Good insights in article, multiple factors seem to converge to give tailwinds to category with 40% revenue and 50% profit contributions (BPC)

Market share gains

Volume growth triggers - no of wash increased, still 1/3rd of global averages

Premiumization of portfolio

New category extensions- conditioner, Serum, etc

Per Nomura HUL 75% product category has gained mkt share post corona - is it a well thought out customer acquisition phase strategy - with rewards to follow? Time will tell - been a massive underperformer in last year and half in line with most of upper quartile FMCG.

Some other interesting facts

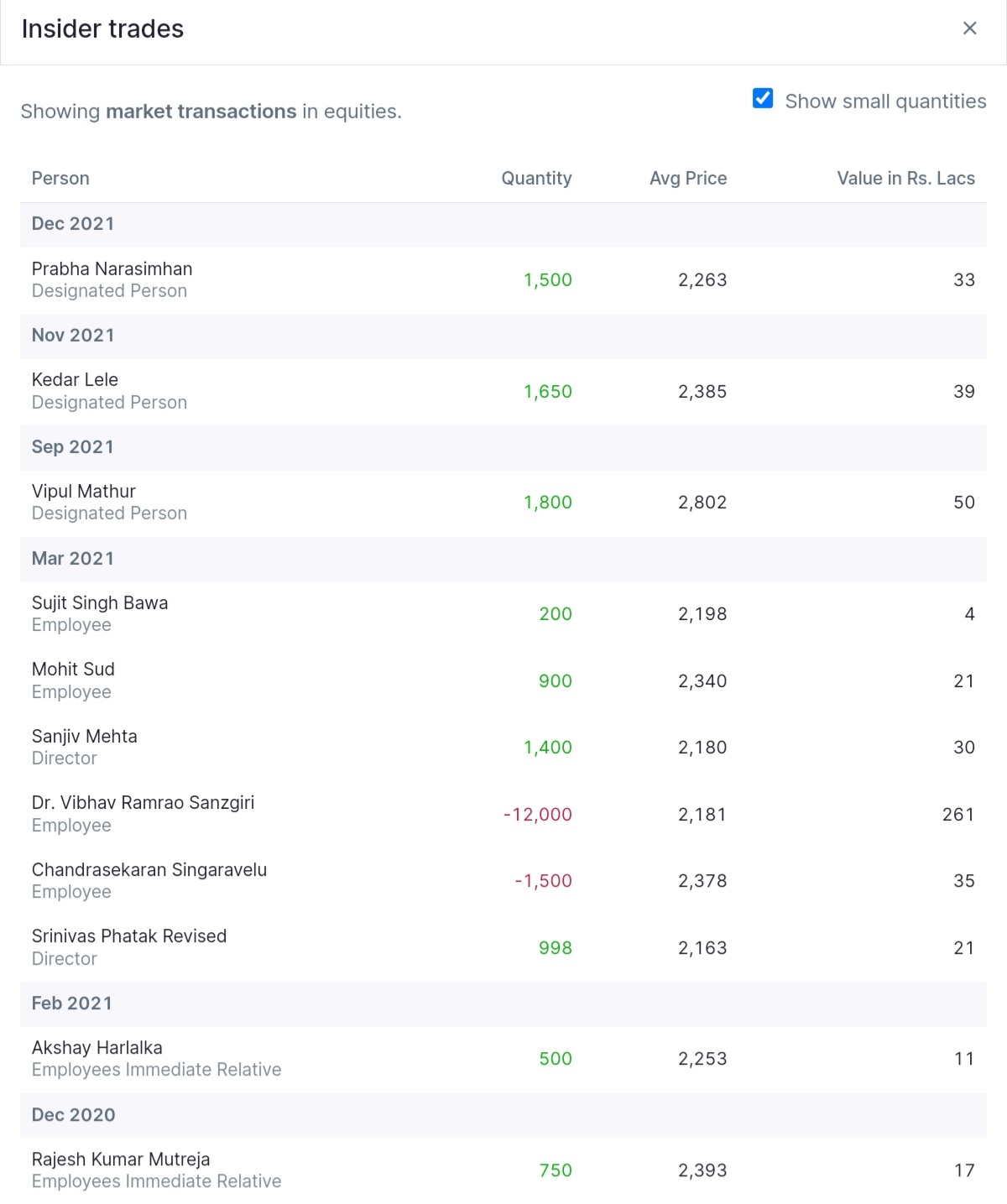

Insiders buying regularly includes Mr Mehta and Mr Lele

Besides strong FMCG characteristics, HUL IMO has been more of a margins expansion story than sales growth, thus rerating over last decade and major contribution to this feat is heavy lifting by BPC segment( 40% of sales and 50% of profits and margins above consol)

Used to be one of most sought after quality/defensive names pre corona/narrow phases of market. Margins headwinds once subside and Volume growth goes back to high single digit, may gain its MOJO back. At best a consistent and slow grower(15%+ div) given mammoth size and scale, over med to long term.

