Regarding DHFL, one needs to know that markets pay not for glorious past but rosy future. Anyone having a cursory look at DHFL fiasco can easily make out that the future looks bleak. Kapil Wadhwan showing confidence on TV is something that is inevitable for a man in his position. Imagine him outlining his problems honestly on TV and the impact it will have on investor psyche and stock price.

I am one who usually avoids falling knives and sometimes have missed multibaggers in the process. The lure of big bucks often takes the eyes off total capital loss. I would suggest you read the thread of DHFL on VP fully and make your own conclusions.

I had a look at srikalahasti pipes some time back and was dismayed by the sudden disappearance of cash from balance sheet and couldnt connect the dots. While the business prospects and valuations remain attractive, I tend to avoid these type of companies where I am not too sure about promoters/management or balance sheet issues.

Hi Hitesh ji, between KEI, Polycab, Finolex cables, what is your opinion? Polycab is comparatively bigger with market base, growing faster… Let me know your thoughts…

Hi Hitesh bhai,

Whats your view on CCL whether can it be considered a company which can keep on growing even though it faces competition from Nestle , Bru etc in view of expanding market size ?

What level of growth can one expect to continue for 5 years in revenue considering that the capacity expansion has been almost done and whats your view on the retail foray ?

Many thanks in advance

After your suggestion I nowadays view companies with pledge with suspicion. But what percentage / trend of pledging is optimum to brush off a company from the wish list?

I have these two companies in my wishlist with around 15-25% pledge. In the past these companies had even greater pledge which they’d diminished afterwards.

KEI is largely a b2b player though of late it is trying to get higher revenues from b2c segment and the plan to is take this chunk much higher. But having followed it since past few quarters, in my definition it falls in the good category. (not great) Its a laborious business wherein the company has to keep expanding capacities to keep growing. Opportunity size remains good.

Polycab is a bigger player than KEI but I havent looked at it in too much details. I see some ads related to its products so it too might be aspiring to have higher revenues from b2c segment.

Finolex cables is a very old company and has been well covered on VP thread on the company.

All these businesses I feel are quasi ancillary plays on cap goods revival besides being steady growers. But there is a limit to how much margins they can improve and how much valuations/rerating these companies can command.

I had bought KEI sometime back as a techno funda bet and got out around 450 thinking it had reached fair value only to find I was a bit premature in selling.

I feel these kind of businesses have to be bought cheap and sold when markets give them higher valuations as I think these will always remain high beta stocks. Moves being magnified on either side in sync with market movements.

Since I have observed it, I have found CCL to be a company that has flattered to deceive. Every quarter they dont perform, they have some or the other excuse and you feel this is one off and then within a quarter or two something else turns up to haunt it. The only good thing about the stock is it seems to be in the hands of strong players most of whom have strong conviction in the story and hence the stock price is able to survive disappointing numbers thrown up off and on.

But if one looks at price pattern, since 2 years back in March 17, it posted its all time high, investors in the company have hardly made any money, while no brainers like HDFC Bank might have given 50% or even 100% returns. So the question that needs to be asked is do we need to be too clever? Or just be dumb and buy sure shot things like HDFC Bank and make decent money.

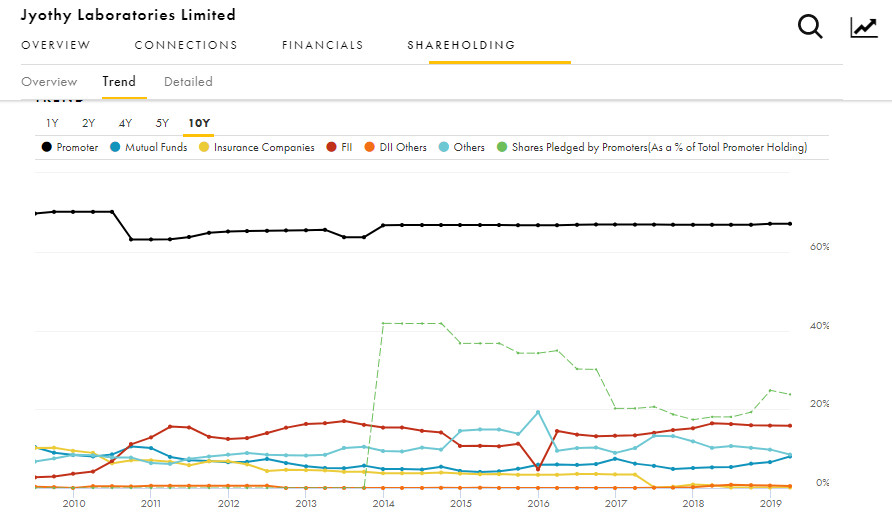

Promoter pledging is a factor which cannot be looked in isolation. If the business is great, predictable and consistent in numbers, then small amount of upto 25% (of total promoter holding) can be ignored to some extent. And one also has to look at the promoter history on how they have treated minority investors in the past and how they have conducted their business.

