An interesting thread indeed.I read all concalls and Annual reports since the demerger to gain some insights into the fluctuating revenue and profits. My two cents:

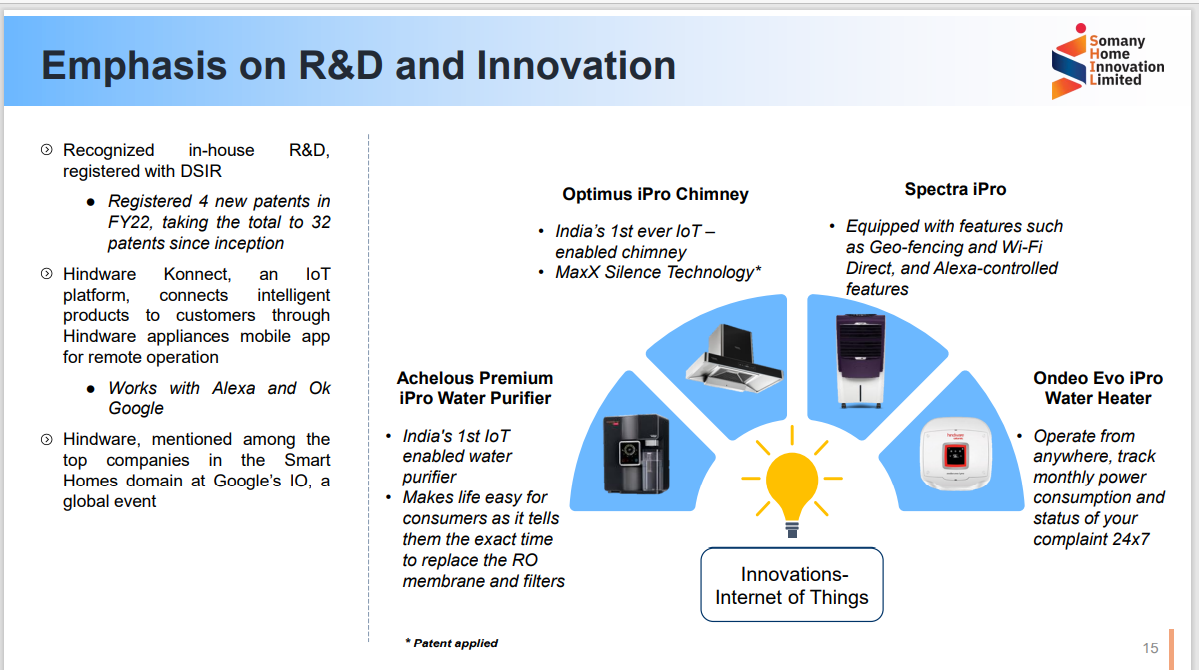

(i) SHIL is heavily investing in R&D, JVs and tie ups to expand it’s product portfolio of IoTs.

One major takeaway is company is trying to innovate and bring in technology in most of the product be it faucets, heaters,air purifier, chimneys or sanitarware which as a result has put it in strong postions in all the verticals. Moreover, studied the product lines of Cera and parryware etc though it has been consistently rolling out new products, IoT enabled product offerings are less as compared to SHIL Company has gained traction after having the first mover advantage in IoTs.Good to see management understanding the market sentiments and future growth drivers.

Lost its market share to Cera 2-3 years back however capex and R&D efforts are reaping results.

(ii)Is continuously trying to reduce raw material dependency from China and other foreign suppiliers. Aims to reduce kitchen appliance raw material import from 90 to 15-20% . Will result in being less susceptible to global supply bottle -necks.

(iii) Signs of Real estate demand picking up in tier 2 and tier 3 cities in last 2 quarters will be a massive driver for sanitaryware after some years of muted growth.

(iv) Management vocal in addressing that geographical areas where they have a weak presence.

(v) Weeding out inefficiency: Shut down 8 IVOK retail stores which as a result has helped to turn EBIT positive in last quarter.

