I usually average up in my positions where I find that there is clear visibility of growth for near to medium term. Or else some other near to medium term trigger is clearly visible. Sometimes I take my cues from technicals, where if I find that after very tight consolidation, stock price has broken up to the upside with good volumes.

In current market environment nearly every stock has corrected to varying extent . If I find that stocks which are not likely to be affected by current market concerns also have corrected and offer attractive entry opportunities, then also I add more even though stock price may be much higher than my initial buy price.

Regarding profit booking I am not too good at this aspect and its always a work in progress for me. One parameter I use these days is to look out for trend change in price. If there are signs of breakdown in stock price, then I exit or atleast book partial profits. In instances where there has been parabolic rise (instances where stock price goes up 50-100% or more in a matter of days or weeks) in stock price without too much change in fundamentals, I often book partial or full profits.

Would really appreciate your view about the ongoing wave of tech IPOs in India. At first glance, value investors like ourselves would tend to avoid such overpriced issues and wait for the dust to settle before picking which horses to back. On the other hand, we’ve seen how the US and Chinese markets have come to be dominated by tech stocks over the last 10-20 years. If we believe a similar pattern will play out in India as well, we need to pay attention to good internet businesses and buy them at the right time, even if we need to overpay a bit in the short term. Where do you see the opportunity in this space and how are you thinking about it?

Thank you

D - not invested in but tracking all the recent tech IPOs

I think you have a very pertinent point. Tech and platform companies would be the place to watch going forward. As investors we need to learn how to evaluate these kind of businesses. Idea should be to find out companies which are going to emerge winners and those that have staying power. Most of these companies initially are cash burn type of companies and still markets are willing to pay top dollars for these companies.

From among all listed companies, its a tall ask to find out companies of above characteristics which are going to emerge winners. So it might make sense to keep a basket of such stocks and as and when picture becomes clearer, add to winners.

what is your take on PSUs at the moment. Many are trading at a price to sales of less than 1 and has P/E of 5, which is way below average multiple of past years. The investments and cash equivalent are more than twice the market cap. I am referring to GAIL and OIL India as example

