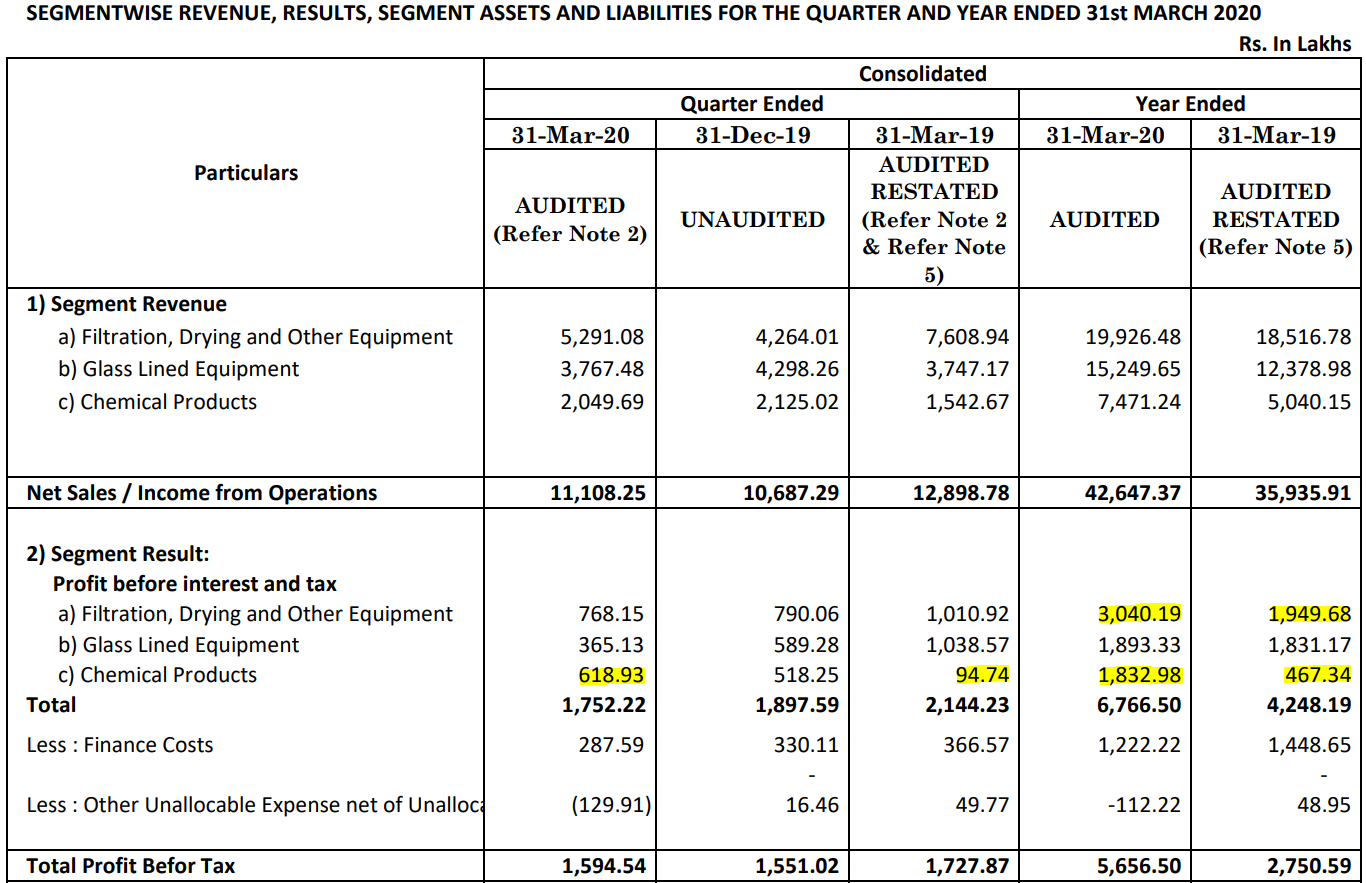

GLE is stagnant to be fair, and Chem had extraordinarily great performance, Filter/Drying eqpt. (FDE) performed well. I guess they are refurbishing/re-engineering and expanding, specifically the GLE production, which explains divergence from continued market demand. (also margins may be muted due to heavy dependence on input prices)

They have a great product in the FDE, add to it the GLE and that makes a great combo.

Good to have the Chem icing on top, hope they move it and not shut it down.

Folks,

I’ve only just come across these two companies - what is driving such expensive valuations for these two? HLE has gone up 5-fold in the past 6 months ! Duopolies are nice, a great deal of predictability in the market share and competition skyline. Growth in the standalone results of HLE is impressive. I’ll dig some more into this and post.

