju Ji, I want to look at the bank from the market cap point of view rather than from the equity dilution point of view.. Today, IDFC FIRST BANK has earned interest at Kotak level in FY21. I am not saying that IDFC FIRST BANK should get the valuation of Kotak Bank, but in future when IDFC FIRST BANK will become equal to Kotak Bank on many parameters like cost to income, interest expense ratio and credit cost, then this bank will show better profitability than Kotak…

9 Likes

Q4FY25 PPoP is 7069 a generous growth of 25% be assumed, then in two years we land at 11045, still far from the number in the Excel sheet.

As far as my expectations go, I believe Banks are not going to do too well for next few quarters.

Last quarter we saw

Sharp increase in Provisioning QoQ, signals distress.

Icici 104% ![]()

Hdfc 352% ![]() (YoY 450%)

(YoY 450%)

Axis 190% ![]()

Idfcfirst may fare a little better cuz it addressed the pain early.

I believe, Next year this time we should see this stock run a few strides.

6 Likes