Good investment depends on entry price and business performance.

There was lot of pessimism about stock price and company’s prospects around mid March when stock traded even below 53, very close to its book value. It has delivered good returns from that run from 55->78.

Buying this bank at Book value will be a good bet. At 1.45 P/B, expectations are certainly higher now. Most of the returns from last 4 months have come from multiple expansion. With expected growth in BVPS from earnings and that fueling further higher P/B ratio, higher returns than earning growth are possible.

I am a passive investor and haven’t run a business let alone heavily regulated business like banking . I was bit surprise by extent of the equity offerings but large fund raise definitely removes uncertainty related fund raising over next 2-3 years. I will give management latitude in operational and strategic issue such rapid product expansion, fund raise and even merger to acquire bank license.

It will be a candidate for trimming if P/B ratio expands ahead of earnings growth and alternative opportunities.

Thankfully my sense was right and it paid off to hold the stock from March till now. I have started taking partial exits as the price is much better than March and overall I’m not that big fan of this bank as a shareholder as I was till a year back

PS: No buy sell recommendation, please do your own research

Stock is at an interesting stage. Uncertainty is still holding it in check. The price jump in the last week happened after one single buy recommendation by investec. So it should be taken as only one more positive confirmation. If this Quarter results come out positive on 26 July ie net profit around Rs 1000 crore, then we may see another similar price rise of a few percent. In my opinion a sustained positive sentiment would require around 3 to 4 consecutive good quarterly results each coming at around 1000 crore+ net profit. Price would mature only after that. At present this stock is an unfinished work in progress product. Those who can wait should wait for at least 2 years. It is my personal opinion, and equity investment should be done based on personal research only. I am increasingly invested since 2018 so I could be biased.

imo, Q1 profit will be around 500-600 crores at best, as in annual report vaidyanathan mentioned that MFI impact will be there for 2 more quarters…

has anyone noticed any mention of guidance 2.0 and ROA of 1.4 by 2027 and PAT of 12000-13000 by 2029 in Annual Report released yesterday as I could not find it anywhere…have they withdrawn the guidance 2.0 silently…??

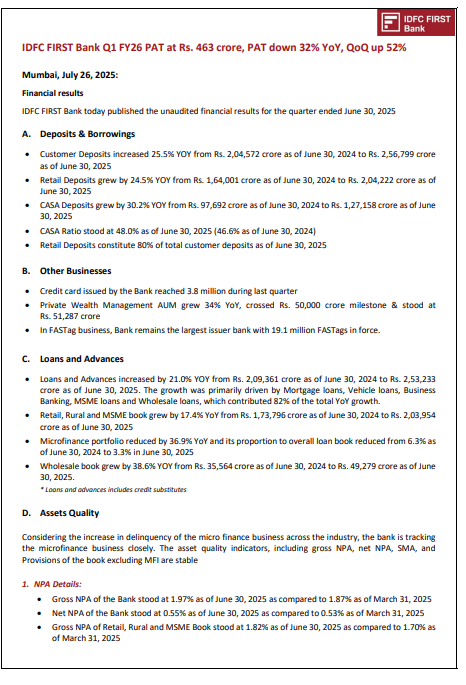

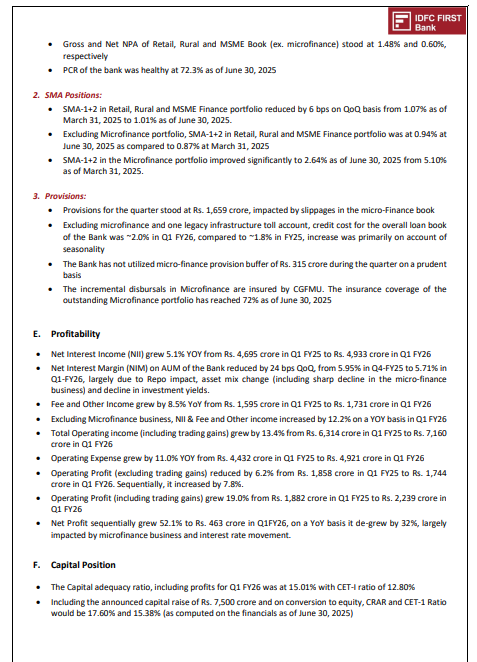

Standalone PAT 462.57 cr vs 680.65 cr down by -32.04% YoY & up by 52.12% QoQ

Customer Deposits rose 25.5% YoY to ₹2,56,799 Cr

Loans & Advances grew 21% YoY to ₹2,53,233 Cr

NII up 5.1% YoY to ₹4,933 Cr

GNPA 1.97% vs 1.87% QoQ & 1.90% YoY

NNPA 0.55%vs 0.53% QoQ & 0.59% YoY

Bank says:

Net Interest Margin (NIM) on AUM of the bank reduced by 24 bps QoQ, from 5.95% in Q4-FY25 to 5.71% in Q1-FY26, largely due to the Repo impact

Pretty bad results. Q1 26 PAT down 32 pc yoy. I have seen most banks posting bad results atleast trying to find a positive tone in headline in press release like “operating profit up 15%” etc.

Nothing here. The minimum they could do is to make an effort to be positive.

Yes, the results are disappointing. The provisions have increased ..

I am disappointed with the show. The management needs to take up the challenge & do something different. We have heard only promises telling “All will be good in coming days”

I aways felt that it is mediocre bank but all analyst, Fund Managers & influencers are bullish on this bank due to Mr. V. Vaidyanathan. I am invested just due to FOMO

I am invested in this bank for more than a decade due to my small holding of IDFC.. Frankly I have not made any decent returns till now.. but I have not lost capital either,

The primary fact remains that, over the past 5/6 years they have built a public facing bank with top notch tech stack, increased deposits at a much greater pace than most competition, nurtured decent voulume of Fastag deposits and Cards businesses , suffered several systemic setbacks within this period and are communicating not so sweet facts about business situation continuously.. Afterall doing business is not easy especially if one does ethically as IDFC First claims..

Yes, It has been a frustratingly long period of not so decent returns.. but somehow I am not seeing any reason to sell at this stage..If our country is expected to do well over the next decade then most banks will do well.. maybe including IDFC First.. this my opinion and is biased due to my exposure..

,

I was just curious as a new investor to understand that ICICI bank have given more than 20% returns in last 1/3/5/10 years and Still experienced investors are choosing IDFC First in spite of relatively low returns.

Finally everyone is in stock market to earn good returns.

For me , as a long term investor…It is like there are several boats available ( at varying price points) and you chose one in your wisdom and convenience.. you got on to it and your boatsman ( who can choose his own path) take you through the ride, So , sit on the boat in good faith.. Ups and downs are part of the process,… too much analysis and comparisons sometimes distracts your mind from enjoying the ride ,sometimes even through the rough patches.. keep sailing…if the boatsman abandons the boat midway without suitable process .. use the life jacket and swim to nearest available boat.. please treat this post in a lighter vein…

Now fear is opportunity lost. Many banks have given good returns in last five years.

Second concern is it’s number of shares size which is increasing a very fast pase. Lot of esops to employees and equity dilution.

I think even after some year however bank seems good eventhough uptrend in share price will very difficult .

Some one says that everyone benefited by bank depositor for better intrest and loan taker for easily approval except shareholder.