I dont track this sector too closely but you can address this sector questions to @suru27 who seems to be tracking the sector and SIS specifically. I think he has posted the details on the thread of SIS.

1 Like

I havent tracked honeywell too closely so not much idea. I think @dd1474 could be a better resource person as i think he tracks it.

1 Like

@hitesh2710

Hello hitesh sir,

Would like to know your views cholamandalam finance as a long term bet in one’s portfolio given that they are doing reasonably well compared to peers in the current nbfc situation and management seems confident in concalls.

Hiteshbhai

Please share Your views on Multibase Ltd…

As corrected significantly and some big moves taken by promotor Dow how u look at that?

Thanks

Chola remains one of the better managed NBFCs. It primarily caters to the CV segment and other vehicles. It also has presence in the home equity segment. Results till now have been good. Only problem is that with the severe slowdown in the auto space, it might find difficult to keep growing at earlier rates. This year due to the implementation of BS VI norms there could be some pre buying and lead to some growth but one needs to consider the prospects of growth for FY 21.

Multibase has corrected because a big component of its business , antifoam segment contract with the parent has been terminated. How the company manages to revive growth in absence of this segment needs to be seen. Stock price has corrected a lot in sync with the news.

4 Likes

Sir,

May we know ur views on Hester Bioscience for long term? Also some insight into its valuations, if possible. Thank you.

1 Like

Hester Bio has been a great growth story over the past few years. Company is in a niche space of animal vaccines and poultry vaccines. The promoter ceo Mr Rajiv Gandhi seems to be capable guy and articulates quite well in all concalls and of late has been delivering and even bettering on his projections.

The Nepal plant has not lived up to expectations but now they will have the African plant to start contributing to growth.

At current juncture I think valuations dont leave too much for an investor in the near term but if someone were to accumulate this company on declines patiently it can be a good bet.

14 Likes

@hitesh2710 ji,

I was seeing the product list of Transpek Industry. As per my understanding, these are not new compounds, so they can’t have patent on any of these. The pharmaceutical or agrichemical industries which require the chemicals can also produce the compounds in house.

However, a company focused on acid chloride industry is able optimize the production, reduce pollution etc. They can also have process parent in case they discover a new cost-effective way to produce these chemicals.

My question is, where is the competitive edge of these kind of companies. Why can’t another company start producing the same chemicals and take away the profit? Is it customer trust, lowest cost production, or anything?

I understand that the company is still small and there is huge space of growth but is the industry so big to accommodate more players like them?

1 Like

Hiteshji,

2013 to 2017 end, the market players were gung-ho about small and mid caps and drove them sky high and large caps were shunned by them during the period. Then the small and mid caps tanked and the

investors in them started staring at deep losses. Meanwhile Sensex and Nifty went on to hit life time high with large caps outperforming and most of the money chasing them. Most of the large caps seem priced to perfection now whereas many of the small and mid caps are hitting 52 week lows. Now there is talk of more value in mid and small caps and risk reward is better in them etc. Now the question is with many having burnt their fingers investing in small and mid caps, will they not be trading sideways with negative bias for another 3-4 years before making a strong come back? If the question is inappropriate, moderators please remove.

10 Likes

Any views on inox leisure sir seems company on solid track as per recent results and company cocall.

Thanks And Regards

Ashish

Hi Hitesh,

What is your view on Transport & Logistics sector for next 3-5 year period? Why company or stock do you like or is in your watchlist?

Thanks,

Anil

Hi Hiteshbhai,

Had a query regarding consumer durables/consumer electric sector . Request your views on the same .

1 Companies in consumer durables or consumer electricals sector are in a way secular as they are consumer facing however being consumer discretionary , they progress only when economy prospers unlike FMCG . They are also subject to raw material price fluctuations . In such a case are they to be considered secular like Asian paints etc or are they cyclical industry ?

2 Whats the future growth prospects of consumer durable or consumer electrical sector (companies like Havells , V guard) and is lesser prone to disruption ? Alternatively , can these be considered coffee can companies ?

3 Banking/NBFC stocks are considered very risky and hence one looks at only "perceived " quality stocks like HDFC bank , Cholamandalam , Sundaram finance , HDFC ltd , Bajaj finance . What could be the reason for Sundaram finance to not have kept pace with other peer companies growth rate ? Can one plan to invest in Sundaram finance in the Hope’s of value unlocking by way of demerger of its subsidiaries in future ?

Many thanks for always explaining amateurs like us to the nuances in a simple manner as also warning us against risk of investing in risky businesses .

2 Likes

Very interesting observation and a pertinent query especially looking at the current market scenario.

