ICICI bank came out with IPOs of 2 of its subsidiaries 3i infotech and First source solutions, in 2005. IPOs/ listing of subsidiaries etc is supposed to be positive for the shareholders as it is supposed to ‘unlock value’ by giving an exit route to those who want to sell their holding in the subsidiaries and also determine a fair value / market price for the shares of the subsidiaries.

Now, as far as I can remember, I did not get any shares of either 3i infotech or First source solutions either free or on a preferential basis. So value unlocking, if any, was not there and I did not gain anything from the IPOs of those Coys.

I also think that the situation will be similar when the IPOs of Insurance cos etc will come to the market. So I said ‘better forget making any money on the side.’, meaning that listing of subsidiaries will not allow you to unlock any value.

@ yash_pal… I am just wondering…weather it is legally possible for the parent company to list its subsidiaries without giving out shares to existing shareholders???

@yashpal, how is it legally possible to not provide stocks in subsidiary, once they get listed?

If not stocks, same earning from subsidiary sale should get add onto parent company B/S.

Any views?

I have not checked rules of SEBI in detail but the rules after 1991, when CCI (Controller of Capital Issues) was abolished and SEBI was mooted, are vastly different.

I hope you can check the present rules of SEBI. It is no more mandatory to offer any fresh capital issue to existing shareholders as rights, so far as I know. There are also many ways to avoid rights issues.

Expects NPA additions to remain at elevated levels in FY2017

ICICI Bank conducted a concall on 29 April 2016 to discuss the financial results for the quarter and year ended March 2016 and prospects of the bank. Chanda Cochhar, MD&CEO, and NS Kannan, Executive Director of the bank addressed the call:

Highlights:

Credit growth

Bank has maintained the healthy loan growth driven by strong retail portfolio growth gaining share to 46.6% of total loans. The domestic loan growth stood at 16% at end March 2016

The net advances of the overseas branches declined marginally by 0.3%. In US dollar terms, the net advances of overseas branches decreased by 6.0%.

CASA deposits

Bank has improved CASA ratio to 45.8% with retail deposits share at 74% of total deposits at end March 2016.

The daily average CASA ratio was at a healthy level of 40.5%. Total deposits grew by 16.6% in FY2016 to 4.21 trillion Rupees.

Bank has improved distribution network of 4,450 branches and 13,766 ATMs…

Financial performance

The net interest margin declined to 3.37% in Q4FY2016 with the fall in domestic NIM to 3.73% and international margins to 1.62%. The non-accrual of income on the higher slippages impacted NIMs by 10-12 basis points. Further, the international margins in Q4FY2016 were also lower on account of bond issuance expenses and excess liquidity during the quarter.

Retail fees grew by 13.0% constituting about 64.8% of overall fees in FY2016 up from 61.0% in FY2015. Corporate fee income continues to remain impacted by subdued corporate activity.

Treasury recorded a profit of Rs 2190 crore. Following the receipt of requisite approvals, the Bank completed the sale of 9.0% shareholding in ICICI General to Fairfax Financial Holdings and 2.0% shareholding in ICICI Life to Temasek. The aggregate profit from both the transactions was Rs 2131 crore.

Other income was Rs 707 crore. The dividend from subsidiaries was Rs 473 crore and the Bank had exchange rate gains relating to overseas operations of Rs 261 crore in Q4FY2016.

The bank is holding substantial value in subsidiaries. Insurance holdings are valued at Rs 33000 crore based on concluded transactions and there is further significant value in other domestic subsidiaries.

The significant value creation in the ICICI Group has been demonstrated by recent transactions in insurance subsidiaries. The Board of Directors of the Bank has approved sale of a part of its shareholding in ICICI Life through an initial public offering by the company, subject to market conditions and necessary approvals. The size and other details of the offer would be determined in due course.

Capital adequacy position of the bank was strong with Tier I ratio of 13.09% and total capital adequacy of 16.04%.

Costs

The cost-to-income ratio was at 34.7% in FY2016 showing improvement from 36.8% in FY2015. Excluding the positive impact of sale of shares of ICICI Life and ICICI General, the cost-to-income ratio would have been 38.2%.

