Dear All,

I found this company to be interesting, please provide your inputs. About Company

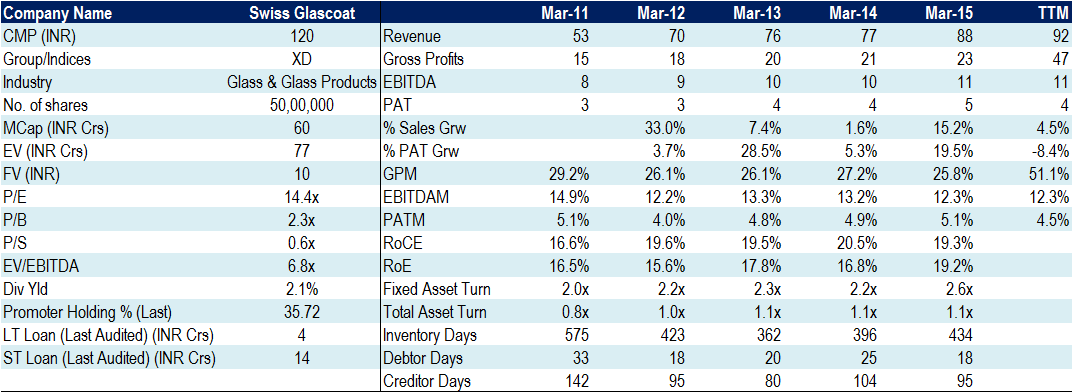

Swiss Glascoat Equipments specializes in design and manufacturing of Carbon Steel Glass Lined Equipment (Reactors, Receivers / Storage Tanks, Dryers, Filters, Columns, Agitators, Valves, Pipes & Fittings) Prodcuts are sold to Pharmaceutical / API, Specialty Chemicals, Dyes/ Colours, Agro Chemicals, Food Processing and allied Industries. Nature of Indian Industry

Largest player is GMM Pfaudler. I guess Swiss Glascoat is the second largest player. Investment Trigger:

With renewed interest in Chemicals industry, I feel many players will augment their capacity in the near term. I guess there will be fair amount of capex in India. (Not verified yet). Negatives:

Promoter Holding is low

Some how its Gross Margins are significantly lesser than GMM

Inventory overhang (as of FY15 out of INR 50 cr inventory and INR 34 cr of wip). Would appreciate if anyone can throw some light about industrial sector inventory dynamics) Snapshot:

There are only 2 listed companies in India in glass lined manufacturing space as of now - 1. GMM Pfaudler and 2. Swiss Glascoat. Both companies are plagued with issue of no meaningful growth.

GMM Pfaudler’s foreign promoter gave open offer to minority shareholders in April 2015 but failed.

In case of Swiss Glascoat, I don’t understand why the company carries inventory worth half the sales on its Balance Sheet. This leads to high short term borrowing (high interest cost) thereby impacting profitability .

Reviving a relatively inactive thread…Since this thread started with a valuation comparison with GMM Pfaudler, pasting a link of a recent blog post I came across on GMM Pfaudler -

Interesting write up on GMM although present valuations look quite expensive.

Longer replacement cycle can really affect the growth and this can be a laggard for some time, as valuations are rich already.

But definitely a stock that has to be kept on radar on bad days / bad results.

Yes agree with you looking interesting and company entering in to Non Glass Lined Equipment

And cross selling to old customer may lead to growth

Disclosure not invested in GMM pfaudler

Thanks

hello all,

1 interesting aspect is that banco products india limited and it’s promoters overseas pearl limited and hasumati patel hold around 11% of the total shareholding of swiss glascoat as part of the public share holding. Wondering if there is some relationship between swiss glascoat promoters and banco products india limited promoters. since the new promoters have recently taken over, this is pretty curious.

disclosure: not invested, but actively looking as a turnaround case.

I had attended the AGM of Swiss Glascoat. Some of the points I noted during the AGM are given below:

• NCLT approval for the merger is expected to be received by October, 2019. Board will take a call on dividend post the merger.

• We are working to reduce inventory days in Swiss Glascoat.

• Order book – Both HLE and Swiss Glascoat have inventory of more than 6 – 7 months.

• Post-acquisition of Swiss Glascoat by HLE Engineers, we have added quite a few new customers.

• HLE is a market leader in Agitated Nutsche Filter Dryer (ANFD) with 50% plus market share. Like Glass Line Equipment (GLE), ANFD also have oligopoly market structure with top 3 players controlling 80% of the market. Our largest competitor in ANFD is GMM. We have been in these segment for decades and have built expertise in it over the years.

• HLE started as a chemical company and later forayed into ANFD. Post restructuring in the group, a portion of chemical business remained in HLE as the ANFD division shared the same premise as that portion of chemical division. We might plan to shut these chemical division going forward. Chemical division contributes Rs.40 – 50 crore to sales of HLE.

• HLE uses stainless steel while Swiss Glascoat used Carbon Steel. Post-merger, there will be synergies in procurement and increased bargaining power with steel manufacturers.

• We completed expansion in Swiss Glascoat by almost 40% in February, 2019. The benefit of that will accrue in the current year. Furthermore, we might look for further expansion by year end. Total cost of capex was Rs.15 crore funded through debt and internal accruals.

• HLE had low margins in FY17 as it was one off year where we had to shut down capacities for undergoing modernization and capacity expansion.

