Honeywell Automation India Ltd, a part of Honeywell group, USA, is its Indian subsidiary working in automation and control systems in industries, buildings, automobiles etc.

- It seems one of the best for its job and as a result, it has some very prestigious and large clients.

- It faces significant delays in the collection of money from its customers. It has written off more than ₹100 cr of receivables over FY2009-2020. At any point of time, about 20%-35% of its receivables are more than 90 days overdue from the day they became payable.

- In the past, the company gave money to other group entities by inter-corporate deposits. Though in recent times, the company has not reported such transactions.

- The company reported inflated profits due to wrongful allocation of costs to projects in the past. The company acknowledged that it had weak internal controls.

2 Likes

Any company you deep dive for last 20 years, you would most probably find some issues or other at some point of time which is not desirable from the investor point of view …but one needs to see if

(1) The company is transparent in disclosure

(2) Who are the auditors…

(3) And if such issues are repetitive or one off case

(4) And finally how the company has delivered performance over years and what return you get over a period of time…

(5) Here at least the company has been maintain ing transparency, disclosing and recording all such events in annual report…and finally getting the accounts audited by a reputed auditor like Deloitte…

(6) The company net profit compounded @40% annually, compounded @30% return on stock price for investor annually, 22% return on equity over last 3 years …and I don’t find any serious corporate governance issues with the company over last 5 years…

(7) The stock valuation is reasonable when compared with many other MNC’s…

Discl: Invested long term and may be biased in views … But not married to the stock …will change my views if situation changes …

1 Like

Was wondering how the stock went up by 14% today ?

Due to Covid19 lockdown, market was expecting a complete washout for Q1 2021.

But the company reported a much better than expected performance… 4 % increase in revenue QoQ and a minor drop in net profit QoQ must have cheered the market and the fact that Industrial Automation seems to be playing out clearly to reduce human foofalls due to covid19…you may please read the previous views on Honeywell automation in the thread post Covid19 as to how Honeywell would play out during Covid19 and post Covid19 …and whether industries will go for automation to reduce human foot-falls…and whether offices , commercial complex , housing societies will opt for automation …in fact these seem to have started…even all indian IT companies are flooded with orders for Digitisation…

Yes securities seems to have raised a target of Rs 36000 for the stock…though it may be too early to say that unless someone is sure about the order book position…

Dicl: I like all MNC play in spite of lot of skepticism from investor community  … invested for the long term… May be biased…please do your own analysis before Investing.

… invested for the long term… May be biased…please do your own analysis before Investing.

1 Like

In the AGM meeting, Honeywell automation India has amended the Article of Association (AOA) of the company allowing it to Buy Back shares.

Earlier, as per the article of association, it was not allowed to Buy Back shares.

That could be one of the reason why the stock was trading 3-4% higher today…

But it is not that it would happen soon… or may not happen at all…

However, going by Q1 2021 result for an industrial automation stock during pandemic, it appears the company may be doing well as the industries may be going for automation to avoid human foot-falls…

Please read the last paragraph of the first page which extends up to the 2nd page.

https://documentcloud.adobe.com/link/track?uri=urn:aaid:scds:US:6e77a580-755e-4cf3-94b0-7bd56ce7ad85

Discl: invested… may be biased…Not a buy or sell recommendation …

Please do your own assessment before investing in stock market

1 Like

Promoters already own 75% which is the max allowed in India. What is the use of this provision ?

1 Like

Amending the Article of Association to enable them to buy back seems to have created a lot of confusion in the market…

In reality, Honeywell may not be able to buy back share, as they already hold 75%. The Securities and Exchange Board of India requires listed companies to maintain no more than 75 per cent public shareholding. So they can not buy back unless they want to Delist the company…

But why should they delist when they already have absolute control over the company… they take their own policy decisions …What will they gain? Rather they will have to spend a lot of money in buy back… They have already declared 750% dividend…

When they have a listed company, they create a brand in the market place…

Any views from members ?

