Management interview dated November 26,2021

While H1 was subdued, underperformance seems to be temporary. Strong industry tailwinds should help in financials coming back on track.

Disclosure: Invested

Management interview dated November 26,2021

While H1 was subdued, underperformance seems to be temporary. Strong industry tailwinds should help in financials coming back on track.

Disclosure: Invested

This is an old article…reappearing again in this tread.

More than one year back it was posted in this same thread , which you can find if you scroll backwards…

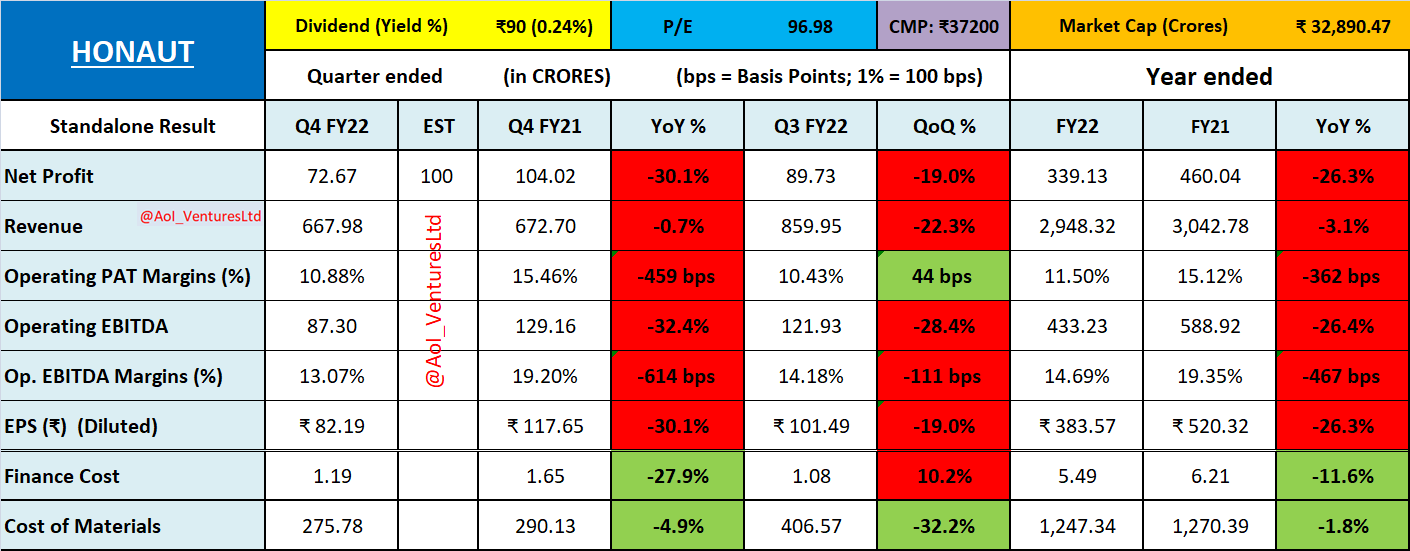

Q3FY22 Results

Wondering if you’re still tracking the stock…

with no concalls or continued brokerage coverage and hardly any information on order bookings or enquiries it’s difficult to make up mind on this company…

When capital goods cycle in upswing guessing why this stock is getting hammered… from 45000 to 32000

I had written to the Co about the lack of earnings related disclosures about two weeks back. No reply as yet. Have pointed out to them that the parent Honeywell Ltd has a detailed press release, a full slide deck as well as an earnings concall every Q, something which should be implemented at HAIL as well.

