I too read that… But what the interest rate they are charging ???. If home finance co lending lend at 9 or 10 how the NIM will playout… Any idea…

You can check the UGRO thread for discussion on the co-lending model, it may help in having a better understanding.

1 Like

Bank will lend to NBFC or HFC which will get 80 of funds from bank and remaining 20% from its own fund… Pricing is upto bank and lending entity … Am i right??

NBFC : Will get lower cost of funds than in market

BAnk: Can meet its priority sector targets…

Good read on home first -

2 Likes

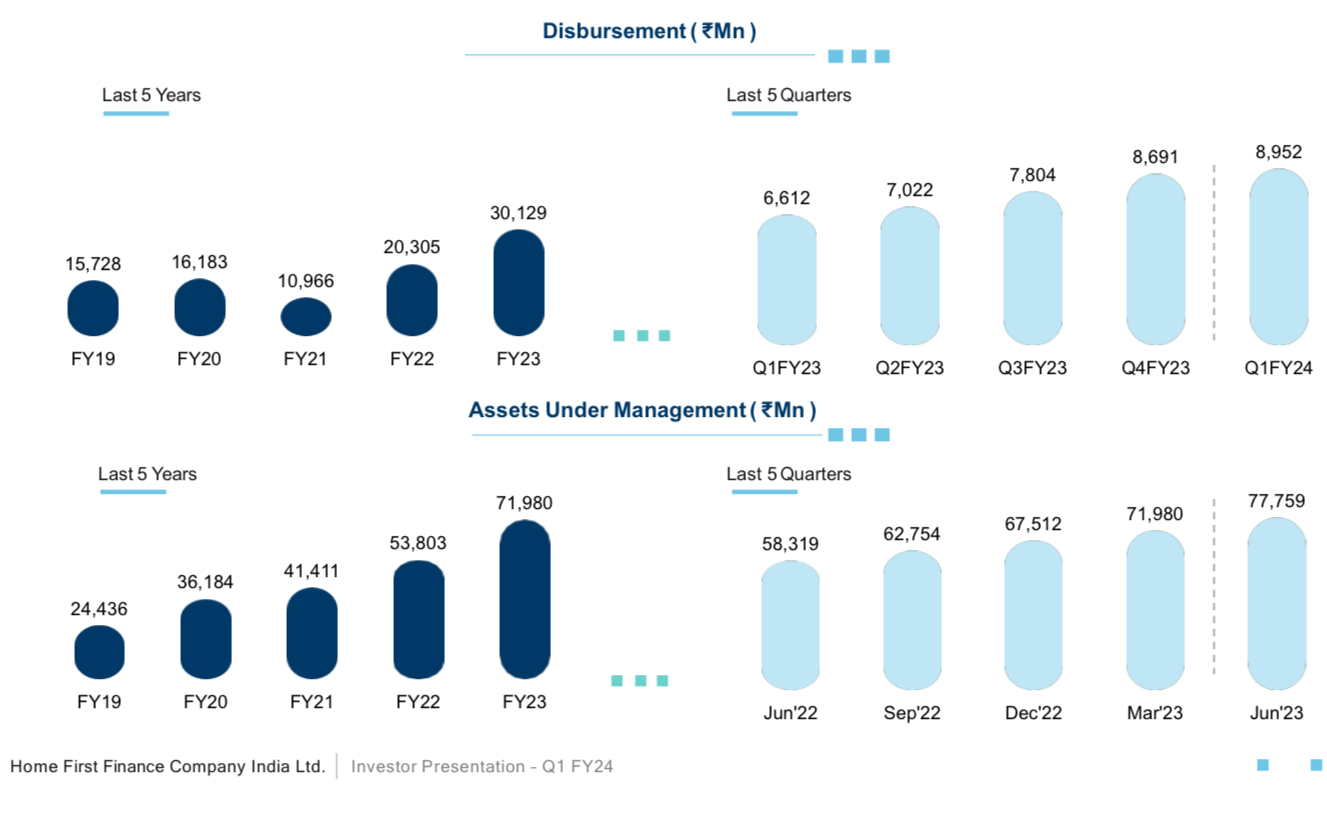

Q1 FY 24 Highlights

AUM - 7775.9 cr ( 8% up QoQ and 33% up YoY)

Fresh Disbursements - 895.2 cr (3% up QoQ, 35% up YoY)