Discl: Invested for the long term …may be biased…please do your own assessment before investing in stocks…

You could buy back with promoter participating so that the shareholding remains the same.

1 Like

Say 100% shareholding is 75% promoter and 25% non-promoter before buy back. Now the management proposes with buyback of 10%. Now if the buyback is participated by the promoter then 10% of the promoter shareholding and 10% of non-promoter holding both equally gets extinguished. So 75%-10% = 67.5 and 25%-10% =22.5. So technically 67.5/90100= 75% and 22.5/90100=25%. So both the shareholding remains intact.

Ps you could refer the buyback done by smartlink holdings for further reference

3 Likes

Honeywell India:

We’ve grown 2-3 times faster than India’s GDP: Honeywell

Companies are delaying large capital expenditure plans because of low demand and so on, Akshay Bellare said

For Honeywell India, Covid-19 has come as an opportunity. Akshay Bellare, India president, believes remote operations and data management are among the key areas of the company’s growth in the country. In an interview to Shine Jacob, Bellare lines up the firm’s roadmap in India and expects double-digit growth over the next five years . Edited Excerpts:

With a diversified portfolio, do you see Covid as an opportunity?

Companies are delaying large capital expenditure plans because of low demand and so on. When we go into the software domain, what we are creating is higher productivity. We are trying to enable our customers to extract more profitability for their assets. I think that makes our software very powerful. To my mind, those projects may get delayed because of demand challenges, but the technologies that we are offering–whether it is remote monitoring or Honeywell Forge–are more critical for customers during these times because you are maximising your asset utilisation.

What kind of potential did you see in the India market?

Each business is impacted in different ways. There are certain businesses that are growing during these times, while some others are facing challenges. That is the beauty of Honeywell’s diversified portfolio.

There are a lot of smart cities coming up. The government still is spending on infrastructure. E-commerce is getting much more significance. All of us now sit at home and more people are ordering things online. This means warehousing and logistics technologies are becoming more critical, where our Honeywell technologies are extremely useful. We have safety solutions concept and building solutions, all these sectors are offering good opportunities for us and we are pivoting into those.

In some verticals, like airline or oil and gas, there is a slowdown. In these, we see some challenges in the next six months. To me, it is about how we can pivot to areas that are growing rapidly for us. It can actually maximise our performance during these difficult times. I am positive about our ability to offer technologies where I see significant growth – for example, safe building, warehouse automation, remote operations, smart cities, data centre management, building management system and healthcare and pharmaceuticals. Honeywell as a whole is feeling good about the future and we will be able to weather the storm created by this pandemic.

Compared to your global revenue of over $40 billion, the Indian share is minuscule. What are your plans for India?

In the context of the amount of growth, if you look at Honeywell India, in the past two decades, we have grown two or three times faster than the GDP of the country. Traditionally, India has been a big part of the growth story for Honeywell. We have a very good track record here. Of course, the pandemic has given a bit of challenge for us, for all companies globally. The second quarter was difficult for all companies because of the lockdown. We are looking forward to things getting better in the next quarter. We see growth coming from certain areas where we are well-positioned to offer our services.

The future for Honeywell is bright. Our CAGR for the Indian market is going to be at least two to three times GDP growth. We just put together our strategic plans and when the country grows, we actually do better than twice that. We are looking at double-digit growth for the next five years.

With Covid becoming a catalyst for remote working, how is Honeywell adapting to this makeover?

In all sectors, including oil and gas, digital transformation is happening. I believe this pandemic has actually accelerated the transformation in operational technology space. Now, more and more importance is being given for digital transformation as more remote operation can be done without actually being at the location. We feel very good about remote operations that we are able to do as a result of our technologies. Similarly, Honeywell Forge increases the ability of workers to remotely connect, gather data, get information that can be put together by its powerful tool and that is why we are excited about it.