In FY2016, the Bank added about 6,239 employees primarily in front-line roles in the retail and rural banking business. Non-employee expenses increased by 13.9% driven by larger distribution network and higher retail lending volumes.

Senior management would not receive performance bonus for FY2016. Performance bonus would however be paid to employees in the grades of Deputy General Manager and below.

Credit quality

Bank has completed the exercise of review of classification of cases highlighted by RBI in the Asset Quality Review, or AQR. Bank continue to work towards resolution and reduction of exposures through sale of assets and deleveraging.

As per the bank, the weak global economic environment, the sharp downturn in the commodity cycle and the gradual domestic economic recovery has adversely impacted the borrowers in certain sectors like iron and steel, mining, power, rigs and cement. Thus, the Bank has on a prudent basis made a collective contingency and related reserve of Rs 3600 crore Rupees during Q4FY2016 towards exposures to these sectors, over and above provisions made for non-performing and restructured loans as per RBI guidelines.

The gross additions to NPAs were Rs 7003 crore in Q4FY2016 compared to Rs 6544 crore in the previous quarter. Slippages from the restructured portfolio were Rs 2724 crore in Q4FY2016 compared to Rs 1355 crore in Q3FY2016.

Deletions from NPA due to recoveries and upgrades were Rs 781 crore and sale of NPAs was Rs 709 crore. The Bank has also written-off Rs 148 crore of NPAs.

The net NPA ratio was 2.67% end March 2016. The gross NPA ratio was 5.21%. The provisioning coverage ratio on non-performing loans was 50.6%.

The net restructured loans reduced to Rs 8573 crore end March 2016 from Rs 11294 crore end December 2015.

The Bank implemented Strategic Debt Restructuring, or SDR, for loans aggregating about Rs 1200 crore in Q4FY2016. All these loans were existing non-performing or restructured loans. Bank has outstanding SDR loans of about Rs 2933 crore end March 2016. The Bank is currently considering SDR for additional loans aggregating approximately about Rs 500 crore.

The Bank implemented refinancing under the 5/25 scheme for loans aggregating about Rs 680 crore with the outstanding portfolio at Rs 4240 crore end March 2016. The Bank is currently considering 5/25 refinancing for further loans aggregating approximately Rs 750 crore.

Bank’s strategic priorities for FY2017

On Portfolio Quality, bank proposes to proactively monitor loan portfolios across businesses, improve credit mix in favour of retail and higher rated corporates, reduce concentration risk, and resolution of stress.

On Enhancing Franchise, bank proposes to maintain digital leadership, continued focus on cost efficiency, and focus on capital efficiency and further unlocking of value in subsidiaries.

Outlook

Bank target domestic loan growth at around 18% for FY2017, driven by about 25% growth in the retail segment.

Growth in domestic corporate loans is expected to be 5-7% given the Bank’s focus on lending to higher rated corporates and reducing concentration risk in its portfolio.

The SME segment is expected to continue to grow at around 15%.

The portfolio of overseas branches is expected to further decline in US dollar terms.

Bank would continue to focus on sustaining a strong funding profile with an average CASA ratio in the range of 38-40%.

The yield on advances would be impacted in FY2017 driven by the shift in the loan portfolio mix towards secured retail and higher rated corporates, reduction in yields where exposure is migrating to stronger sponsors and non-accrual of income on the higher level of additions to non-performing assets. Bank expect NIMs for FY2017 to be about 20 basis points lower compared to the Q4FY2016 level.

Bank targets double digit growth in fee income in FY2017, led by retail fees. The overall fee income growth would depend on market conditions, particularly activity in the corporate sector, as well as regulatory measures with respect to various components of fee income.

The Bank would continue to focus on cost efficiency, while investing in the franchise as required. Bank expect operating expenses to grow by around 15% during FY2017.

Bank expect the challenging operating and recovery environment for the corporate segment to continue in FY2017. Slippages from the restructured portfolio are expected to continue. Bank expects NPA additions to continue to be at elevated levels in FY2017.

Given the uncertainties around the corporate segment explained earlier, and the ageing-based provisions on existing NPAs, provisions are expected to remain elevated in FY2017.

Based on the current regulatory framework and accounting standards, Bank expect the common equity Tier 1 ratio to be above 11% till March 2018.