Cost to Income - 36%

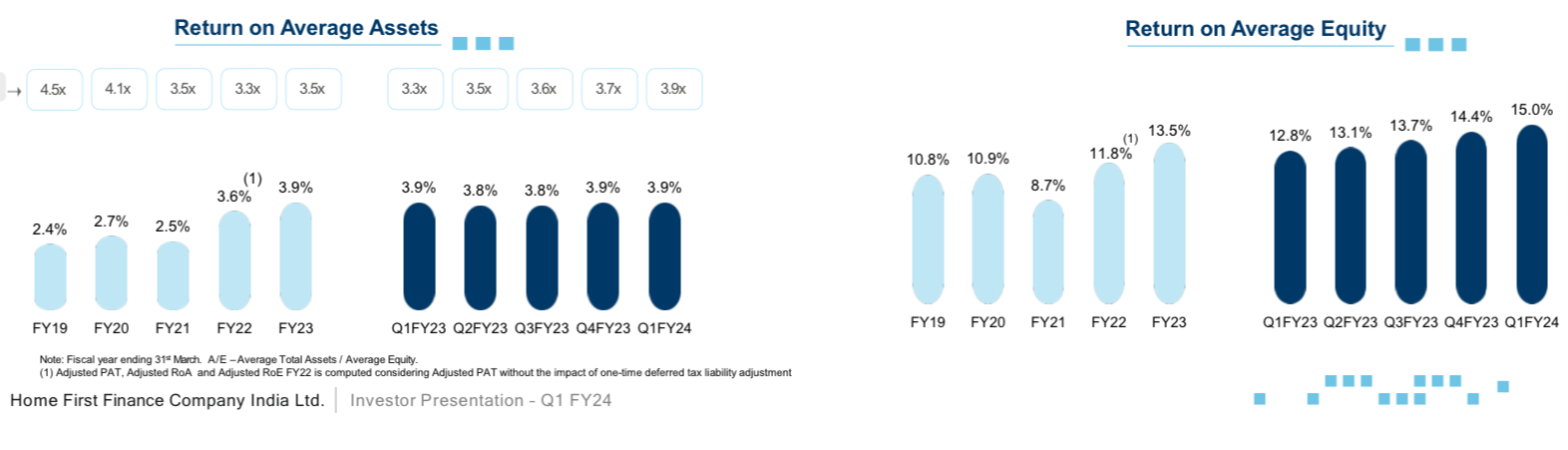

RoA - 3.9%

PAT - 69 cr

Price to Book

What would be right p/b to consider ??

Home first clicking almost all parameters …

Will growth and NIm sustainable when book size enlarge ??.

My personal range of PB for HFFC is 3-3.5. And if you are willing to buy it, you have to hope that P/B expansion will happen. Otherwise stock price will not return anything beyond 15-16% per year

1 Like

Hi All

Can anybody check Gross Profit on Trading View Chart for HomeFirst; it is showing Rs 150.4M , could you explain where they got this number from.

Note: I checked the earnings ppt

One should be careful in assigning PB to HFC. Earlier in the past they used to trade at crazy P/B and growth was not supporting PB. Pls note that HFC have limited segments to lend Housing + Affordable housing. NIMs are in Aff hsg and this segment is today getting highly competitive with pvt/ psu Banks, NBFC, SFB focussing on this segment. Hence, I think PB to HFC should not be more than 2 if you want to invest for good near term returns. In high Interest regime, NIM’s are under pressure and earnings growth have not been great in june quarter as well for HFC’s.

1 Like

Aavas had a great run…When its loan book gets big the same HF company not looking optimistic as it looks earlier… But how to get good HFC at 2x of PB??

There is only 1 HDFC Limited which has grown large in HFC sector. It gets tough to grow beyond a level in single segment. In financial sector, diversification is the key. Even likes such as Bajaj, Chola are diversified now. Today, there are better opportunities in market as compared to pure play HFC’s as their product portfolio is limited, no fees income, high competition, lower Yield and only advantage-Lower NPA. IMHO, negatives are more as compared to positive. History speaks, pure CV financiers - Shriram, M&M, pure Gold loan financiers-Muthoot, Mannapuram are unable to grow when Banks/Large NBFC’s focus on their segments. Loan book has to be diversified for any Financial institution to become big.

I hold a different perspective. In my view, a business’s growth should primarily depend on the available market and its growth potential, rather than the degree of diversification it possesses. Specifically, I strongly believe that the affordable housing loan market represents a substantial and continuously expanding opportunity.

The negatives you mentioned about the business not diversifying into other sectors do not concern me. I do not see it as a negative factor. I believe that instances where growth has tapered off in other businesses were primarily due to the limited size of the addressable market, rather than being a consequence of focusing on a single area of expertise.

For me, what truly matters is that a company excels in its core area and remains focused on a large market. I am confident that this approach will yield positive outcomes for investors. As an investor myself, I prefer to have holdings in specialized financial players, each focused on different businesses, as a means to achieve diversification. For instance, one of the players in my portfolio is Ugro Capital focused on another larger addressable market of MSME lending. This way, I aim to spread risk and capture opportunities across various sectors, rather than investing in a single company involved in multiple businesses.