You mentioned about Forge. Honeywell recently had a tie-up with Cairn for their enterprise performance management software. What are the advantages of this?

Cairn was looking to digitise their workflow. They were going for digital transformation, largely driven by their desire to improve their productivity, brand efficiency and enable their workers to work remotely. We offer analytical software through Honeywell Forge – that provides real-time data, visual intelligence and offers secure cloud technologies.

When we talk about Honeywell Forge, it is an enterprise performance management system. This is for manufacturing, industrial operations. It brings together the equipment process and people and by doing that, provides actionable information. This allows us to monitor things on a real-time basis. When we think about Forge, we have to think about all different aspects of an enterprise – maintenance and reliability, efficiency and utilisation; how to optimise the output. Digitisation.ensures that data is collected from different systems and then be provided with insights. That is the objective of Honeywell Forge. It maximises, efficiency, effectiveness, safety and profitability for any enterprise.

5 Likes

Is this for listed entity, some unlisted entity or all Honeywell India?

1 Like

I am not sure ,but when I searched honey well forge which is their industrial performance management system mentioned above in HAIL annual report of 2019 -2020 and it’s missing.Honeywell-Annual-Report-2019-20.pdf (1.9 MB)

Honeywell Automation MD Ashish Gaikwad On COVID’s Impact & FY21 Outlook:

6 Likes

Does Honeywell automation have any benefits associated with electric vehicles adoption? Its parent US company seems to be heavily into automation of ev.

What about Honeywell automation if India adopts ev in the long term? Any idea?

Surprising, Honeywell hasn’t reported its results yet. Last year the meeting was on 22nd May 2020. Any insights??

Q4 Results Declared

Board recommended a dividend of Rs.85 /- (Rupees Eighty Five only) per Equity share of face value Rs.10/-each

3 Likes

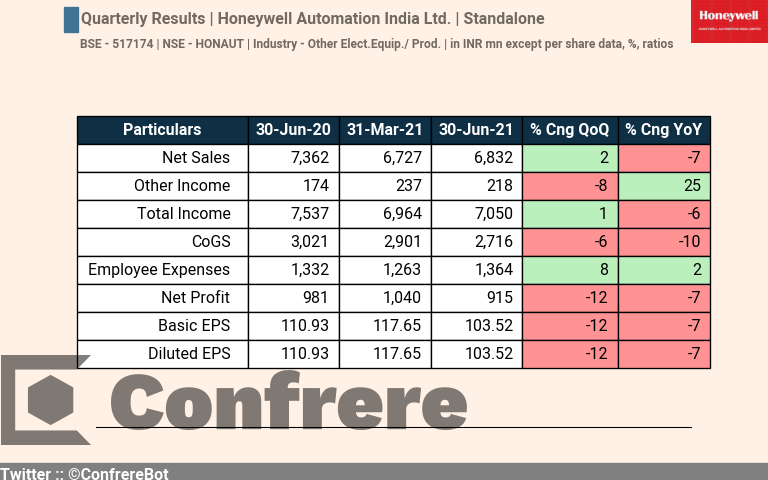

Source: https://twitter.com/ConfrereBot/status/1423291835905048582/photo/1

Qrtrly Financials June’21

Honeywell Automation Annual Report 2020-21

1 Like

Financial results September, 2021

Results have been subdued for the last few quarters. I was hoping for business to improve from this quarter due to general buoyancy in capital goods sector, good track record and relevant product portfolio. Also, commentary by MD in a TV interview in Sep 2021 was positive (link below).

However, Q2FY22 has been disappointment again. Is anyone aware of the exact reason?

1 Like

There is a dip in Revenue from operations as well as a buildup of WIP. These 2 combined is reducing the profit. But yet to find any detailed explanation.

In the notes, it was mentioned that Indian buyers are delaying their purchases due to uncertainty from multiple covid waves. Probably that explains the short term underperformance

Invested

1 Like