Very interesting point by @dd1474 on possibilities of rewarding shareholders using reserves over next few years, that’s the specialty of an experience lens which comes with longer term.

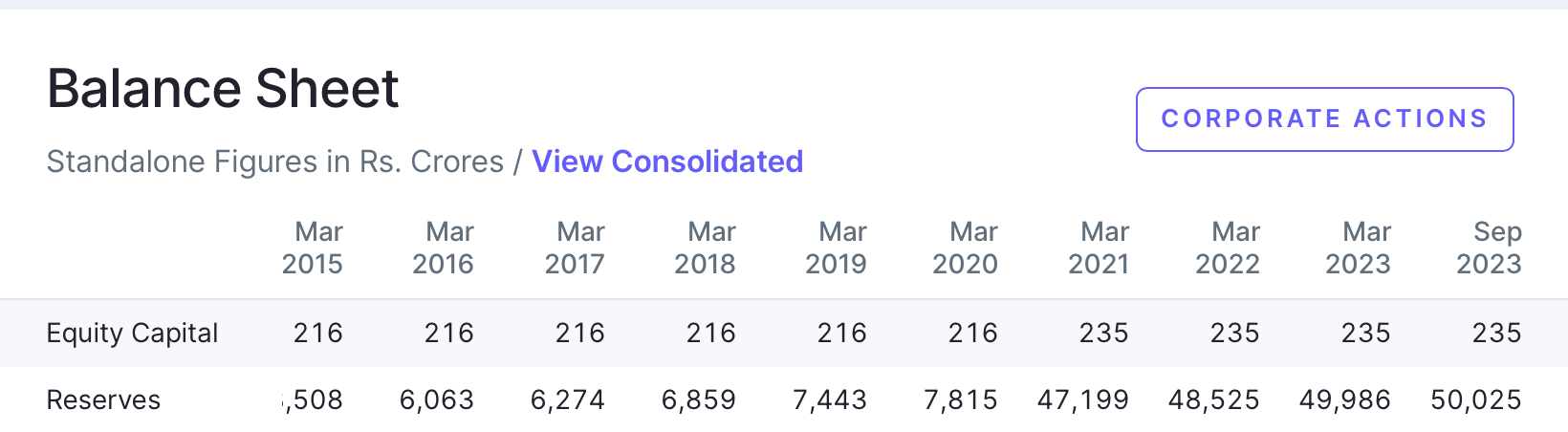

Reserve is a liability and can not be the source of dividend. One must look at the Asset side of the B/S to see if dividend beyond normal is possible or not.

66% of Total Assets consist of Goodwill and Other intangible assets. This will will pull the margins south. Other intangible assets needs to be amortized every quarter and Goodwill will be tested for impairment on yearly basis and may lead to write down as and when impaired.

What’s Likely?

With 235 Cr. shares, even to pay a dividend of INR 34, HUL needs 8000 Cr. cash. Seems possible considering current cash of 4500 Cr. and operating cash flow that will happen in H2FY22.

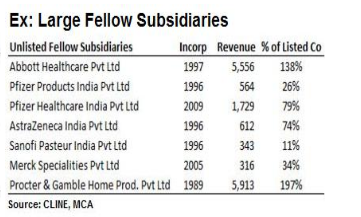

One of the few listed MNCs in India not having unlisted subsidiaries.

Even Nestle introduced pet food through unlisted subsidiary

The narrative seems to be that HUL stock price is going down due to inflation and fears of inflation. I think this is just a case of narrative following price. Weren’t FMCGs supposed to be a good bet (especially large ones like HUL) in inflationary scenario due to their ability to pass on costs

Thing to take care of. Go a bit slow since 50dma has recently gone below 200dma. Momentum is an important factor in the time period upto 1 year.

As you rightly mentioned, HUL looks good from a valuation standpoint. If at all HUL is able to acquire MDH which has a good presence in the spices market, it will be another shot in the arm to increase its market share further, though MDH is claiming this as a rumor.

I am new to investing and thus what I say should be taken with a huge huge grain of salt.

From what I have read and understood from articles and the most recent conference call of HUL is the following:

One of the main reasons for the drop in HUL price seems to be due to the slowdown in its rural markets, primarily lead by inflation.