(vi) Targeting an EBITDA range of 15-16 % in next 5 years. If margins expand , will imply more cash flows , better return ratios, thus better value.

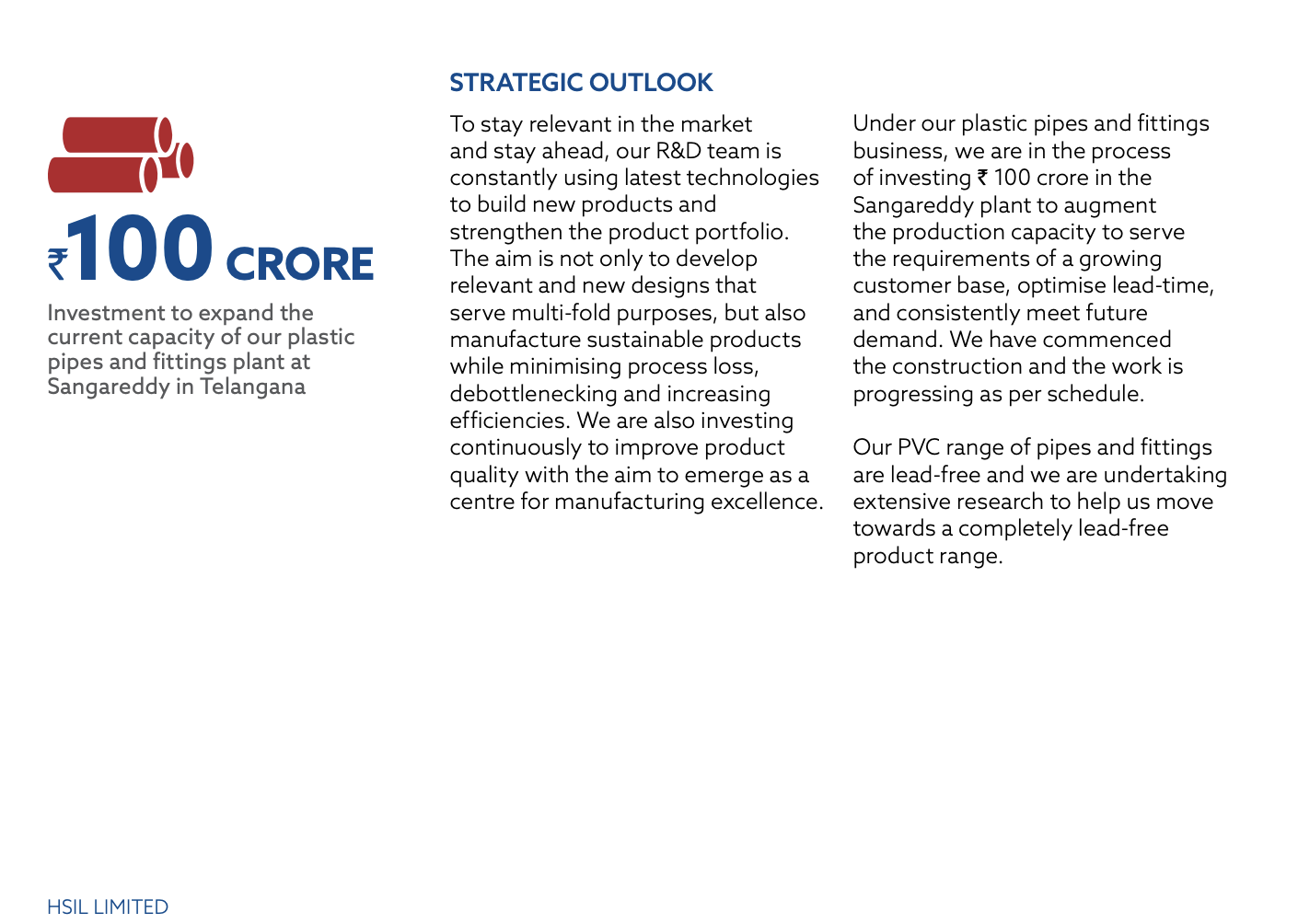

(vii) Pipes and fittings business has been a major determinant for double digit growth of Building products, however will be interesting to see if Truflo can gain the market share of the big guns(Astral, Prince, Supreme,finolex ) in this sector. Will it be able to sustain high growth in a very competitive industry? What does it offer differently to outgrow it’s competitor in case of downturns?

