-

I asked Perplexity to “get your facts right” (it is of course limited by the quality of inputs it gets) - here is what it says - Perplexity admits inaccuracies

-

What matters in CAR is CET 1 (which is shareholders’ equity) and not Tier 2. Here is how various banks compare at Sept 30, 2025

The inadequacy of CET 1 of IDFC First in comparison to other banks is quite clear - leading to the biggest fund raise at the lowest cost of Rs 60 / share; lower than the July 2024 fund raise at Rs 80.63 per share - a discount of 25%.

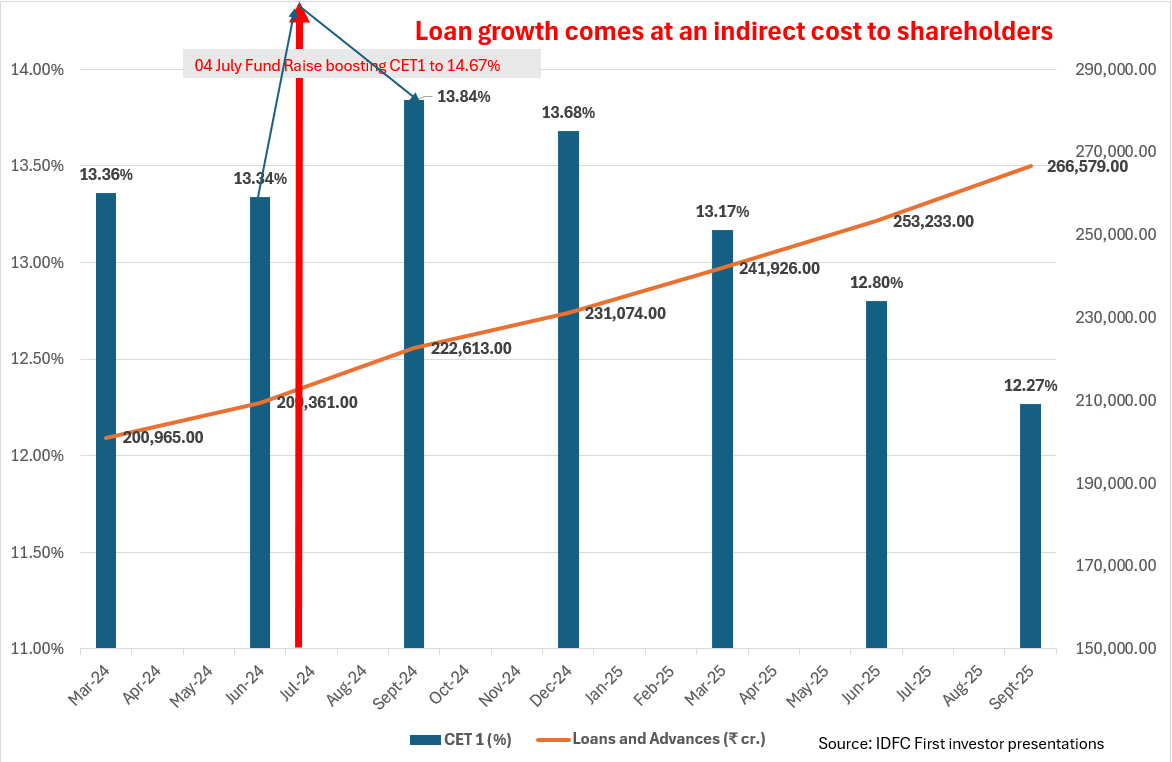

- This decline in CET 1 is on account of aggressive growth in Loans and Advances (L&A) but not in profits. This is despite a 04 July 24 fund raise boosting CET 1 to 14.67%

You may see that CET1 declines rapidly because IDFC First boosts loan growth even with deteriorating profits

