I’d say the debate between portfolio diversification and concentration is rather meaningless. The former is protection against ignorance and is much suited toward people who don’t know what they are doing. On the other hand, if you understand what you are doing, it simply makes no sense to allocate capital to your 7th best idea; let alone your 20th best idea.

Imagine yourself as the owner and CEO of Godspeed, a business that is the best in the world at making its product ecosystem, X, and making a lot of money selling it. Being the frugal potato that you are, you also manage to keep your costs ridiculously low. However, for a bit of perspective about how to deploy your cash hoard, you happen to hire Mr. Suit Nice Tie, a charming financial advisor who has an MBA from a much respected institution and who for a fee stumps you with “Hey, you know, what happens if we can no longer do X?” “The man has a point,” you think. Now instead of focusing your effort on ensuring that X remains relevant in the future by stepping up your game and widening your moat, you could then spend time on finding out alternatives to X. Aye, it could make sense to have one or two of these alternative sources of income especially if it expands your ecosystem and deepens customer mindshare, but if you were to do entirely unrelated things you’d risk becoming the jack of all trades.

For example, imagine if Apple started its own airline, iFly, in the name of diversification. “What a wonderful idea that would be! People love the iPhone. They will surely love the airline, especially if it is coming from Apple!”, an exuberant Mr. Nice Tie would remark. Well, if Apple started its own airline, instead of making 5 times as much as it spends, it would then have to spend 10 times as much as it would earn. Now that wouldn’t be a great way to allocate capital, would it? It might very well be a stellar and remarkable product, but if it costs you more to maintain it than it can make, it doesn’t matter how good the product is; you would lose money. And you know what they say about losing money: don’t lose money. Therefore, being the more practical smarty-pants, you would gently ask Mr. Suit Nice Tie and his band of jolly fellows who can tweak their spreadsheets but refuse to use a little bit of business judgement, to pack their bags and clear their desks on the way out. It wouldn’t hurt to vow to never hire Mr. Suit Nice Tie and his elk again. Imagine all the unnecessary salaries and severance packages you would now not have to dole out.

I’m not sure how doing 10 things mediocrely can equal doing a couple odd things brilliantly well. If I find a great idea and understand what I am doing, I’d swing for the fences. It makes no sense to take a single on a free full toss. I’d hit a 6, and there would be no two ways about that. The choice between concentration and diversification is analogous to that between the marvelous and the mediocre. I cannot settle for the latter. You might want to choose your own outlook after a wee bit of deliberation and a dose of fine whiskey. While I’m certain you’d find your own path, I do have a bit of well-meaning advice: if you buy a business buy it with the intention of never selling it. That rule of not being allowed to sell alone will force you to make substantially better selections.

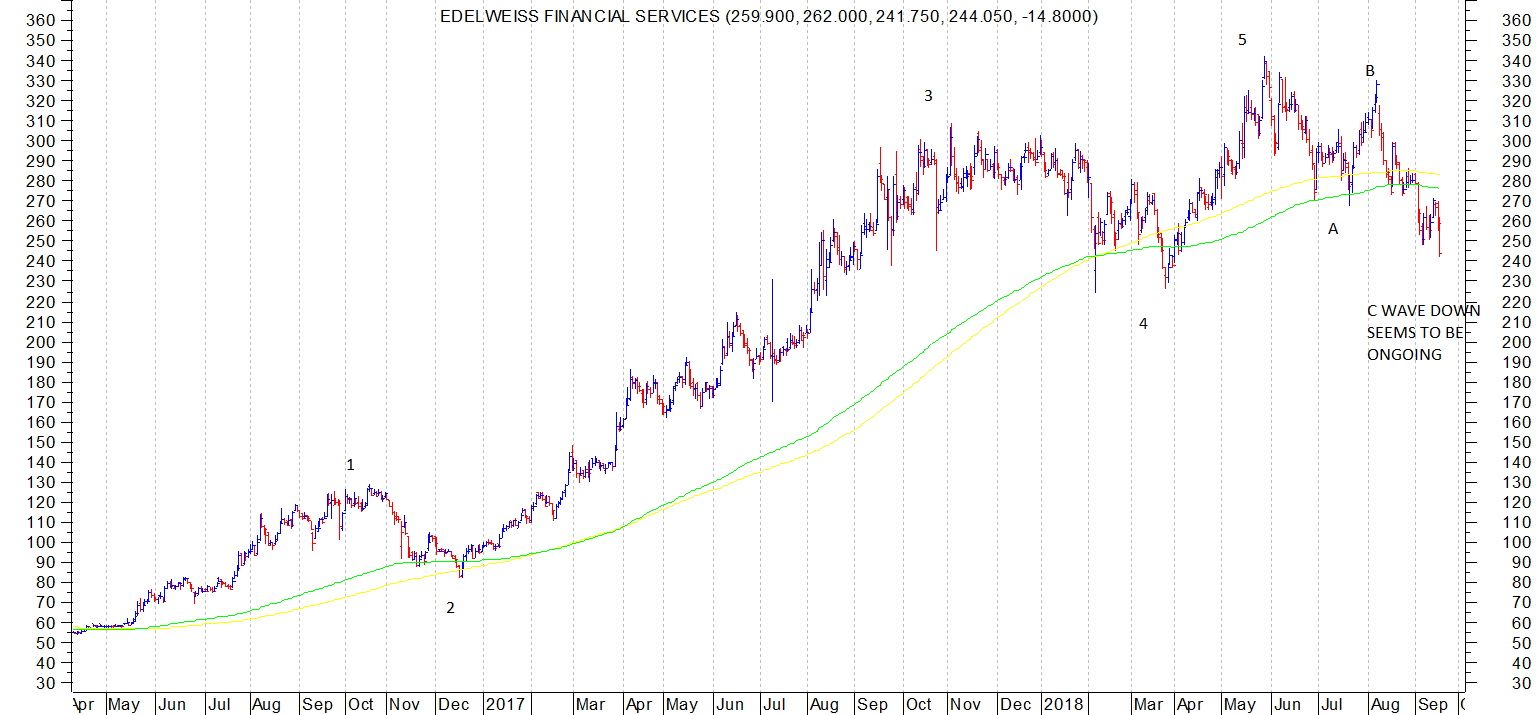

It was an interesting analysis for me as I never thought distress period can last so long for gold unless saw numbers, will put it in detail sometime

It was an interesting analysis for me as I never thought distress period can last so long for gold unless saw numbers, will put it in detail sometime