(viii) Since SHIL financials has been quite volatile over the last few quarters and not so much information for reliability of management execution on an independent basis, it Boils down to whether the management can “Walk the talk” of 20+ CAGR in next 5 years?.

(ix) Rise of UPI coupled with consumer online shopping sentiments change post Covid ,will benefit organized players and offer more opportunities due to higher visibility of online products.)

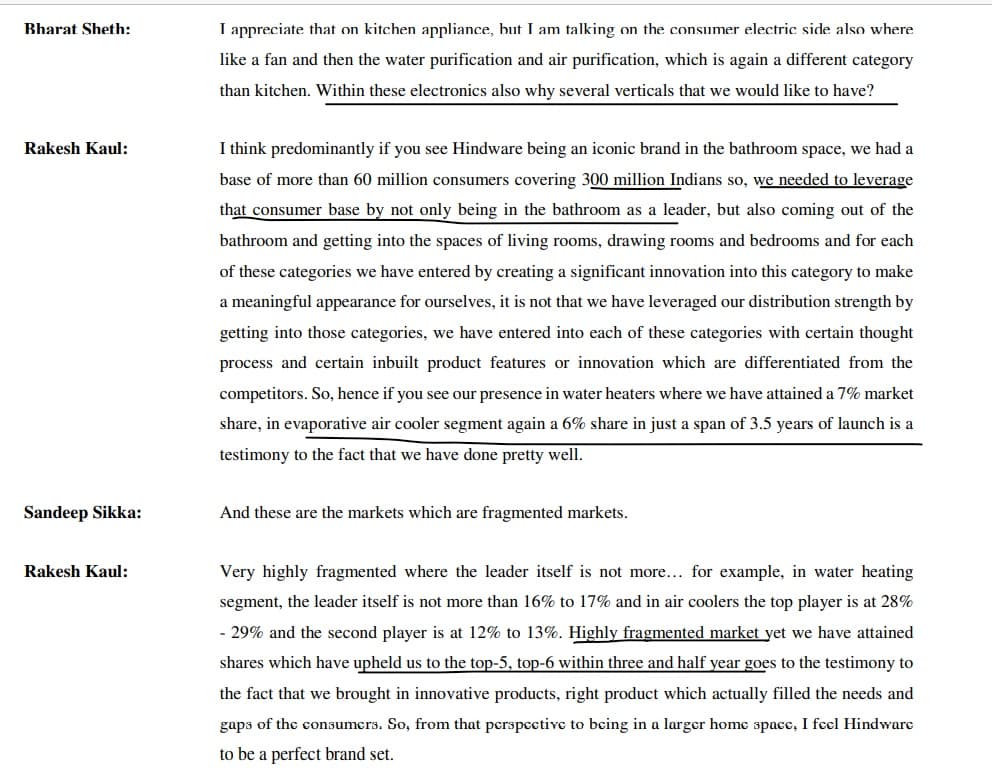

(x)However personally liked the fact 7 years prior, although being the market leader the parent company didn’t grow complacent .Took an aggressive approach and Forayed into faucets(more volume growth factor vis a vis Sanitaryware )thereby increasing their TAM. Also entering into pipes, home appliances and retail has leveraged it’s TAM by 10x. The company is in the top 6 players in every segment it’s in! Having 3 different streams of revenue and wide product line reduces the overdependence on it’s primary Sanitaryware vertical.

