If one were to go for SEP or SIP, in a bunch of stocks, then there should be atleast some diversification to minimise company specific risk. In case of Asian Paints, the one big risk I see is the entry of two big entities into the paints segments… namely Grasim and JSW. Both are groups with deep pockets and have a long standing presence in the Indian business environment. If Asian paints starts feeling the heat from these companies and suffers market share loss, then there could be some strong de rating in the company. As of now things seem going well for Asian Paints, but we need to watch out for how things pan out in terms of competition.

So for someone wanting to play conservative game for the real long term, a basket of high quality businesses bought in a regular manner over a long period of time would be very fruitful and my guess is it would beat index funds too.

Sir,hope you are doing well.

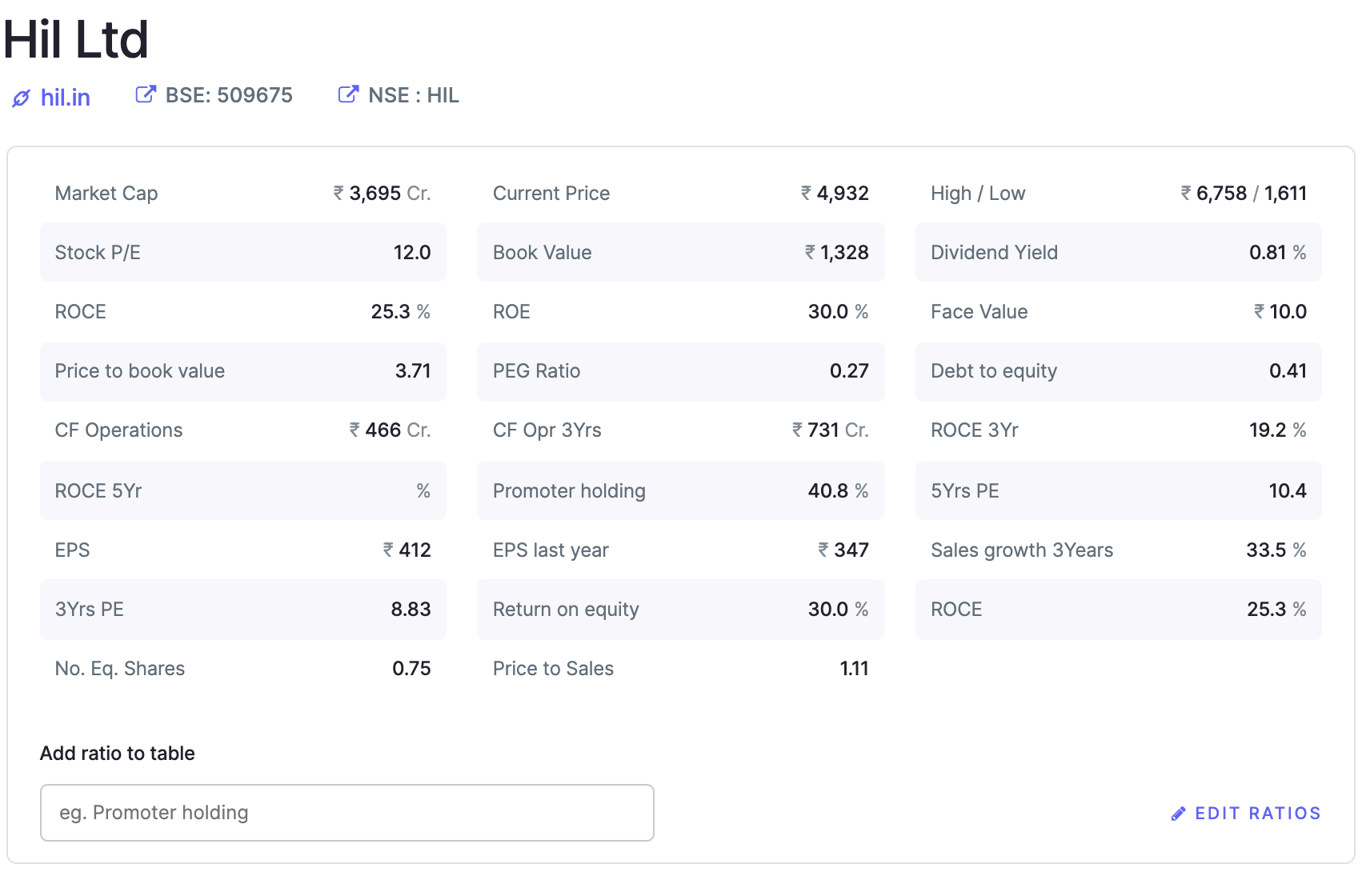

Wanted to know your views on HIL.