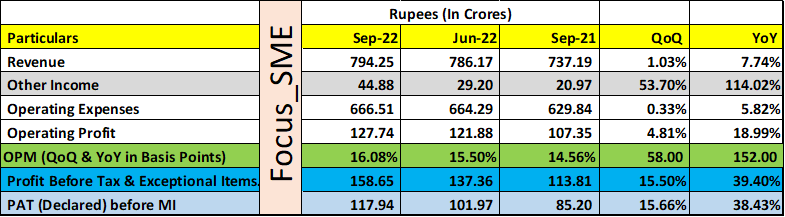

Sales at Rs 794 crs up YoY marginally but flat QoQ. Still way off the Rs 900 crs ~ levels it has seen earlier

Op Margin at 16% maintained – it has done 20%+ earlier

Other income up

In the balance sheet there is no new capex coming in, so FA is down due to depreciation kicking in

Inventory at highest in years at Rs 134 crs from Rs 98 crs in Mar22 and debtors from Rs 675 crs to Rs 835 crs have risen – why???

Is the quality of sales worsening?

Creditors consistently coming down – may be the reason for RM cost not rising – paying on time, cash discount

Stock is down 3%, 38550

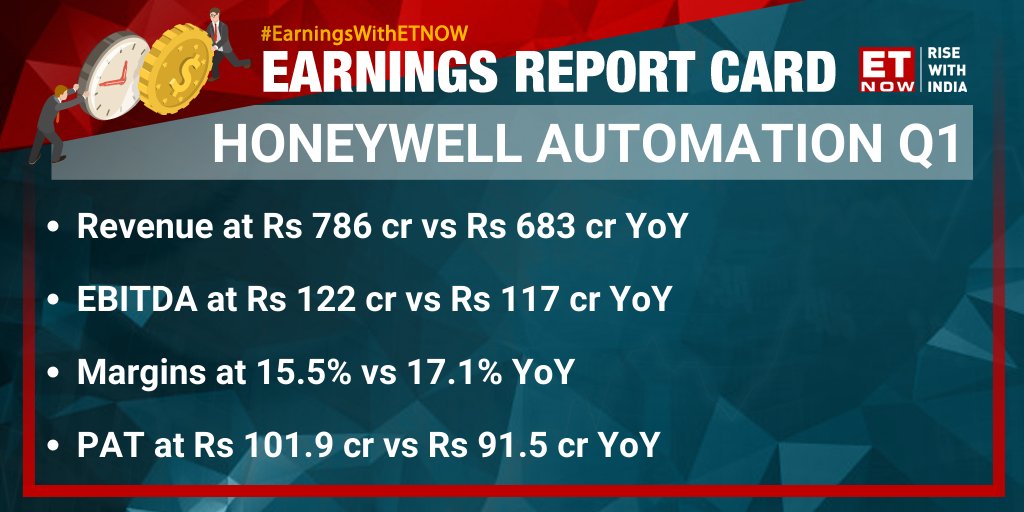

Management Interview

https://twitter.com/Nigel__DSouza/status/1593104472221548546

3QFY2022-23

FINANCIALS

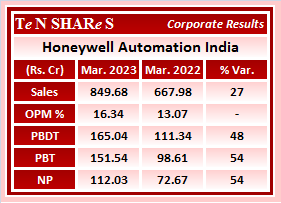

4thQFY22-23 Financial Results

FINANCIALS

dividend @ Rs. 95 /- sh

Q1FY22-23 RESULT

FINANCIAL

Q2FY2022-23 Quarterly Results

Financial

Notes from 39 AGM held on August 10.

HONAUT prioritize safety over everything at their workplace.

2) Posted a highest revenue ever of 3448 Cr indicating a 17% YOY growth.

3) NP growth of 22% YOY

4) Fiscal deficit is seemingly going down and is coming under control is a good indication for us and we see this as a good economic indicator for our Company.

5) India imports almost about 80 plus % of our oil and natural gas and therefore the price of oil and natural gas makes a big impact on the business environment.

6) The growing infrastructure and increasing focus on infra like Airport, Metro and hospitals is conducive for the good growth of the Company since all these infra projects require automation and company has the portfolio for that.

7) The other trend that can prove to be tailwind for the company is the manufacturing push. EV’s, Chemical and new chemical manufacturing facilities. HONAUT has the product portfolio to support growth in all these sectors.

8) In 2005, the revenue mix was 19% export and 81% domestic. For the last fiscal the revenue mix was 41% export and 59% domestic.