Whilst the company posted a healthy Q3 result, as per the conference call 2/3rd of the growth was lead by value and 1/3rd by volume. In fact they also mention how the rural market saw a negative volume growth.

Inflation leaves consumer markets very uncertain as buyers try to determine when to consume. By this I mean, if rates were hiked very recently it could have two effects, namely either the consumer purchases the product immediately anticipating another price hike or delays the purchase till he himself gets a pay hike or the inflationary environment becomes more stable.

Overall to sum up the concern seems to be the fact that whilst HUL has been able to take multiple price increases, at some point the demand drops of dramatically in the rural markets leading to a reduction in the magnitude of growth for the company overall and the inflationary environment has left investors un sure about what exactly will happen. Thus I believe investors are re rating the stock anticipating a reduced growth rate or at least being un certain about the growth rate especially due to the rural markets.

However, in the same conference call the management also indicates that according to them rural demand will eventually bounce back and alongside that there is also a good amount of pent up demand that is also making its contributions to growth.

Being an investor in HUL, I look forward to the Q4 results and conference call as I hope to hear more about what investors and management both think of this continued inflation.

The bet is macro on HUL …primary question is for how much time hyper-inflation (crude flirting 100$ +) continues …during 2005-12 there was inflation pressure due to which fmcg companies took significant price hikes. The benefits of this price hike ensued during 2013-19 as FMCG companies enjoyed higher margin as cost of doing business eased (price benefit + cost savings). Now, how many quarters of underperformance is likely to ensue given the peak operating margin background that HUL is coming from. Logically; if profit margin expansion story has dried-up, so what is left-over?? …revenue growth?, that’s also likely to be impacted and is not likely to be much exciting! …

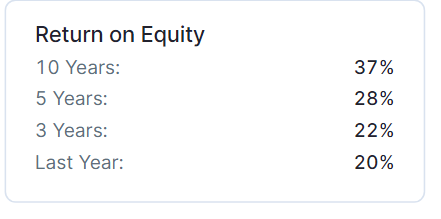

Post merger of GSK CH business into HUL, the equity on balance sheet shot up significantly. The denominator in RoE shot up in last 3 yrs hence RoE looks reduced

