Hind Zinc -

Q4 and FY 26 results and concall highlights -

Q4 outcomes -

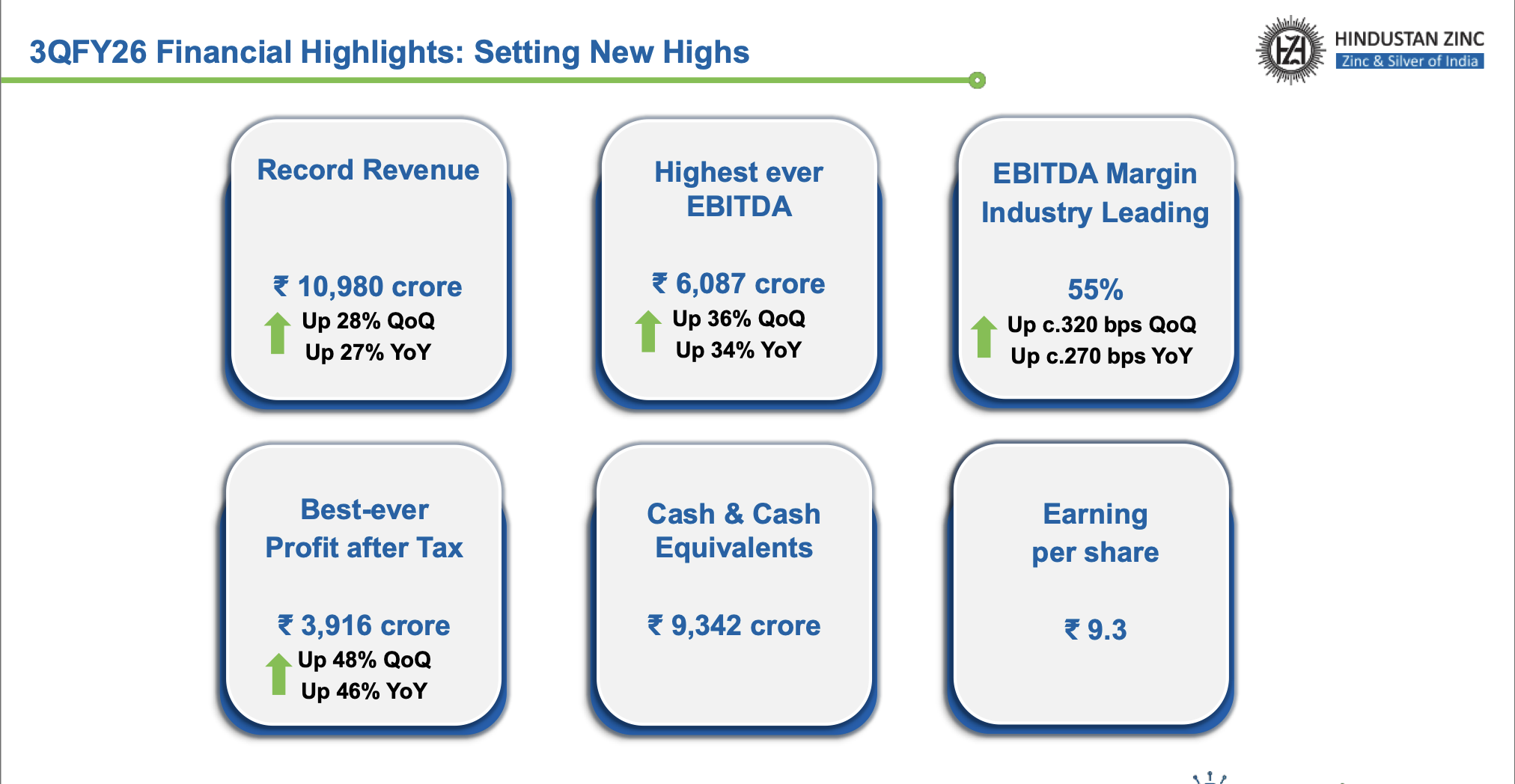

Revenues - 13544 cr, up 49 pc

EBITDA - 7747 cr, up 61 pc

PAT - 5033 cr, up 68 pc

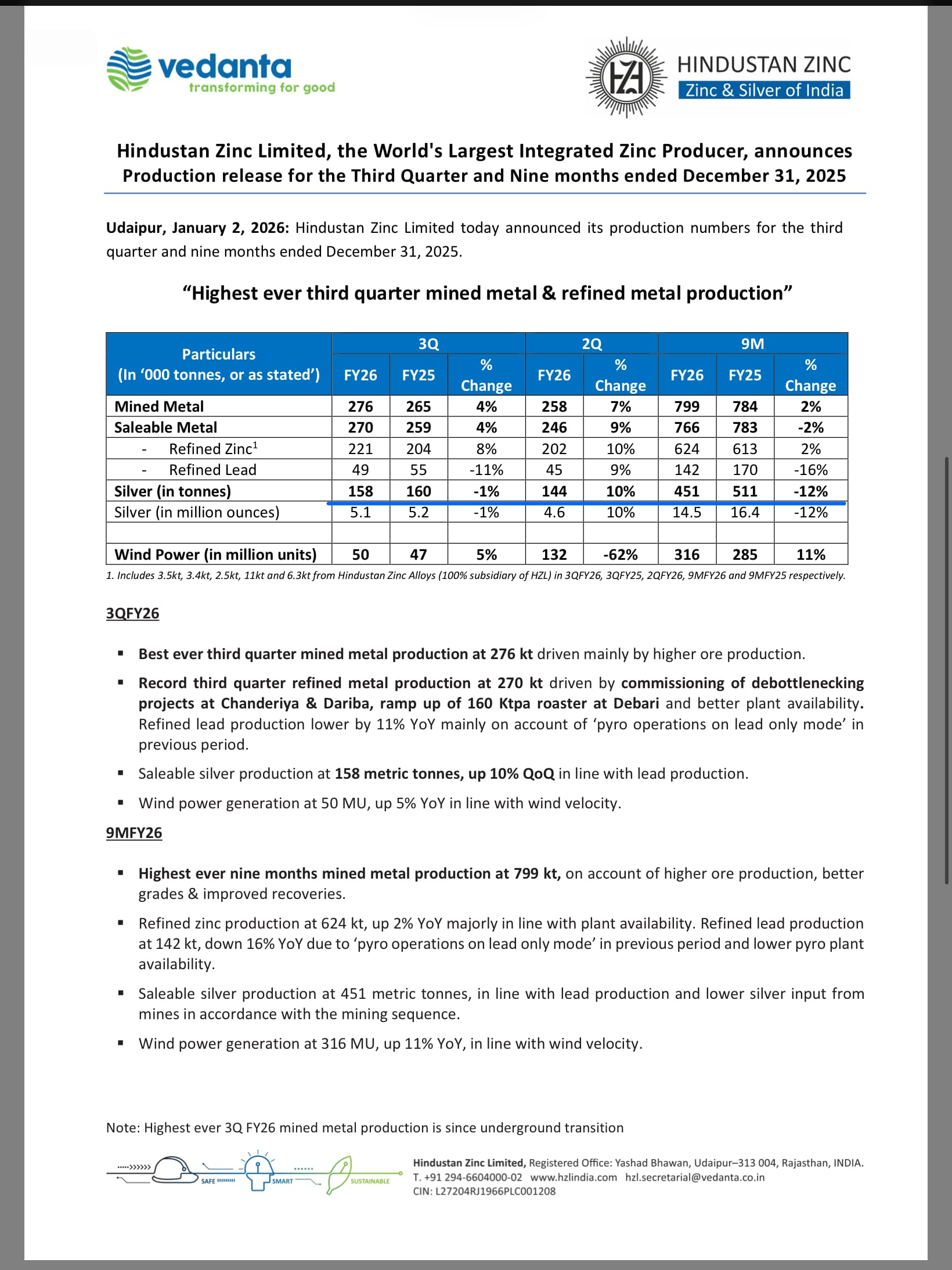

Mined metal production @ 315 KT ( or 0.315 MT ), up 2 pc YoY

Refined metal production @ 282 KT ( or 0.282 MT ), up 5 pc YoY

Qtly Zinc CoP @ $ 903 / MT ( excluding royalty ) - down 9 pc YoY

FY 26 outcomes -

Revenues - 40844 cr, up 20 pc

EBITDA - 22162 cr, up 27 pc

PAT - 13832 cr, up 34 pc

Mined metal production @ 1114 KT - highest ever

Refined metal production @ 1048 KT - second highest annual production

Annual Zinc CoP @ $ 959 / MT ( excluding royalty ) - down 9 pc YoY

Notes from previous concalls -

Company has commissioned expanded smelter facilities ( post expansion ) @ Derbari and Chanderia in Q2 and Q3

Hot acid leaching plant @ Darbaria for additional recovery of 27 MTPA of Silver and 6 KTPA of Lead is expected to be commissioned by Mar 26

510 KTPA - DAP fertiliser plant ( DAP is mainly imported into India ) is expected to be commissioned by June 26. It ll be producing DAP fertiliser and NPK nutrients. The fertiliser plant that the company is expected to commission next FY has the potential to do peak EBITDA of 450 - 500 cr / yr