Would like to disclose here that while I had invested in ICICI at 230-240 and continued to invest as it fell, I sold off on Friday, as I think my thesis will take some more time to play out (bottoming out of the NPA cycle). The recent results did not give much confidence.

Although according to this article, I may have sold off too soon:

On the other hand, what else can a broker say when he is with clients

I’ve held a small position of ICICI Bank for close to a year now and fair to say I didn’t foresee the magnitude of NPAs that the market had always been suspicious of and was proved correct. I’ve felt like liquidating my position many times and even more so in the recent run-up as it’s around the purchase price. But there are a number of factors which have always helped me stay on-

2% div yield and it div/share only increase from here on (NPA recognition is mostly done and dusted)

Increasing focus on retail advances - 23% growth YoY for FY16 and a visible shift from it’s long term strategy of being a corporate lender

CASA Ratio at healthy and highest levels > 45% which should help increase margins

Gurjot

Perfectly valid reasons, which is exactly what made me hold on to the company till now, after results. Green shoots are there, but only just so.

Basically it is a trust issue now. With all banks going back on their pronouncements made just 90 days back and reporting awful numbers, I am no longer sure how deep the hole is. A case in point is the article below.

I still believe ICICI bank will give decent returns when things turn around, but the WHEN has been postponed farther out. I might have held on, but incidentally, I found a company to switch to, which triggered my sale. So it was a matter of relative attractiveness.

Just a point on the dividend - why should the bank, which severely needs to conserve capital, should declare dividends completely beat me, till I read the announcement that the senior management would forgo their annual bonuses. With the relatively large dividend compensating, who needs a paltry bonus of 5cr?

Request boarders to provide their views if ICICI BANK share holder will have any additional benefits while subscribing for ICICI PRU IPO.

Someone has mentioned that bank shareholders will not get any free shares against their holding in bank but why it is so, is it that the value which bank with this sale is getting will be invested in core banking and there will be indirect benefits to the bank share holder.

Further do anyone see that Government will be coming up with any legislative help for banks reducing their NPA.

Can Icici Pru Sail through ?? Such a big issue and no scope for investor making money… can we have views from valuepickrs… Also I have seen in past that when big issues come then market falls after the issue is fully subscribed…

@Mehnazfatima

Hi Mehnaz,

Following your TA for long and appreciate your understanding.

Could you please share your technical views for ICICI BANK after recent break out post results.

There was turnaround in ICICI bank @ 258 at the end of December 2016 on quarterly charts…since then its in uptrend…I think, from here on, the stock will take care of itself…does not require much monitoring…

If one looks at Peak RoA, Peak NIM or NNPA private promoter driven banks tend to do much better compared to other banks. This is simply because promoter has much more skin in the game e.g. HDFC twins, Kotak Mahindra, Yes Bank etc. ICICI bank is peculiar in the sense that there is no promoter despite being a private bank.

PSU banks show better Peak ROE simply because they are much more leveraged. So ROE in itself is not a very good metric to judge the bank. RoA seems to be better metric.

Again private promoter driven banks, show much better cost to income ratio compared to PSU banks or ICICI bank. Cost to Income remains a single metric upon which if ICICI and SBI improves, they can improve their bottomline.

For yes bank, CASA ratio is lower compared to other banks and hence higher cost of funds. As that ratio goes up, the funding profile will continue to become favorable to that bank.

Now coming specifically to ICICI bank, following are few points →

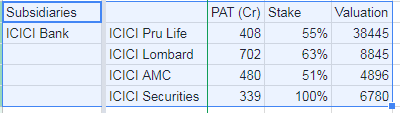

ICICI has some very good subsidiary businesses and I have put valuation on them above. For ICICI Pru Life, since it is listed, I have used share of market cap. For other subsidiaries, I have used PE multiple of 20. At current market cap of 2L Cr, ICICI has almost 60k Cr valuation in subsidies. The book value of ICICI is ~ 1LCr.

Based on some discussions, ICICI is looking to be very cautious in corporate lending book and trying to grow the retail lending book. It is unlikely, they will lend to another Vijay Mallya from here. Actually, cursory look at all the banks’ presentation shows that - everybody is focusing on retail book. If this caution stays for 2-3 years, banks balance sheet will continue to improve.

