Fundamental questions on IOB

Rating Rationale (crisil.com)

-

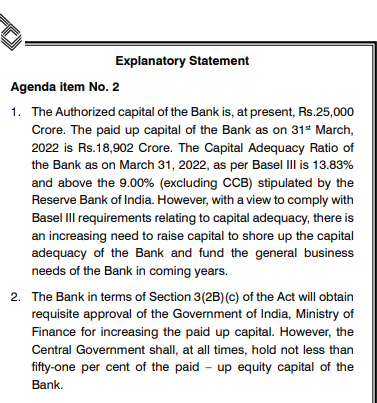

GOI going to raise capital of ₹1000+200 Cr(ESOP) in FY23. Dilution of 6%

-

GoI has infused ₹ 22,974 crore in IOB over the past four fiscals,.

-

General Article on state of PSB’s : Public sector banks are steadily gaining strength (indiatimes.com)

-

Became profitable since FY21: The turnaround story of Indian Overseas Bank - The Hindu BusinessLine

Do you think RBL banking tanking since appointment of R Subramaniakumar is down to markets perception of bank’s books or the ex-IOB man’s leadership? -

We aim to achieve a 25% year-on-year rise in net profit every quarter this fiscal

Concluding thoughts:

-

It appears worst phase is over. Still concerned as this not an Investment I would have made

-

Can’t decide if raising capital is good or bad

-

Rough Valuation : BV * P/B * Earnings growth

Case a: 12 * 1.5 * 1.20 = ₹ 21.6

Case b: 12 * 1.8 * 1.25 = ₹ 27

Please share your valuable insights. Kindly excuse the use of links as vp thread has been quiet for this one