• Market size for GLE business is Rs.500 crore while for ANFD business is Rs.500 crore. Both the segments are seeing increase in demand due to large capex being undertaken by chemical and pharmaceutical industry (largely API).

• GMM’s EBITDA margins are higher than Swiss Glascoat on account of some pricing advantage which they have due to their MNC parentage, conversion to gas based furnace and export sales which have much higher margins than domestic markets. There are lot of low hanging fruits in Swiss Glascoat to improve margins. For the expansion, we have used gas based furnace instead of electric furnace installed in existing plant. Furthermore, Swiss Glascoat currently derives negligible revenue from exports. We have started focussing on exports by participating in chemical fairs. We want to focus on export markets as well now. HLE already derives 5 – 10% of revenue from overseas markets.

• Post takeover by new management, in Swiss Glascoat we have done three major changes:

o Capex for expansion in capacities which got completed in February, 2019

o Substantial debottlenecking done in the plant

o Changed lay out of the plant for better operations

• Lot of synergies in marketing in HLE and Swiss Glascoat. There are hardly any orders where we are not discussing ANFD and GLE products in the same breadth. HLE does its marketing through its own offices while Swiss Glascoat works through its own channel partners.

• HLE is also seeing major shift happening from centrifugal filter and dryer market as ANFD is the latest and advanced technology. However, ANFD prices are more than centrifugal ones. Large chemical players already use ANFD while smaller companies in the sector use centrifugal filters and dryers.

• Replacement cycle for HLE is 10 years plus while for GLE it varies from 3 to 10 years depending on usage. On an average the lifecycle of GLE is 8 – 9 years. However, in more corrosive environment the lifecycle of GLE is less.

• Growth in Swiss Glascoat will be more than HLE as there is lot of room for improvement in market share in it.

• Exports are a thrust area for us in Swiss Glascoat. We have participated in trade shows in Germany and received some export orders as well. Export sales will grow sharply as we currently hardly have any sales from it. Europe, South East Asia and US will be our major markets for exports.

• In terms of quality in GLE, we are at par with our competitors. If companies like Divis, Bayer and other large chemical/pharmaceutical API companies are our customers speaks a lot about our quality. Name any large player in the segment and we would have supplied products to them.

• Advances from customers range from 10 – 30% depending on client and quantum of order to be supplied – for both HLE and Swiss Glascoat.

• With current capacity, Swiss Glascoat can do turnover of Rs.180 – 200 crore while HLE’s equipment division can do revenue of Rs.250 – 300 crore.

• HLE holds 80% stake in HL Equipment which has a plant in Silvassa. It also manufactures ANFD.

• ANFDs are highly customized and complex products. Requirement of each and every customer is different. We have also launched off the shelf model in FY19 targeting smaller chemical companies where there is no customization and price is lower. The machine received good success.

• Operating leverage can come in both the companies – HLE and Swiss Glasscoat with increase in revenue.

• Inventory is on higher side in Swiss Glascoat compared to GMM? Taking measures to improve inventory days. Increased vendor base to two from earlier one. We require specialized carbon steel. Inventory day rationalisation will take time but will eventually happen.

• We supply reactors as well as tanks. We are also present in high KL reactors and provide the entire range to customers.

• Target growth of 15 – 20% in revenue over the next 2 – 3 years in both the companies combined.

With regards to the parent, the shift from centrifuge to ANFD is certainly true …multiple centrifuges have to employed to clear out single GLR reaction batch, whereas with the use of ANFD the entire batch can be processed in one go in ANFD of a respectable size.Even smaller chemical companies are shifting to ANFD, centrifuges also require regular maintenance with the bearings giving out every now and then, which is not the case with a hydraulic or a gear ANFD.

So in addition to GLR there should be sustained demand from ANFD side as well

Thanks for the info. whats the opp size of ANFD & GLE ? are u in some way associated with the chemical sector ?Any idea about the promoter quality of new promoters of Swiss glasscoat ie the promoters of HLE mr Himanshu patel n mr aalap patel? views invited from other VPers too?

I run an agrochemical plant, have recently replaced some of our centrifuges with used ANF, thus the knowledge, i am not sure of HLE personally but they have a good name in the market at least for the ANFD.

with regards the opportunity, i won’t be able to put an number on it, but GLR, ANF, dryer is the basic infrastructure required for any chemical or pharma plant, so with all this new capacity going up with the shift from industry from china to india should create some sustained demand.

HLE, one of the largest manufacturers of filtration and drying equipment across the globe with a CAGR of 25%, established in the year 1981. Initially the company was formed to cater their own engineering needs of the fast growing “Patel Group” chemical companies. After 1995, with a rich experience in the chemical industry they started supplying Filters & Dryers to customers across India & few years later across

Mr. Himanshu Patel, Managing Director & Owner of HLE says, “We specialize in exotic metal equipments and since we have experience of making apparatus for our own use, we have deep rooted knowledge of making various equipments used in process vessel industries. In India during early 90s, there was a huge need of filters & dryers and HLE was the only company started making related equipments on their own when every other company were doing it by collaborating with some foreign parties. Also before offering it to customers, we established a pilot plant for testing, research & developments.

Q3FY20 Results. Thesis playing out with margins improving in this quarter and cost of material consumed as a percentage of sales has also reduced. Indicating syngeries arising, and moreover they have also declared a dividend. Stock still seems cheap going by the numbers that will reflect in FY21.