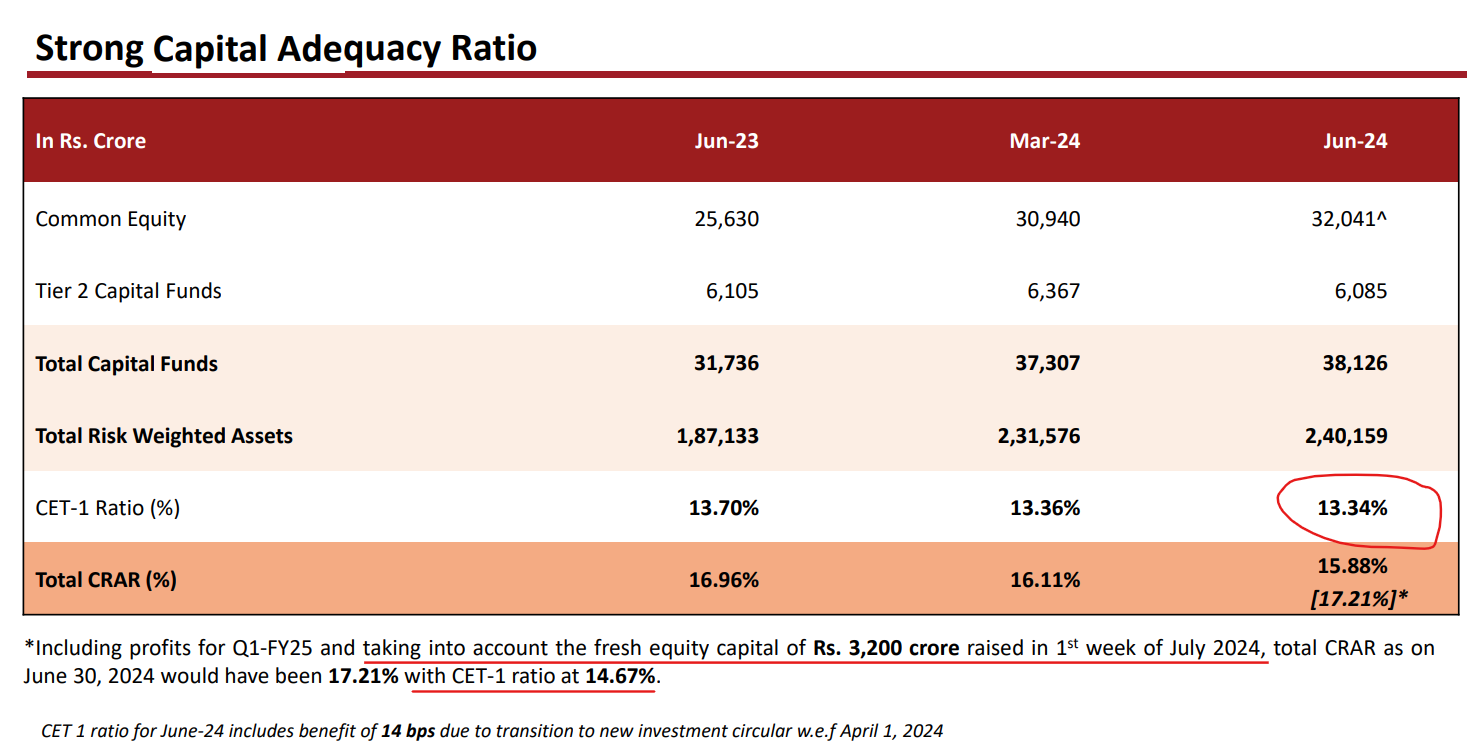

- Management will ofcourse bring future fund raises to current CET1 and say it’s so nice; like it did in July 2024 when it raised Rs 3,200 cr (snip below)

But CET1 deteriorated rapidly from that 14.67% to a dangerous 12.27% in less than 15 months!

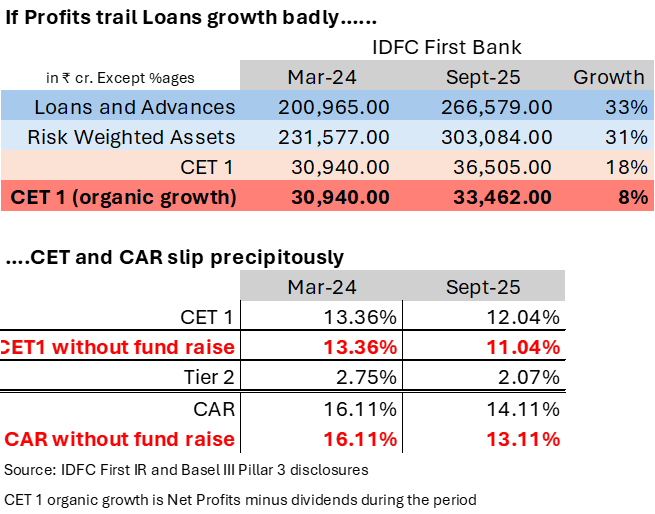

- To understand how aggressive L&A but tepid profits affects CET1 look at the table below

This necessitates fund raise, which IDFC First has been doing again and again.

- So what will happen if IDFC First grows its Loan Book by say 20% annually here on? The Loan Book will grow by ~ Rs 53,000 crores (and so will RWA mostly). To maintain its CET 1 ratio at 14.75%; the bank needs CET incremental capital at 14.75% of 53,000 crores = Rs 7,817 crores next year. Can the bank generate these kinds of after tax profits? If not, then either the loan growth will have to shrink, CET 1 will come down, or existing shareholders face the prospect of further dilution!

To sum: Banks raising equity capital without appropriate profits, just to fund loan growth is bad for minority shareholders