@hitesh2710 , this is so detailed and very helpful. Really appreciate the fact that you take out so much time to part with your knowledge .

Thank you Sir for such detailed notes. In your personal experience, is it at all possible to spot early next emerging or favoured sector. What should we be looking for.

1 Like

Hitesh sir,

As you explained, NBFC bull market is indeed over. Every NBFC Other than 3-4 guys is de-rated. What do you think about Bajaj Finance right now? Do you still hold it?

As NBFC leader, it’s valuation is still intact and no signs of being de-rated till now. One mind tells me to reduce it looking at overall NBFC/Banks situation. Other mind says not to sell a leader near all time highs.

2 Likes

@hitesh2710 sir, I want to know your views on United spirits.

Almost everything is sorted out now…the management seems superb, they have cut debt like anything in last 3-4 yrs( from 2.5+ D/E to 0.24 now(TTM); growth seems nice going forward(Sin stock).

The only concern to me right now seems valuation, but still its less than the 5 yr median PE.

Govt regulations and raw materials dependency are other factors; however, I don’t take them as too much risk: excise duty is huge in liquor and govt will never afford to lose that…else how will they give freebies like farm waiver and other socialist schemes. Regarding raw materials cost, well this company has a moat and so will pass on the cost to the end consumer, like Asian paints or a pidilite.

Need your guidance please.

1 Like

Is it possible that many investors missed the new earnings guidelines by the management. Initially around April or something, the management gave a higher guideline on 2019-20 profit which they subsequently lowered during a TV interview

initial concal: https://ia902904.us.archive.org/28/items/1-q-19/VinatiOrganics-1q19.mp3

subsequent interview: https://youtu.be/x-_ElWiY6Hw

1 Like

A NBFC does well when it can raise funds easily at lower cost. Going by that, Bajaj Finance is doing it easy even in this situation. And by reports it is also increasing its market share. I don’t know if any one can buy it new but I dont see why someone who has it in their portfolio shouldn’t continue to hold it.

1 Like

Are they not already doing the SDB? Any reason you are saying “if bagged”?

As I mentioned in the earlier post, there will be exceptions which will escape the carnage affecting a particular sector. Most of the times it is the well run sector leader or other times its some other company which has great management and great fundamentals.

Bajaj Finance fits in here. It has a fantastic demonstrated track record of many years and as of now not much fear on NPA front. With the pain in the peer group due to the meltdown, the survivors would probably be the biggest beneficiaries. In the NBFC space, I can see some names like Bajaj Finance, Chola, Sundaram Fin and MAS Fin which seem to have escaped the special treatment meted out to the sector as a whole.

Valuationwise BF might appear expensive but it has done so all these years. As long as the growth numbers reported meet market expectations, the run up in the stock will continue. I wont be too worried about BF on the price to book parameter as we have seen similar valuations sustain in case of Gruh finance through cycles. For a consistently growing NBFC, besides NPA I think PE ratio might be a good guide to judge valuations.

19 Likes

@hitesh2710

sir, wanted to know from you if u are tracking the story on VGuard?

technically, it seems a pretty good accumulation structure, presently converted the 52week moving average from resistance to support, and correcting with very low volumes and action… (based off monthly and weekly chart)

thank you!!

2 Likes

Vguard looks good on the charts. It has been consolidating above its 200 dema since past few trading sessions. On the upside 250-260 could be a strong supply area I would watch closely. Ideally I would like to buy above this congestion zone to ride on a quick swing move. Unless it crosses this zone conclusively, there can be a lot of sideways moves.

10 Likes

@hitesh2710

sir, also wanted to know your opinions on ratnamani metals and tubes ?

if u happen to track this scrip fundamentally and technically…

stock seems to be coming out of a base formation, with multiple tests done at 38.2% level retracement of the 2016-17 run, and presently taken support from 52weekly moving average, after breaking out of its resistance on tremendous volumes, showing signs of accumualtion thoughout the entire base…

also i see, in the SHP, L&t and kotak mf have been picking up around 5 percent new stakes since the past 2 quarters…

thank you!!