I myself was seeing such market behaviour after a long time. I think the last time I saw such bipolar movement in the markets for such a long time was back in 2012-14 period just before the BJP came to power for the first time. Post that the small-midcaps took off somewhere in 2014 and the party went on till 2018 January.

Usually these days correction in any segment or subsegment of market (large or small or mid cap) tends to last 12-18 months. We are almost nearer to the 18 month period. Thats not to say correction can be over soon.

But looking at the overall apathy and bipolar movement and people shunning the small-midcap space since a long time, I think we might be closer to a bottom in these segments.

If the above hypothesis is correct then the question arises what to do and where to look out for the next set of big winners.

This is the kind of situation where reading books like The Next Apple or William O Neill’s book How to make money in stocks (canslim method) helps in formulating a strategy.

Ideal thing to do is to look out for companies which have consistently posted good numbers and whose prices have not taken a beating as has happened with companies with mediocre results.

In the current market what happens is that there will be price spikes for short period of time after good set of results and sometimes stocks manage to hit 52 week or all time highs and then prices tend to retrace and move around in a tight price range which we term as consolidation. This kind of situation is ideal for picking up winners. These are the very stocks which are going to create lot of wealth over next few months/years once the market starts developing a taste for small-midcaps.

The other spectrum of the stock picker’s fertile range is to look out for companies which have posted good results but have moved off their lows and are now comfortably consolidating in a tight range well above their 52 week lows. At this stage of the markets these companies are the companies which no longer post fresh lows on a regular basis. These are the companies that need watching. These are the companies which are good to great and are undergoing time correction after multi year bull runs.

The thing I feel that needs to be avoided is to catch falling knives in the false belief of being too clever and knowing too much often much more than the markets. These are the situations that often end up giving painful lessons at high tution fees.  There can be the odd situation where one can get lucky or smart or both and make good amount of money but one needs to see how much capital has been allocated to this situation to make a meaningful difference to portfolio returns. In all other cases these are situations which if turn out to be right provide a lot of bragging rights without too much to show in bank balance.

There can be the odd situation where one can get lucky or smart or both and make good amount of money but one needs to see how much capital has been allocated to this situation to make a meaningful difference to portfolio returns. In all other cases these are situations which if turn out to be right provide a lot of bragging rights without too much to show in bank balance.

73 Likes

Whether J B Chemicals & Pharmaceuticals Ltd and MAS Financial Services Ltd falls into such category

Hiteshbhai, can you please suggest any tools to identify such stock? What data points, websites etc one needs to look for to identify such stocks? It would be great if you can name a few stocks, if any, on your watchlist. @hitesh2710

Hiteshji,

Thank you for the enlightening reply. Does RBL Bank and DCB fit the bill? Posting good results, hitting all time high, retracing and consolidating? Please delete if the questions are inappropriate? Invested in both of them.

4 Likes

Thanks Hitesh Sir for enlightening reply. What is best way for stocks which start falling after purchase for short term. Is it better to sell it off once its certain percent down? Are they other strategies.

Thanks.

JB chem and Mas fin would fit the bill for companies showing relative strength. And posting 52 week highs. But that doesnt mean we go out and buy them tomorrow. Its only a starting point for idea generation and one needs to analyse the company in question and figure out the triggers that would make a winner out of it.

3 Likes

Hitesh Sir, Greetings! Thanks for your note on LUX industries at the Goa 2019 Chintan

Growth surely seems to be there even in comparison to PAGE, the market darling.

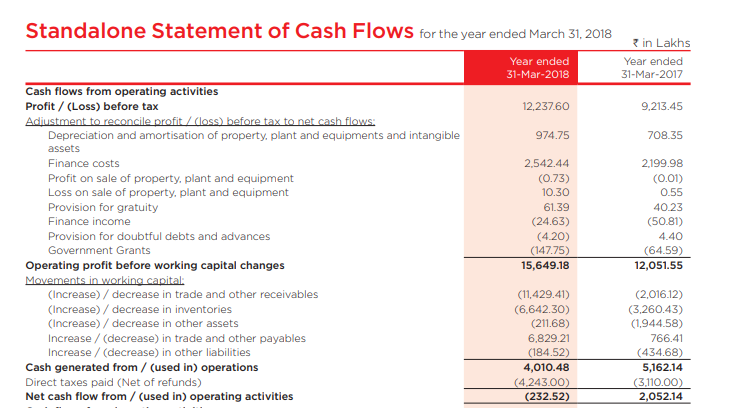

But the top concern based on my limited reading is - Rising Investories and Recievables

Kindly guide if you have any further information on the front.

And the larger question here is on the economy, if an inner wear player has to increase working capital by increasing payables, what does it imply? or maybe is it more pronounced for the SME sector of the economy?

1 Like

Hi Hitesh

Did you check promotor quality??