Disc: Not invested.

Two points, the contingent liabilities and increase in share capital:

Assuming that the capex they have raised is being counted under net debt, there seems to have happened a dilution of shares over the last financial year.

Can someone here explain, whats happening with the stock price, it seems to be running on a rocket engine.

Is it trying to catch up with the valuation of GMM Pfaulder or is it just a rally on hope. Or is there something in the background that the broad market is missing.

I’m looking at this rally for a few days and it gives me a similar impression of what happened in HEG previously. Where the stock price jumped 20 times in a short period and came down back to where it all started.

The question is its still a good time to enter for some quick returns , risky scenario indeed.

what cud be the possible EPS tgt for fy 22 n 23? Views Invited

DISCL- INVESTED

HLE GLASCOAT TRADING BEGINS AT NSE.FROM 22 FEB 2021.One more round of rerating to begin like happened for other stocks which were earlier listed at BSE only.

Post GMM Pfaudler’s acquisition of the parent, the consolidated revenue for FY22 is expected to be around INR 2000 Cr (acc. to mgmt). Assuming a PAT margin of 9-10% (conservative as compared to it’s historic PAT margin of 12-13%), the bottom line would be INR 180-200 Cr, which values GMM Pfaudler at 32-35 PE FY 22 (at CMP). HLE Glascoat currently trades at about 70 PE (TTM). In this case, can we see some moderation in PE multiple for HLE Glascoat going ahead or will GMM Pfaudler stock rally to catch up the valuation gap making it a better investment at current levels?

GMM mgmt. expects a top line of INR 2800 Cr FY24 (consolidated basis) which translates to a high single digit - low teen kind of a top line growth. The above figure acc to mgmt. is conservative and if anything it’ll only increase. This also means GMM trades at a Price to Sales (FY24) of ~2.5x currently. Assuming HLE top line grows at 30% y-o-y it is currently trading at Price to Sales (FY24) of ~4x. There definitely might be a case of better margins for HLE.

Wanted to know others’ views whether this makes GMM a better investment as compared to HLE or is it just that the market is still sceptical as to whether GMM can deliver globally and would want to look at a couple of quarter results before the valuation gap narrows?

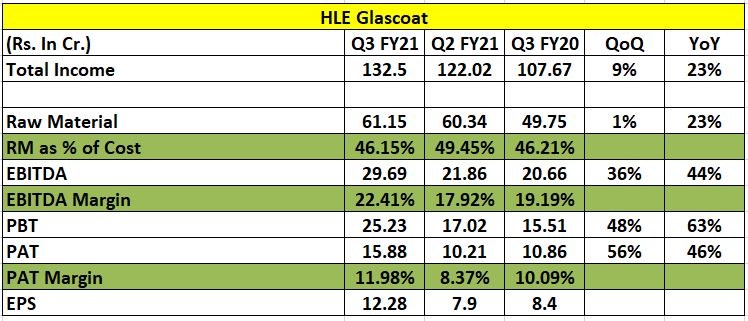

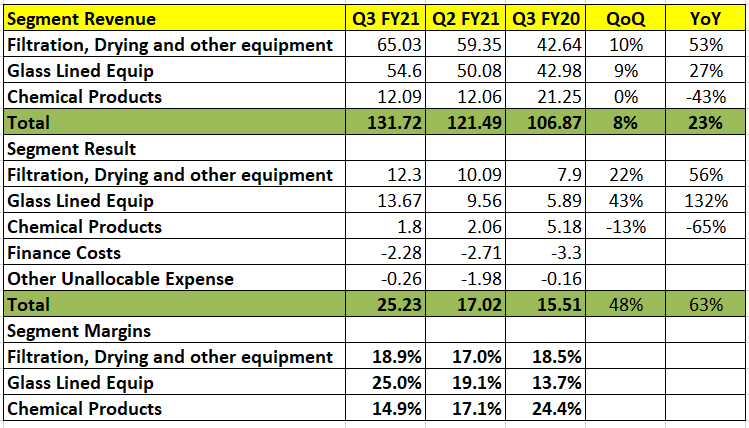

Very good numbers, ROCE has gone over 50% now, the story does remain intact, huge market share gains in both HLE & F&D, they have done really well.

And speaking about Pfaudler Inc, it is surprising to know that Pfaudler Inc has not grown revenues since the last 3 years. I dont know if this was disclosed by the GMM Management but many investors (even me) were thinking Pfaudler Inc was growing at low teens.

Order book of 6 months for filter, dryers and glass lines equipment.