1 Like

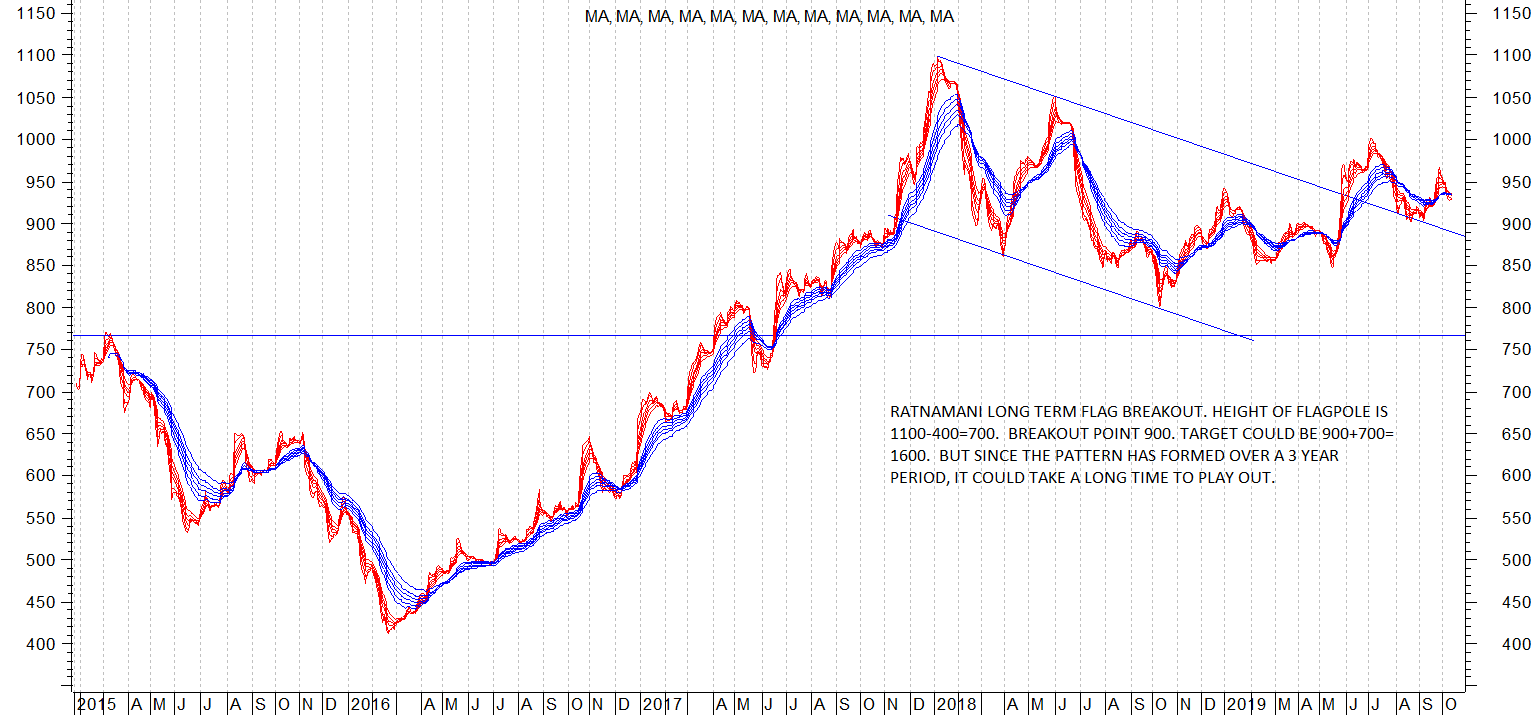

Ratnamani is a very well run company run by a family of brothers (Sanghvis) who have taken the company to a very respectable platform from modest beginnings.

It has incurred huge capex and is likely to reap the benefits of the same beginning FY 21. FY 20 could be a flat/moderate growth year.

Attached chart shows a long term flag breakout as shown by using GMMA. (guppy multiple moving avgs).

15 Likes

@hitesh2710 sir your views on TCI? A decent growth of 15-17% and available at a similar pe. Management with a good and long track record (68% holding as well). Though a bit capital intensive but good interest coverage ratio. An industry which I think has a good growth story ahead.

I dont track TCI too closely. I used to own it earlier and had studied it then. Its a good company in the logistics sector but growth has been moderate and hence unless there is a real small mid cap bull market, there is unlikely to be too much excitement. Valuationwise its fairly valued. Not too cheap, not too expensive. It can be looked at if and when it starts showing fast growth.

4 Likes

Hi Hitesh bhai,

1 What headings and particular items should one see in a banks/NBFC balance sheet to identify asset liability mismatch ? If possible, can you please give an example?

2 What else must one see in a banks balance sheet apart from NPA and NIMS ?

Many thanks

Regarding what to look for to detect asset liability mismatch (and even the bank related query) I think I would request you to pitch this question to @dd1474 who will be better placed to answer these accounting related queries.

2 Likes

Thank you Hitesh bhai.

@dd1474, request your suggestion on the above banking query

Hi Hitesh bhai ,

Which one seems to have great opportunity , high growth prospects between consumer aspirational ( eg Titan) and consumer discretionary ( eg Havells )? Many thanks in advance

@hitesh2710 Thanks for considering me an “specialiist” in this field. While I worked for more than decade in special situations (mainly stress assets management buinsess), only time would tell whether I am specialist or not !!! On a serious note, that thanks for directing query to me.