9 Likes

areyou still tracking home first?

& NBFC Review Of Q3FY24 With Digant Haria | N18V | CNBC TV18")

2 Likes

Anybody still tracking Home First?? It’s peer Aavas Financiaries has recently given a breakout after a very long time. I think it would be worthwhile to reveist Home First once again. Would appreciate a comment from some long time followers of Home First.

2 Likes

Union Cabinet Approves Assistance For Construction Of 3 Crore Houses Under PMAY

Read more at: Union Cabinet Approves Assistance For Construction Of Three Crore Houses Under PMAY

Copyright © NDTV Profit

x.com

1 Like

Home First Finance Q1 FY25 Analysis: Key takeaways!!

Home First Finance continues to demonstrate strong growth momentum, with AUM crossing the Rs. 10,000 crore milestone in Q1 FY25. The company reported a 34.8% year-over-year AUM growth to Rs. 10,478 crore, driven by broad-based expansion across markets. Disbursements reached a new high of Rs. 1,163 crore, growing 29.9% year-over-year. The management remains confident in sustaining 30%+ growth rates in the near term, supported by strong demand and expansion opportunities.

Strategic Initiatives:

-

Technology-driven operations: Home First is leveraging technology to improve efficiency and customer experience. Account aggregator adoption has reached 41% for new approvals, while 95% of customers are registered on the company’s app.

-

Geographical expansion: The company is focusing on deeper penetration in existing markets and expanding into new states like UP, MP, and Rajasthan.

-

Product mix optimization: Home First is gradually increasing its Loan Against Property (LAP) portfolio to enhance yields, while maintaining a primary focus on housing loans.

-

Co-lending partnerships: The company aims to scale up co-lending to 10% of disbursements in the near term to improve capital efficiency.

Trends and Themes:

-

Increasing ticket sizes: Average ticket sizes are gradually moving up due to income growth and inflation in property prices.

-

Digitalization: Home First is seeing high adoption of digital processes, with 70%+ digital fulfillment and 90% of service requests raised through the mobile app.

-

Granular distribution: The company maintains a focus on small, individual connectors rather than large DSAs for loan sourcing.

Industry Tailwinds:

- Strong demand for affordable housing

- Government support for the housing sector

- Increasing formalization of the economy, benefiting organized lenders

Industry Headwinds:

- Rising interest rate environment

- Increasing competition in the affordable housing finance space

- Potential asset quality concerns in an inflationary environment

Analyst Concerns and Management Response:

-

Margin pressure: Analysts expressed concern about yield softening and cost of funds increasing. Management responded by announcing a 35 bps PLR hike effective August 1, 2024, to help maintain spreads.

-

Capital adequacy: With a high capital adequacy ratio of 36.2%, analysts questioned the need for off-book strategies. Management clarified that they are building these capabilities gradually and will scale up when needed.

-

Asset quality in new geographies: Management emphasized their risk assessment processes and centralized underwriting to maintain asset quality as they expand into new markets.

Competitive Landscape:

The affordable housing finance sector is becoming increasingly competitive, with larger players entering the small-ticket segment. Home First differentiates itself through its technology-driven approach, granular distribution model, and focus on customer experience.

Guidance and Outlook:

- AUM growth target of 30%+ for FY25

- ROE improvement of 50-75 bps annually, targeting 16.2-16.5% for FY25

- Spread (excluding co-lending) expected to remain around 5.2% in the near term

Capital Allocation Strategy:

Home First maintains a strong capital position with a total CRAR of 36.2%. The company plans to optimize capital utilization through co-lending and securitization while maintaining an internal CRAR threshold of 20%. Management indicated potential capital raising in the next 6-8 quarters.

Opportunities & Risks:

Opportunities:

- Expansion into new geographies

- Increasing LAP portfolio share

- Scaling up co-lending partnerships

Risks:

- Intense competition leading to margin pressure

- Potential asset quality deterioration in new markets

- Regulatory changes impacting the affordable housing finance sector

Regulatory Environment:

The company operates in a highly regulated environment, adhering to RBI and NHB guidelines. Recent regulatory changes, such as the April 2024 circular on disbursements, have had minimal impact on Home First due to its digital-first approach.

Customer Sentiment:

Management noted strong demand for affordable housing loans across markets. However, they observed some changes in customer behavior post-COVID, such as increased usage of UPI and multiple bank accounts, affecting EMI payment patterns.

Top 3 Takeaways:

- Robust growth trajectory with AUM crossing Rs. 10,000 crore and 34.8% year-over-year growth

- Technology-driven operations enabling efficient scaling and improved customer experience

- Focus on maintaining spreads through PLR hike and optimizing product mix with gradual increase in LAP portfolio

4 Likes

3 Likes