Thank you @vivek_mashrani for starting this thread! Insurance financials are very different, and we are not familiar with it. I just started learning about them recently! Please share your views on the below point:

I noticed that the entire focus is of the company presentation is on GDPI, but the real metric that should be tracked is NEP (Net Earned Premium). GDPI is the gross premium earned, but you can re-insure the policy, cede some premium and reduce the risk. NEP is the premium earned on the risk you are bearing, and hence the real indicator of your underwriting efficiency.

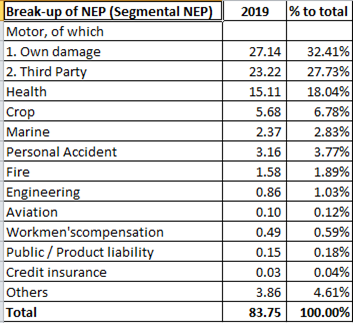

For ICICI Lombard, the picture looked like this:

Thus, ICICI Lombard is primarily a Motor and Health insurance company which in 2019 comprised 78% of the total NEP. This share must have gone up even further this year I guess since they have stopped crop insurance which was no. 3 last year with another 7%.

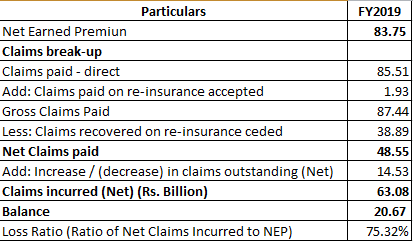

From NEP, we should deduct Claims, to see what the result of the pure underwriting operation is:

This is the figure (Rs.20.67 billion) that should be tracked rather than the GDPI. From this, if we deduct Agent’s Commission, we get the profitability of the core Insurance operation.

I was surprised to see so much emphasis on GDPI and almost nothing on NEP. It is easy for someone to boost GDPI when they are going to anyway re-insure a large part of the risk.

Is my understanding correct? Your views please!

(Disc: Have a tracking position)