@A_shah

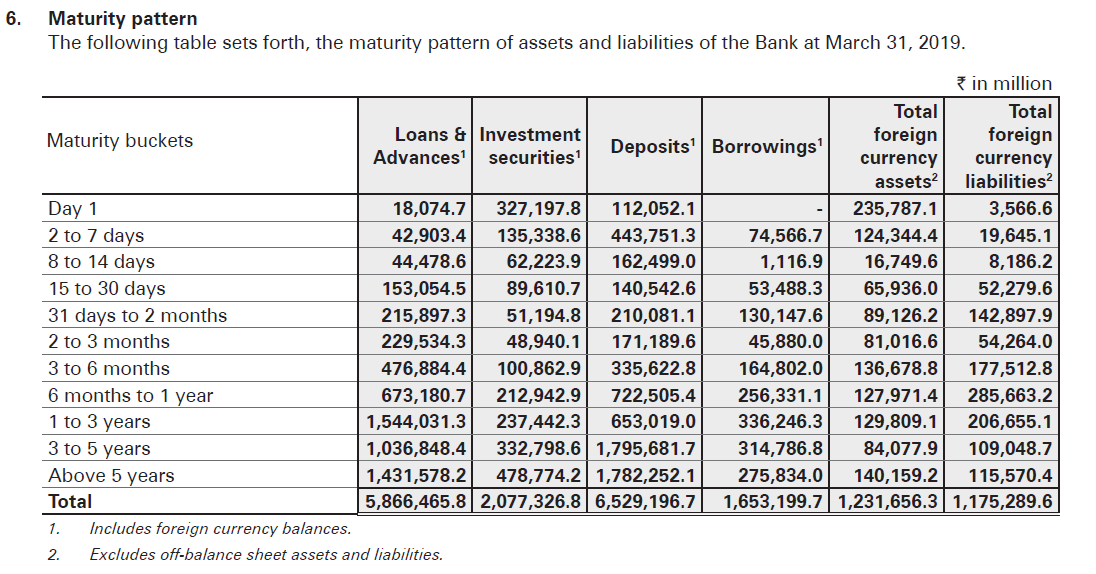

Find enclosed snapshot from ICICI Bank Annual report FY19, page 179,

Find enclosed link to RBI Circular about disclosure in Bank financials, which provide formate for disclosure of ALM (asset liability management) for of the scheduled commerical bank.

https://m.rbi.org.in/scripts/BS_ViewMasCirculardetails.aspx?id=8144#S22

In my limited understanding, we need to add, Deposit and Borrowing liablity side and consider Investment and Loans on assets side to check whether bank run any risk of asset liability mismatch.

Even NBFC are expected to disclose ALM in some what similar formates. Find enclosed RBI directon to large NBFC about same.

https://www.rbi.org.in/Scripts/BS_ViewMasDirections.aspx?id=10586

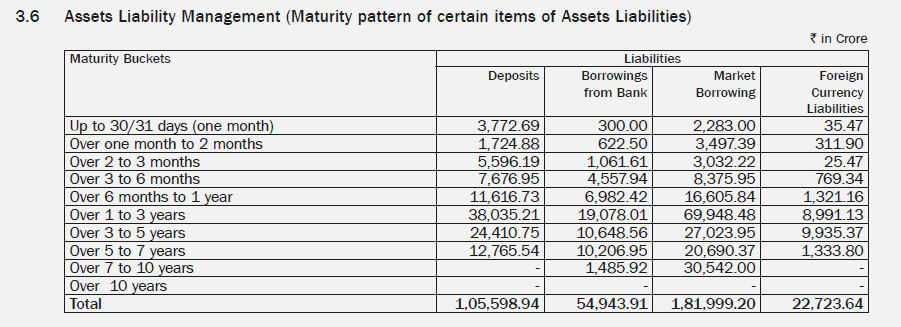

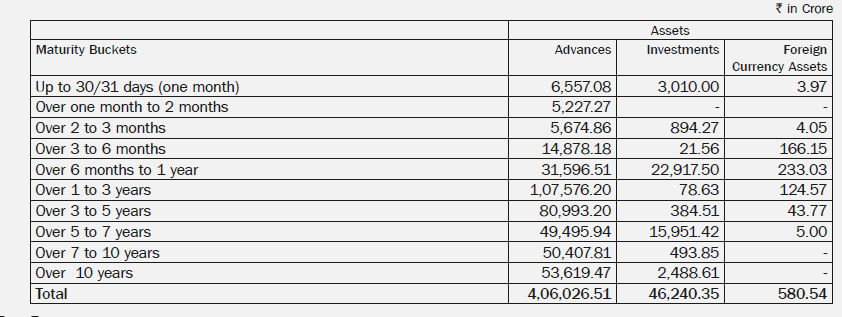

Find enclosed HDFC Limited disclosure about ALM On page 208 and 209 in FY19 annual report.

Hope this answers your query.

17 Likes

Thanks so much @dd1474 for the detailed revert . It’s very helpful

Apart from the above AL mismatch and NPA and NIM , what other essential things should one look for in a banks and NBFC balancesheet ? Thanks once again

Comparing titan with havells is not a fair comparision. As you highlighted, both cater to different segments of consumer baskets.

Titan’s main business segment is jewellery followed by watches and other startups like SKINN perfumes etc. We need to see how it develops new lines of businesses.

Havells has a much wider basket and it keeps adding newer products through innovation or through inorganic route (recent AC acquisition).

If I had to make a choice I would choose Havells even though the competition is more fierce in its segments.

5 Likes