As a building material theme I like their good product line - pipes, roofs, wall putty, bricks,wooden flooring etc.Impressive product diversification.

Nice fundamentals- toppline,profits,ROE,ROCE

Available at 12 PE and 0.3 PEG

CK birla group company so CG wise good

Moving away from asbestos roof to non-asbestos. Earlier asbestos share was 50-60%, now it is 30% and they want to move to non asbestos fully.

CEO mentions 1 Bn USD sales by 2025, that makes a sales CAGR of around 20%.

Concern: only concern I have is that CEO offloaded his major chunk of ESOPs worth approx Rs 10 crores in august at peak price of 6500 odd. Not sure how to take that. But my sense says that if he is so hung ho about 20% business growth then he could have used other channels if at all he wanted money for some purpose.

Do you have views on HDFC AMC? They have been struggling for growth since past one and a half years. They lost their market leader position in AUM and are at third level now (below SBI and ICICI) and the gap is widening. SBI MF is galloping ahead crossing 6L crore AUM whereas HDFC is at 4.4L crores.

SBI’s growth is not just based on the ETF inflow they get from Provident fund trusts but they are growing their non ETF equity AUM as well and are improving their profitability. HDFC used to advertise that they are the most profitable asset manager but ICICI would have overtaken them on that and SBI may do soon as well.

Additionally, the new CEO is getting aggressive on passive funds. They have recently filed around 9 such schemes with SEBI. While that’s a good news, I see two issues

Going big on passive’s will impact overall margins unless until they can grow their active funds AUM too.

To counter margin pressure and to regain market share , they need to grow their passive funds AUM also in a big way. But every AMC is having ETF products including the new entrants like Navi and NJInvest and the future ones also will do the same. So, what could be HDFC’s moat in the passive products.

I see so many challenges like this ahead for them with respect to growth and market share (though it’s a very profitable business).

Can you share your views on the same, can they hold on to current valuations?

What is a good strategy in the current times? The markets are rising higher and new sectors are getting added to the rallies . Is it wise to increase cash holdings or continue being fully invested.

I see people recommending unheard of names and those names rallying.

I think the fact that we are in a strong bull market is a foregone conclusion. Now everyone wants to try and predict a top and hope for a correction. But it seems market has a mind of its own. Those trying to time the market till now have not had much success. And that’s usually the case with bull market. It does not care for valuations, percentage gains, duration of rally so on and so forth. In such cases idea should be to try to ride it as well as possible. Its like a huge object in motion. Unless it encounters any strong resistance it is less likely to stop. It might pause here and there but overall trajectory remains undisturbed.

For guys like me, and a lot of other guys who take some cues partly from technicals, there are so many bullish patterns forming and then playing out that the case for being fully invested, albeit changing horses from time to time is a very convincing case. So the idea is to keep riding till any signs of exhaustion become evident. Few weeks back that was the case wherein only large caps were moving and small and midcaps had stopped showing any momentum. But after a brief respite, the rally began in real earnest and continues to go strong. The only difference I see from earlier is that it has become more of a stock picker’s market than before. Not everything is moving these days as it was before a few weeks.

So the idea should be to try to figure out a comfortable investing style and try to improve it and stay invested until and unless negative cues emerge.

The all important question is what kind of negative cues should one look out for. My guess is most important should be to watch out for market breadth, type of price reaction to positive and negative newsflows or data points, etc. And then some unknown pointers will emerge which will manifest themselves at a future point of time and we have to be able to recognise them.

@newone I dont track hdfc amc or any other amc too closely.

Hi Hitesh sir,

For somebody like me who has just started two months back, what should I do? I can invest 10k in a month. Should I wait or continue buying shares at this price?

I am not entering specialty chem as of now. I am planning to keep on investing in Laurus, GPIL, Supreme Industries, Caplin Point, Tata Power for the time being.

Hello Hitesh sir, from your posts I notice that you have Tata Power as a techno funda bet. Do you have any target in mind or how do you plan to play that.

Its tough to decide what to do at these index levels for a newbie. The best thing you can do is first decide what kind of investor you are or want to be. If you are into short to medium term trading, there will be plenty of opportunities in this market with sectoral rotation going on and you have to learn to time your entries and exits (at some point of time).

If you are a long term investor then you should be making a list of high quality companies you may want to hold for next few to many years. Good news here is that there are still some high quality companies which have not gone up ballistic in current market, post the covid rally. These may the ones that need to be looked at.

From the list you put up, GPIL is not something I would consider holding for the really long term. Essentially its a cyclical having a good time, no matter what the narrative at current juncture. So that’s the kind of differentiation you need to have clear in your mind. If you have not got it clear, then do go through the classification explained by Peter Lynch in his book One up on Wall street. (In fact I would advise you to go through it anyway if you plan to invest on your own. )

Another good option is to try to read good threads on VP where great companies are discussed in detail and try to learn how to analyse companies.