Company has commissioned expanded smelter facilities ( post expansion ) @ Derbari and Chanderia in Q2 and Q3 Hot acid leaching plant @ Darbaria for additional recovery of 27 MTPA of Silver and 6 KTPA of Lead is expected to be commissioned by Mar 26 510 KTPA - DAP fertiliser plant ( DAP is mainly imported into India ) is expected to be commissioned by June 26. It ll be producing DAP fertiliser and NPK nutrients. The fertiliser plant that the company is expected to commission next FY has the potential to do peak EBITDA of 450 - 500 cr / yr

Company has set up a dedicated subsidiary - Hindmetal Exploration Services Pvt Ltd - to continuously focus on exploring, discovering, developing and tapping mineral resources. The subsidiary has interest in exploration of all minerals across the globe by implementing best in class technologies and practices

Company’s smelting capacities -

Zinc smelting capacity @ .913 MMT + .16 MMT ( recently commissioned @ Derbari ) + .21 MMT ( recently commissioned @ Chanderia )

Lead smelting capacity @ .210 MMT

Silver refining capacity @ 800 MT

Have announced a capex of 12000 cr for setting up of 250 KTPA zinc smelter @ Debari ( next round of expansion ). Have already started work on ground ( yet to finalise the technology to be used in the Smelter ). This should take 2.5 - 3 yrs before it goes commercial

Have announced Capex for India’s first Zinc Tailings reprocessing plant. It will be transforming waste into valuable resources while contributing significantly to circular economy

Key highlights -

Feed capacity: 10 MTPA

Total approved investment: ₹ 3,823 crore

Target completion: 4QFY28

Zinc tailings are fine-grained, solid waste materials left after extracting zinc from ore, composed mainly of silica, alumina, iron oxides, and other minerals, posing environmental risks but also holding potential for reuse in construction (roads, concrete) or reprocessing to recover residual metals, turning waste into resources

Electrification and Renewable energy themes are a tailwind for Zinc ( used in Galvanised steel for Solar panels + Wind energy Infra ) + Silver ( widely used in Electronics, Batteries, Solar panel coatings )

In domestic Lead mkt, company’s mkt share is > 90 pc. Their domestic mkt share in Zinc is around 75 pc

Continue to hedge 15-20 pc of their total metals output ( holds for all three metals )

Have spent $ 180 million as growth Capex in FY 26. Will be spending around $ 300 million / yr wef next FY ( talking about growth capex ). In addition, will be spending $ 400 million maintenance capex / yr

The share of renewable energy as a percentage of company’s total energy consumption for FY 27 should be around 30 pc and around 70 pc for FY 28. This would eventually lead to 300 cr / yr kind of cost savings vs FY 26 ( where the company shall exit with renewable power share of 20 pc or so )