At the end of Q4 FY17, the NNPA of the bank were at 25451Cr and the restructured book was at 4265Cr.

There are short term upside triggers to asset quality due to - sale of Jaypee Cement to Ultratech cement. This will lead to up-gradation of 5378Cr from NPA to Standard quality. https://www.icicibank.com/managed-assets/docs/about-us/2017/jal-ultratech.pdf

Also it would be interesting to watch out how Essar case plays out.

The bank has indicated that in FY18, NIM margin will be around 3%. This is due to repricing happening in home loan portfolio and competition arising out of focus on retail book of all banks. Retail NIM might be under pressure for other banks as well and it would be interesting to watch out that number.

The tax rate (~13%) for FY17 because the proceeds from stake sale in ICICI Pru Life was taxed at 0% capital gains. The tax rate is likely to go up to ~20% for FY18.

The bank expects provision levels to remain elevated in FY18 and the internal watch list of bank for loans to below investment grade corporates is at 190bn Rs.

Overall, I expect the bank to report flat bottom line in FY18.

Hi Rupesh

Any plan for making any investment

With the resolution of NPA happening and unlocking of subsidiaries

This seems to be a good investment case

Any comments

I have taken small position, ~3% of portfolio, in ICICI bank over last 4 months at an average price of 282.

Following are some observations from my end -

ICICI Group is listing subsidiaries one by one & the sales proceeds are being accounted for in the books of ICICI bank. So subsidiary valuation can not be accumulated while looking at ICICI bank. I would look at it as pure bank + unlisted subsidiaries.

In banking company, what I like is - retail business is growing at decent pace of 15%+ & bank is focusing more on this segment. I also like that despite corporate loan book growing at < 10%, NPA ratios have largely remained stable. That is a very good sign of bottoming out of NPA troubles hopefully. Also I am hoping that they would be very careful in lending to corporate houses now & internalize the lessons. Anecdotal evidence seems to suggest this.

For a bank growing very fast, NPA ratios would continue to be low or decline - but that is not a good metric of risk presumed. Because if you are giving new loan, it is very likely that stress is not going to creep into that account for first 2-3 years & it might happen only after that. A better metric of measuring risk or underwriting quality is - to probably look at (NPAs for all accounts in particular year in which first disbursement happened/Total Loan disbursed in that year). This information might not be easy to get though. Simply ignoring incremental loan book in recent years while computing NPA ratio is also probably enough.

Disc - Invested, no transactions for last 60 days.

I have remained invested in ICICI bank & Q4 results were encouraging.

Few things that I liked are -

NNPA ratio has come down further to 4.77% on YoY basis despite Feb 12 RBI notification requiring classification of ~ 100bn Rs as non performing. The more important thing is the ratio of net restructured advances to net loans which was at 0.3%. Further the drill-down list came down to 47bn Rs. compared to 190bn a year ago. Further the bank is reducing overseas operations. There might also be some write-backs as IBC cases progress to resolution.

Over last few years the bank has focused on building retail assets in the midst of asset quality issues on corporate side. The bank has given target of 60% retail book by FY20 (currently at 56%) & I think they will exceed this target by 2-3%. The guidance of 14-15% RoE by FY20 is also very encouraging.

The bank is also trying to focus on revamping lending culture to corporates & that remains a key non-quantitative moniterable.

The bank owns various high quality assets through its subsidiaries like - ICICI Life, ICICI General, ICICI Securities etc. The standalone book value stands at Rs. 164 & this shall grow faster in FY19 compared to this year. The subsidiaries also provide support to valuation in my view.

Despite all this, value discovery in ICICI bank might take a little bit longer. As @Yogesh_s mentioned here, there is high correlation between GNPA & P/B value market is willing to pay. ICICI banks’ GNPA still remains high at 8%+. That being said, I have not looked at correlation between say NNPA & P/B value.

The Videocon loan amount remains non-material to business in my view but it might impact sentiments. The question mark over CEO would be settled one way or another over next 3-4 quarters.

Disc - I own ICICI bank & Indian Bank as a part of undervalued distressed bank theme. Together they form 5-6% of the portfolio. No transaction for last 60 days in both. This is not a buy/sell recommendation, please do your own due diligence.