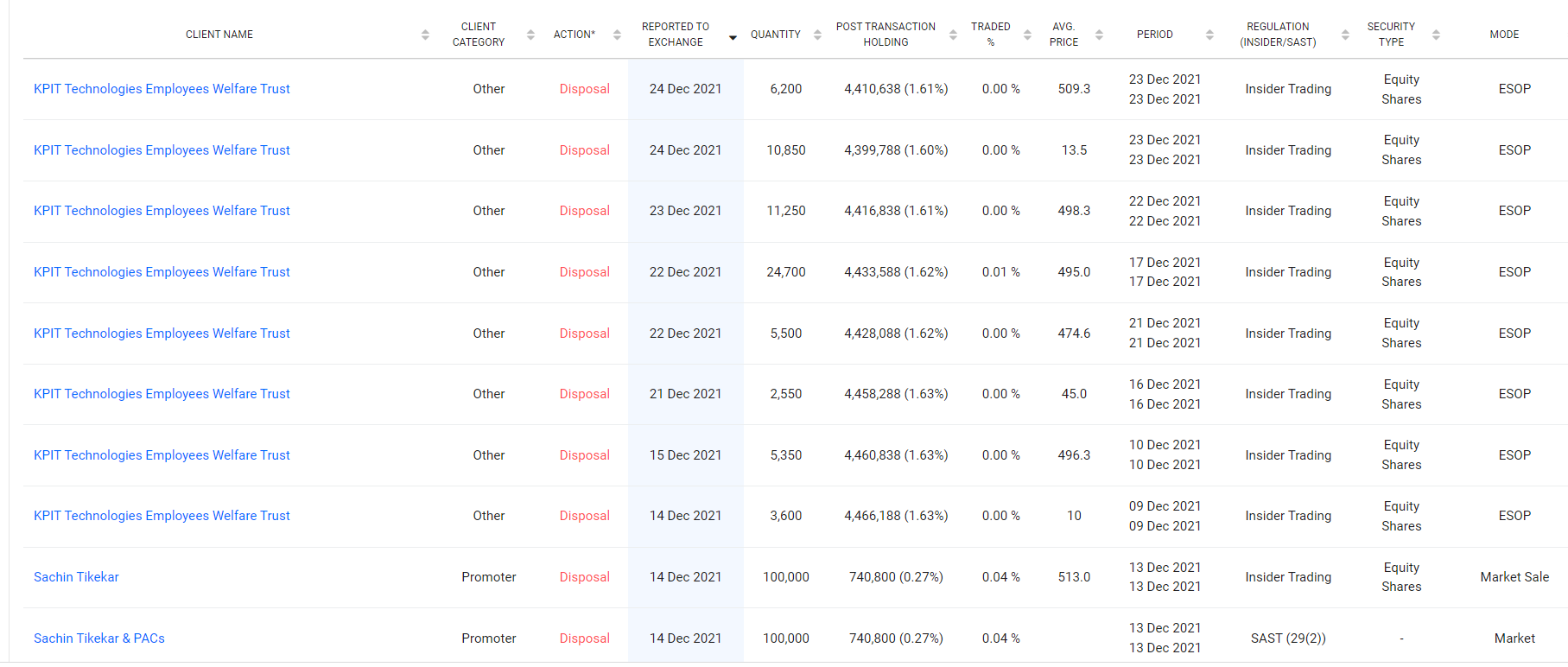

I think the quantum of sales of shares by promoters and PAC in KPIT tech is not too significant in view of overall holding. And the other way to look at it is that inspite of promoters selling, stock price continues to go strong even in a weak market.

We had similar situation where Page Inds promoters were selling shares in open market and stock price continued to hold good and even kept going up inspite of promoters selling their shares at different price points.

I think if we follow fundamentals, the main parameter to look out for is growth and balance sheet strength, followed by minor things like promoters selling shares in minor quantities. If they come out and sell big chunks of their holdings, then I would want to warrant caution and re assess my position.

@Sridhara_R I do not follow ineos styrolution. But as far as I know it is a commodity chemical company and these should be considered as opportunistic plays to ride strong business tailwinds. Difficult to visualise chemicals in current market as value plays. Most of them have gone up multifold and I would like to know on which parameters they qualify as value plays. If we consider TTM earnings we have to be careful to consider the lumpiness in earnings because of shortages and price rises of products of these companies. One has to be absolutely sure that higher prices seen in the past are going to sustain.

@ram1984 Most of the PSUs have been value traps over the years. One look at the price charts of these entities is enough to validate this theory. I dont know how you arrived at the formula of investment and cash higher than market cap in GAIL. I haven’t looked at OIL figures. However off and on these stocks do display strong rallies after periods of prolonged neglect by markets. However timing these rallies is often difficult and one has to be adept at catching the change in trend from down/sideways to up. And then be smart enough to exit at right place as most of the times these stocks give up their gains quickly. Many of these companies are monopolistic companies and I had high hopes from these companies after BJP came to power in 2014, but in last 7 years not much seems to have changed. Even the disinvestment story seems to be losing its steam with ministers making noises off and on about the subject and no real articulation from the govt on how and where they stand with respect to the divestment of these companies. There are different mouth pieces making different sounds and we as investors don’t know who to trust.

Your view on KPR mills at current valuation. You have mentioned this stock long ago in your thread before pandemic and thats when I added and holding since from very lower level. Would love to hear from you if you still track this stock?

KPR Mills had promised improved margins with higher revenues coming from garments few quarters back. That now seems to be playing out and stock price has been on a strong upmove. Results for Sep quarter have been also very good.

Overall it looks a good combination of excellent fundamentals with a strong chart.

What are your views on the spechem pack, Hitesh sir? Most of the strong companies have recovered and have earnings triggers ahead of them. Eg:- Navin, Deepak, GFL etc.

Hitesh Sir ,

How do you see the opportunity of recent multi year breakout in Mayur Uniquoter ? PU leather production as next growth engine , as mayur could be sole exporter of PU leather from India and the tailwinds in terms of shift from animal leather to PU leather.

Thanks.