Investing without learning the ropes of investing is fraught with risk. More so with markets having rallied so hard.

Tata power as I mentioned in the 52 weeks high thread has crossed its previous all time high above 160. The crucial resistance before that was in the zone of 120-145. Once that was crossed, even 160 did not pose much of a challenge. Today stock price crossed 190.

With these kind of stocks where the entire fall of many years was retraced in a few months, momentum is usually strong and in such cases, its better to keep trailing your stops rather than exiting at predetermined targets. You can see the chart of JSW energy as an example. Somewhat similar chart structure and look at where it went post crossing its previous ATH. So I would prefer to keep riding it till I see signs of weakness in the trend.

@Gothamcapital I do not track the coal crisis in India. It suffices for me that neither is the market bothered by it.

@hitesh2710 Hi sir,

Wanted to know your views on SJVN,NHPC and power grid. I had shortlisted this earlier for pure dividend play with minimum risk.

But now power sector is having significant tailwinds can they also be rerated ?

Besides bull market exuberance, do you see Tata power’s fundamentals justify current valuations? It’s way above life time highs. Same with Bajaj Finance also.

I have not looked at NTPC too closely. Tata Power investment logic I posted in this same thread few posts back. There is a difference between the optionalities for Tata Power and NTPC. Hence Tata Power.

@Shishir_rai I dont track SJVN, NHPC or powergrid.

@newone For Tata Power I think the best is yet to come and hence I do not prefer to look at current valuations to value it. For me it is more a thematic investement. If it does well in most of the segments it is present in, then the picture can be different in a few quarters from now. You may go through the presentation to understand their businesses and divisions.

Your views on Tata Motors. With EV story unfolding, new car model launches, taking market share from maruti and latest TPG investment- Stock is nearing life time high.

Tata Motors has been cyclical - what is your future outlook on the stock.

Tata Motors looks to be a momentum / sentiment run to me, joining the Tesla induced EV bull run. Their domestic passenger vehicle segment has been the bad performer for many years and now that looks to be more promising due to their new electric cars. They still haven’t made any profits for few years already and not sure if just the sentiment towards EV really means if it will be a high growth and profitable business. If Tesla enters Indian market soon with right pricing, it will be difficult for other players to catch up (pricing is key, of course). Valuation of 1.5 Lakh crores for a non profitable company looks quite expensive but stock price may run up as long as market sentiment is good. All Tata group company stock prices have been on a strong rally since last year. Indian Hotels is another example. They are a very solid brand but their business revival will take an year even if there are no further waves. They are still in loss but stock price has crossed life time highs already.

Tata Motors seems to be on a strong footing, with huge pent up demand for cars coming through and success of its models like Harrier, Nexon EV, new lanuches like Tiago EV etc. Even the CV segment seems to be showing some signs of life if one were to go by monthly reported numbers. But I think the rise in the past few days is more a frothy reaction to the TPG investment related to EV. Stock price has gone up from 350-370 to 500 plus within only a couple of weeks. This kind of rise needs some rest and so I think anyone thinking about buying should wait for an opportunistic dip.

Even a look at youtube and social media platforms like Whatsapp is filled with everything and anything about Tata group. This usually signifies a frothy environment. Its not as if all things related to these companies were unknown to markets. Its only now that this bombardment has begun and usually this is designed to induce a sense of adventurism in naive investors. So in my view those wanting to enter fresh should be patient and careful about not getting sucked in at too high prices. Those who had entered earlier may afford to stay invested.

Plus other car companies are also going to go ahead and launch EVs and these probably will be better quality and technology than Tata motors. EV manufacturing no more remains akin to rocket science. Its only a matter of time before EVs become commodity products. And then all this excitement about being in the segment will fade away to more saner levels. This whole process of froth subsiding to sanity could take a few qaurters to few years. Its anybody’s guess.

Those trying to time the market till now have not had much success. And that’s usually the case with bull market. It does not care for valuations, percentage gains, duration of rally so on and so forth. In such cases idea should be to try to ride it as well as possible. Its like a huge object in motion. Unless it encounters any strong resistance it is less likely to stop. It might pause here and there but overall trajectory remains undisturbed.

Those trying to time the market till now have not had much success. And that’s usually the case with bull market. It does not care for valuations, percentage gains, duration of rally so on and so forth. In such cases idea should be to try to ride it as well as possible. Its like a huge object in motion. Unless it encounters any strong resistance it is less likely to stop. It might pause here and there but overall trajectory remains undisturbed.