I think in both Jyothy and Ajanta, the promoters till date have not done anything to shake investors’ confidence and have run the business pretty well, within the limitations of the constraints of the sector.

Another factor to be seen (and you mention it) is reduction of percentage of pledged shares over a period of time.

@hitesh2710 ji,

Thank you as always for your precise & insightful response. I learn a lot from you.

My next question is on investment in holding companies.

Case 1:

Suppose I am interested in the growth prospects of Company A, & Company B.

Company B holds some percentage of ownership of Company A & also has its own operation.

Should one invest in both Companies A & B or only in Company B?

Example:

Company A (CDSL) & Company B (BSE)

Case 2:

Suppose I am interested in the growth prospects of Company C, & Company D.

Company D is unlisted.

Company E holds some percentage of ownership of Companies C & D, but doesn’t have any operation.

Should one invest in both Companies C & E or only in Company E?

Example:

Company C (Cholamandalam Investment and Finance Company), Company D (Cholamandalam MS General Insurance Company), Company E (Cholamandalam Financial Holdings).

Should the ownership percentage matter in the decision making? 20% vs ~51%?

@sujay85, Laying aside all these A, B, C, D and Es the most important aspect of investing in a growth company is to directly invest in that particular company rather than the holding company. The company that shows growth is going to be rated accordingly by the market whereas one is not too sure about the kind of holding company discount that will be applied to the holding company.

For me the path is plain and simple, Buy growth companies if they appeal to you, rather than trying to be too clever and buying holding company at a substantial discount and hoping markets gives you the rewards of the growth company and reduction of holding company discount.

I feel as investors we need to simplify things rather than complicate by taking circuitous routes. I see a lot of discussions on DHFL thread with lots of interpretation of events and newsflows, when the prudent thing would have been to avoid it (or get out as soon as possible) as soon as shit hit the fan.

But the lure of making quick bucks on rebound is too much to resist I guess.

@hitesh2710 Bhai. Any views on Honeywell Automation India ? The company has given spectacular returns in past being a MNC, debt free and a decent growth company with support from Parent. Market Leader in India as it excels in Industrial Automation and primary domain being Oil & Gas along-with building materials/construction, environment control sensors etc. The future looks good as alongwith Hardware manufacturing its even looking to complement that with software also making a complete solution.

My intention towards investing in Holding companies was a bit different; to reduce the number of companies in portfolio.

For example, if I like Zydus Wellness, Cadila Healthcare, HDFC, HDFC Life, HDFC Asset Management (total 5 scripts), I am theoretically getting the same Investment exposure by investing in Cadila Healthcare & HDFC (2 scripts).

I understood your point, nevertheless! Thank you as always for your continued mentoring.

Great learning this for amateurs like us to avoid the " fear of missing out " syndrome

Hitesh bhai , deeply appreciate your guidance to amateurs like us

Is one correct in assuming that since one is unsure of the holding period of holding company and so required valuation is not given of the high growing subsidiary ?

Between HDFC bank and Bajaj Finance , which one , according to you has more growth potential ?

Many thanks

@ankitchandra, I think sterlite tech is not a company where one can take a 5 year call confidently. As can be seen from the product price scenario that has changed drastically over the past few months, this business comes across as a commodity (or slightly better than commodity though i am not too sure) business and in these commodity businesses there will be cycles of demand and supply and their mismatches.

On top of that you add the sterlite group management which is not too well known for top notch corporate governance and it would make a deadly cocktail if prepared for a 5 year period.

Hi Sir - if possible, may I know your views on companies which provides temporary staffing, in particular, Teamlease. There are a few other companies such as Quess where Fairfax is the majority stakeholder and SIS. Could you please let me know your thoughts as your time permits? Thanks