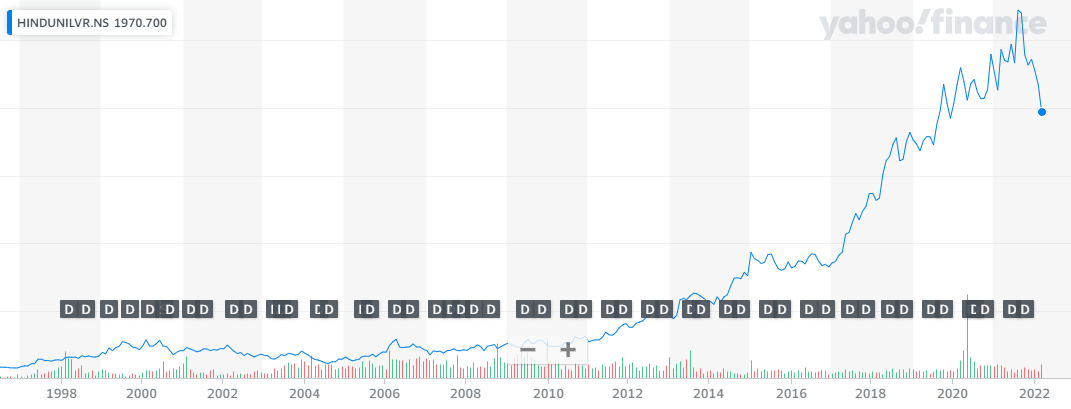

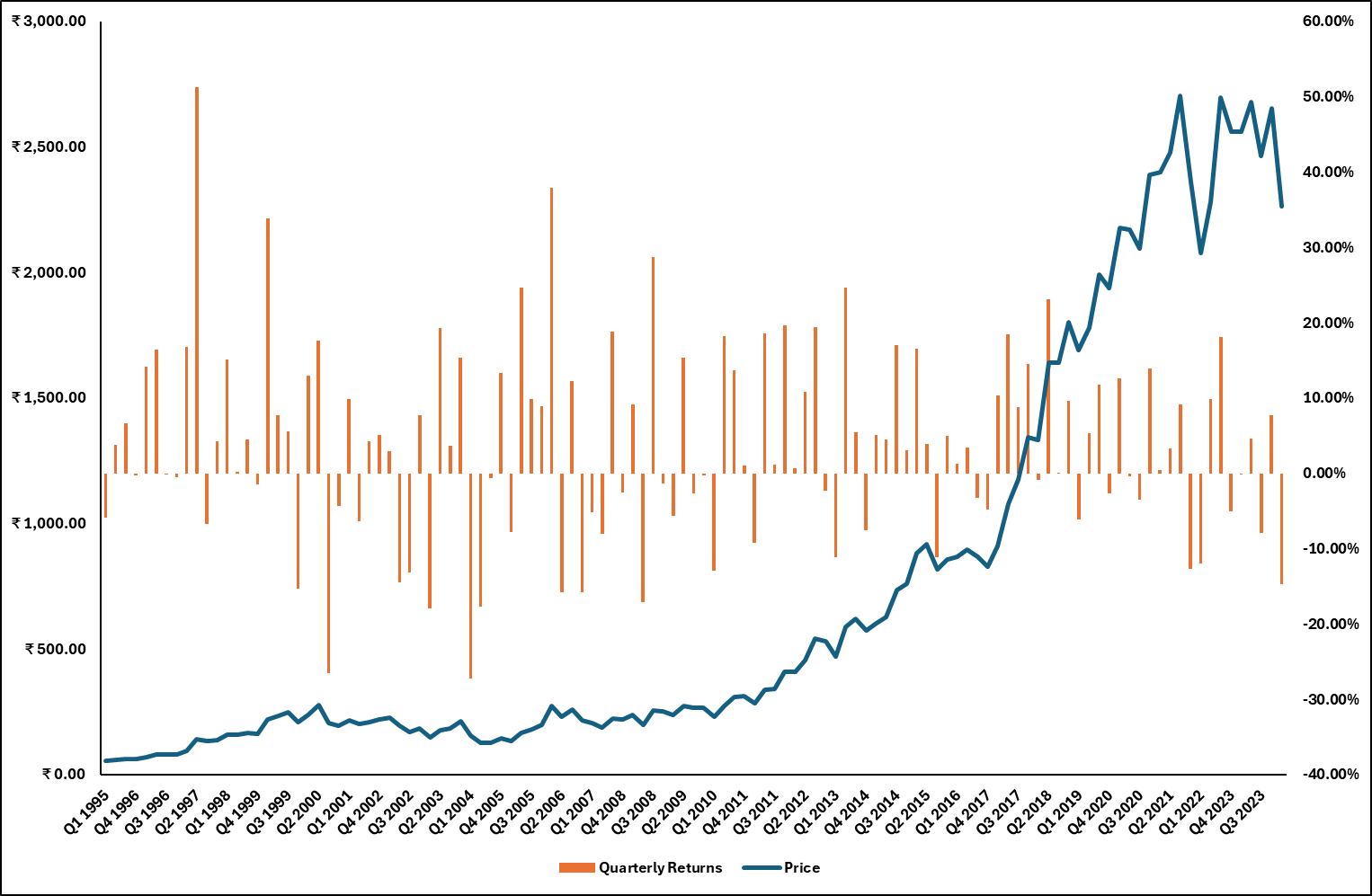

That’s because much of the future growth was already priced in and due to lack of fresh triggers the stock price maintained its sideways trajectory. I’ve seen some experts opining that FMCG companies getting 50-60 PEs were relics of the last decade and might not continue…remains to be seen.

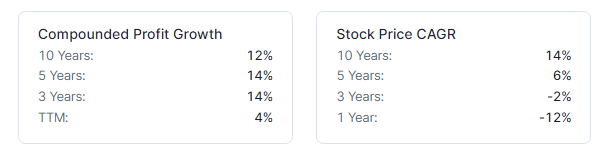

Nice post, I think your 10 year profit vs stock growth cagr explains it already. Profit cagr of 12% and a stock cagr of 14. For company like HUL where there is no significant gap to be filled, stock cagr will mirror profit cagr over the LONG TERM provided there is mo downside risk due to derating amd neither upside risk due to market seing any significant gap to be filled in coming years…

HUL has infact done great as a business with 12% cagr profit growth last decade…and stock has beautifully given 14% with much less relative risk returns and a decent dividend yield as well.

I think these experts have been saying this since decades…they might as well buy the moment any volume recovery hint even comes…

Even after what not this decade, many fmcg still beyond 50 plus PE.

If they start quoting at 25 PE or so, I would worry about country more than stocks…and if country is doing fine its time to sell everything else and buy these…

Personally I see HUL as fairly valued at these levels…any uptick in expected growth may trigger a rerating…

Disc. very small tracking position in hul. significant holding in other fmcg hence biased. Not a buy sell recommendation and post only for academic purposes. Not eligible for any advice