(A good question asked on over-diworsification and nicely answered as well)

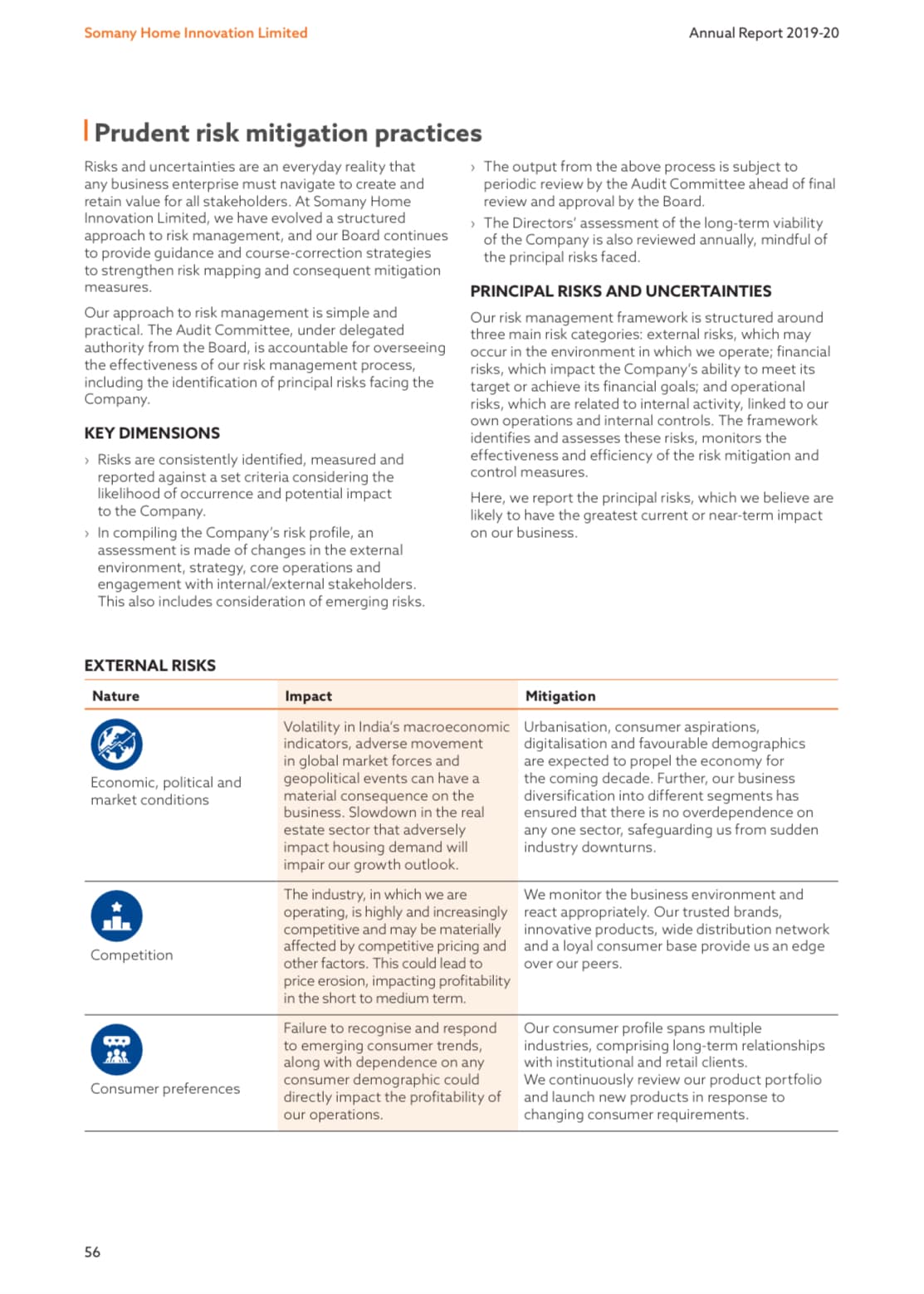

@Dinesh.Bomma @vnktshb Would like to know what key risks you foresee other than Execution capabilities?