9) The export revenue pie comes from multiple countries and multiple product. Given the current growth environment in India, the company expects the domestic revenue PIE to grow.

10) The parent company HAIL sees India as high growth rare region but, that does not specially mean HONAUT. It has other legal entities in India too. The CAGR of FY19-23 was only 2% for HONAUT.

11) Growth in orders from non-Honeywell customers has reduced from 31% in FY22 to 11.9% in FY23. The slowdown is probably due to the bigger portion of the Company has what is called as the long cycle projects business. And, you book the projects which turn the revenue over maybe 12 months to 18 months, to sometimes even 24 months. And so if the backlog goes down, then to build that backlog takes time and therefore then the revenue starts coming back up again. What we saw in specifically the 2 years that were affected by pandemic, that the number of opportunities in the market had gone down and therefore the backlog was burned from the previous years and now we are in the phase of building that backlog. That’s how you see the growth rates in the order bookings that we have shared with you. And as we go along, you will see that the backlog that is being generated will turn into the revenue.

12) The growth in RE is also a big positive for the growth in the company is because RE such as wind and solar are not produced round the clock, btu the demand for energy is round the clock and thus increase in these resources require an increase in battery storage system. HONAUT has a Battery energy storage product names BESS which makes them cheerful about the growth in RE.

13) RE sources like LNG or natural gas are liquid in nature and their transportation required automation for which the company has a portfolio.

14) There is a new industry which is coming up, it is ethanol industry. We are blending 10% of ethanol into our petrol and it is going to go right up to 20%. And beyond that, there is a lot of talk about ethanol directly getting used as fuel or ethanol getting converted into other usable fuels. And so all of these processes and industries are going to need the kind of automation that your Company has in its portfolio so we can play in that economy as well

15) Hydrogen as another renewable energy basically uses an electrolyser which splits water into hydrogen and oxygen as we all know. And when you do that through this electrolyser, it needs what are called as programmable logic controllers or PLCs and again, that is there in our portfolio. And when hydrogen is either stored or transported, it needs automation and control and we provide that in that sector as well.

16) The overall growth in RE will require newer factories that will produce the photovoltaic cells, the PV cells, the batteries that go into EV. All of these factories that will either produce batteries or the PV cells will need automation, they will need the building controls, they will need climate controls, access control, the CCTV surveillance and stuff like that. So all of this is again, a part of the overall portfolio.

17) The company does not provide break up of revenue in a particular segment since it is diversified.

18) The headcount at the company has been flattish since FY 16. It is a good thing as per the MGMT, because they have trained the staff to be very efficient and with rev going up and cost staying in control. It can see better operating profit.

19) In terms of Pharm and life Sciences, company has a portfolio around fire safety and security which are used I plenty in the industries. In addition, these industries also use a lot of energy for which the company has a lot of automation. And in pharma company has product to keep electronic copies of batch record which are tamper proof so that the authorities can directly verify and trust the batch records.

20) Margins are getting impacted due to project mix. ( Company has higher in service than project based business). Higher Inflation cost has also impacted the margin. Also the revenue mix of import and exports affects margin. Company faces higher competition in the domestic market.

Overall, the company doesn’t seem to be very aggressive to me when it comes to increasing their revenue. Rather they seem to be focused on quality and let the market play out and decide who the strongest and valuable player. The competitive intensity in the space of automation has gone up considerably in the past few years which was highlighted by the management multiple times during the AGM. Given the broad portfolio the company has and the focus of Govt on RE and infra-Automation, company can potentially see higher growth going forward.

I had read above in the thread that there are multiple subsidiaries in India by the parent company which can potentially divert some sales to other entities and the lack of disclosure from the company coupled with only 2% CAGR growth of sales from FY19-23 makes it a little tough to take an investment decision. Although I doubt, the company is veering of any sales.

#Valuation

HONAUT is trading below its 5 year median PE of 78.5 vs current PE of 73.2. (Industry PE of 75.6)

Q3 FY 2023-34 QUARTERLY RESULTS

Financials

Great results saw a big upmove in the stock today