Net debt at 56 Cr, reduced from 74 Cr in FY20.

ROE and ROCE at 39% and 41% respectively

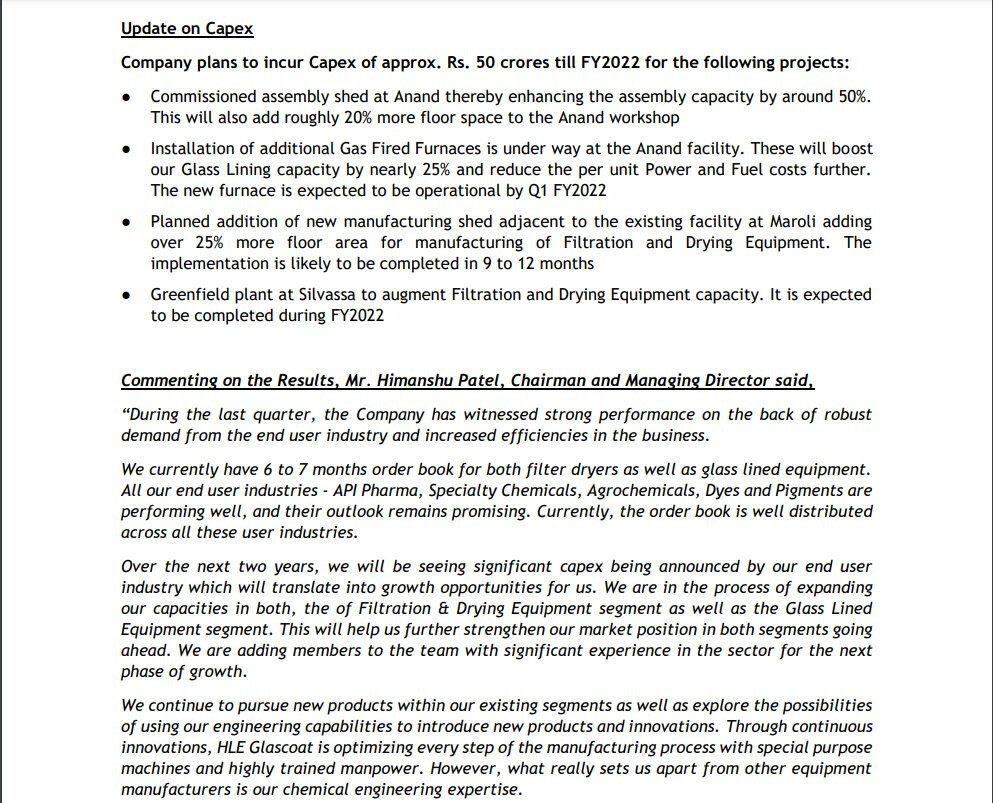

Capex:

Installation of additional gas fired furnace at the Anand facility and to be operational by Q1FY22. This will increases GL capacity by 25% and reduce power and fuel cost.

Addition of 25% more flooring area for manufacturing of filtration ,drying and other equipment at Maroli. This is likely to be completed in 9 months at cost of Rs. 15 Crs.

3.Greenfiled plant at Silvasaa for filtration ,drying and other equipment at cost of Rs.50 cr to be completed during FY22.

Company has limitations in operations due to lockdowns, unavailability of oxygen, manpower shortages…etc due to second wave of covid 19.

Aalap Patel ED at HLE

I am thrilled to announce that HLE Glascoat Limited is among the twenty-six companies from India that have made it to Forbes Asia’s Best Under A Billion, an annual list of 200 publicly listed small and midsized companies in the Asia-Pacific region with sales under $1 billion. In a challenging year, a clutch of companies stood out for their resilience, clocking in sound financial figures amidst the pandemic.

:We are proud to have done our part in making an “Atmanirbhar Bharat” by developing and manufacturing highly differentiated chemical processing equipment that have replaced foreign equipment. We have been at it for the last 4 decades and our products are used and trusted by all the top pharmaceutical and chemical companies in India.

Amit Kalra Chief transformation officer HLE Glascoat

I am thrilled to announce that, HLE Glascoat (www.hleglascoat.com) has signed a definitive agreement to acquire the global business of Thaletec GmbH, Germany, (www.thaletec.com) the leaders in glass lined process equipment in the highly sophisticated German market. This acquisition will enable us to expand our global footprint and further enhance our product differentiation. Our vision is to create excellent benefits for our customers globally by combining Indian industriousness with German innovation. We look forward to welcome our new enthusiastic German Team to our HLE Glascoat Limited family.