I feel the speciality chemicals rally is a multiyear event. It will of course be interrupted by corrections and that’s a healthy sign. Most of the characteristics of sectoral stocks in a rally with longer term growth visibility are present in spec chem pack. One can compare these to previous bull run sectoral stocks/sectors. Usually its to do with very high growth visibility. Starting with moderate valuations, these stocks attain superstocks status with valuations reaching high levels and sustaining for multiple quarters/years. This is due to continuous positive newsflow and consistent results shown by these companies. Even when these stocks correct, its usually healthy correction and these stocks often dont break their longer term uptrends.

As you say, most of these stocks have earnings triggers in form of capex, strong product demand, shift in sourcing from other geographies to India etc.

These kind of rallies can sustain for a long time and surprise a lot of investors for a long time.

Few days back, Mayur gave a strong breakout above its previous all time high of 560 and went up to 626 before cooling off along with broader markets. Its now trying to take support from the zone of previous highs. (usually we should consider a zone of support instead of a fixed number. In this case a few rupees above and below 560).

Fundamentally too a lot of triggers are lined up for Mayur going ahead. Near term headwinds are there in form of lackslutre auto sales numbers. But if its exports pick up and PU plant starts contributing meaningfully, it can give good returns.

Technically any stock that has crossed its major resistance (here its previous ATH) and then subsequently consolidating around that level on declines, is a stock worth considering.

Firstly a big thanks for taking your time out and guiding novice investors like us. I follow your replies relgiously and it has been a great learning experience.

Sir if you follow Finolex industries and airo lam please share your views. Lot of news from all quarters coming about pickup in real estate sector and these 2

companies are available at relatively cheap valuations as compared to their peers .

If you do not advise them then anything intresting in this sector which you like

I have been looking into Mayur Uniquoters for quite some time and i have a few questions, which concern me before putting fresh money into Mayur - kindly advise.

They are very poor at collection and their debtor days are at their highest as per Mar 21 reports (113days)

They are also very poor at inventory management - current aging - 165days

Their operating cashflow is consistently lower for Mar 2019, 2020, 2021 than that of Mar 2017 and Mar 2018 - this is also reflected in their annual sales growth (Last 5 years - 0%)

Their operating profit margin is also markedly lower than 2016 and 2017 nos. likewise their ROCE is at 18% down from 36% in FY’16/17

Honestly, from a value investor standpoint, there are few things that are worrisome with Mayur especially since Auto Industry not showing definite signs of revival beyond Tata motors. Do you think that the current uptick in Mayur could be speculative or operator play? or there is a possibility of secular growth story unfolding? They have in last few years, invested heavily in adding capacity - but seemingly the demand hasn’t kept pace with capacity addition

How do you view Mayur from value investing standpoint? Or you look at it merely from technical perspective?

Hi Hitesh sir

Seeing the positive headwinds in textile stock

Export of yarn cotton showing improvement more than garments

Seeing the fundamentals which are the good stocks in the segment to read according to you

I had a look at finolex inds and it seems interesting. It is the only pipes manufacturer which is vertically integrated right from PVC production. In past couple of quarters the play was on rising PVC prices, because of which the company benefited and reported good numbers. Going ahead, demand pickup from agri and real estate space should augur well for the company. You can listen in to concall of the company to get a better idea about the company. Valuationwise also its not too expensive, but we have to consider the fact that part of the business is PVC which is a commodity business. Pipes business is a very good business with a lot of demand tailwinds currently.

Mayur recently broke out above its previous all time high of 561 posted in 2018, posting a fresh all time high above 600 this time. In tune with markets it corrected and is now retesting its breakout levels. (560 plus or minus few rupees. ) Usually when stocks take out their all time highs, its time to sit up and take notice. Here in absence of any obvious results, stock price has gone up and hit all time high. So ideal thing would be to listen to the most recent concall and try to figure out if there are any triggers. I think the PU plant commissioning and export demand are two important triggers for the company. Auto demand has witnessed a slight slump but going ahead, I think this too should revive.

I do not track figures for Mayur too closely but most of the times, numbers alone is only a part of the story. One needs to dig deeper and figure out what is going on.