Notes from Q4 concall -

Additional 400 KT and 200 KT smelters for Zinc and Lead are in conceptualisation stages - to be set up at existing locations. This should take the total refining capacity up to 2000 KT { from 1129 KT - currently ( 920 KT of Zinc + 210 KT of Lead ) + Debari Capex of 250 KT }

Also aim to scale up refined Silver production / yr to 1500 TPA from 800 TPA ( at present )

Aim to indulge in aggressive exploration activities ( @ Zewar and Rajpura Dariba clusters ) to sustain mine life > 25 yrs at all times

Cash on books @ 13846 cr

Segmental revenues for Q4 -

Zinc - 6997 cr, up 19 pc

Lead - 1153 cr, up 12 pc

Silver - 4032 cr, up 139 pc

Others - 1362 cr, up 164 pc

Avg metal selling prices for Q4 -

Zinc - $ 3241 / MT, up 14 pc

Lead - $1931 / MT, down 2 pc

Silver - $ 84 / Ounce, up 165 pc

A $ 100 / ton increment in Zinc prices inclines company’s annual EBITDA by 675 cr

A $ 100 / ton increment in Lead prices inclines company’s annual EBITDA by 125 cr

A $ 1 / ounce increment in Silver prices inclines company’s annual EBITDA by aprox 175 cr

As of today - Zinc, Lead and Silver prices are trading @ $ 3476, $ 1965 and $ 76

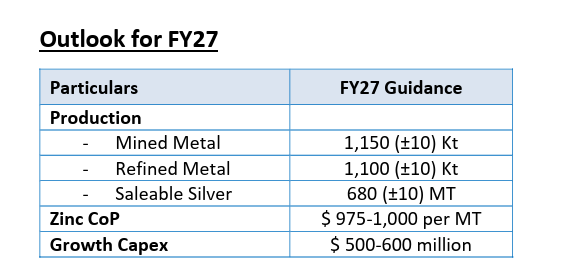

Guiding for 1150 KT of refined Zinc + Lead output for FY 27 ( vs 1114 KT in FY 26 )

Guiding for 680 Tons of refined Silver output for FY 27 ( vs 627 Tons in FY 26 )

Guiding for Zinc’s COP @ $ 975-1000 / Ton for FY 27 - looking at current geopolitical tensions + inflationary environment in general

Paid royalties worth aprox 6000 cr to Rajasthan Govt for FY 26

Hedging prices ( for aprox 10 pc of company’s output ) for Zinc and Silver for FY 27 stands @ $ 3225 / Ton and $ 59 / ounce

Theoretically - if Zinc prices fall below $ 2900-3000 / Ton and Silver remains above $ 60/ounce, it would be more profitable for the company to switch over to Lead + Silver production combo ( thereby increasing Silver production to above 700 tons )

Have declared an interim dividend of Rs 11 / share - resulting in a cash outgo of aprox 4000 cr

Royalties / Brand fee / Consultancy fee paid to Vedanta for FY 26 and FY 25 stood @ aprox 1300 and 1120 cr respectively

Should be able to start manufacturing Phosphoric acid by Q2. Should be able to commence making DAP by end of Q4 FY 27

Sales and EBITDA from Lead concentrate ( pre refined lead metal ) sales for Q4 were around 500 cr and 300 cr respectively

Once their 250 KT smelter @ Debari goes live ( towards the end of FY 28 ), their annual Silver output would also move towards 800 tons

Sulphuric acid is a significant by-product of zinc smelting/refining and Hindustan Zinc is actually one of India’s largest producers of sulphuric acid. Company typically produces 1.3-1.4 million tons of H2SO4 / yr. Their customers include - Coromandel Intl, Deepak Fertilizers, Paradeep Phosphates etc. This is a good position to be in - given the Sulphuric acid shortages caused by Iran war

Disc: holding, core investment position, not SEBI registered, posed only for educational purposes, not a buy/sell recommendation, biased