Expecting others to follow suit as well. If companies start claiming its 99.9% effective along with necessary legal formalities we’ll end up seeing people use them daily like we use toothpaste. Currently only big player is Listerine owned by J&J.

This mouthwash with CPC is made by P&G in USA. Cetylpyridinium Chloride (CPC) is a well-known, broad-spectrum antimicrobial agent used in over-the-counter mouthwash in USA.

(Crest® PRO-HEALTH™ Mouthwash, Procter & Gamble).

So if HUL brings a CPC mouth wash in India,

P& G india is also expected to bring it’s product from USA .

Now also , you can get Crest mouth wash in Amazon …but they will import and deliver to you…

Actual price in USA 3 to 4 USD for 150 ml …but if we import it we have to pay 20 USD import duties

HUL seems to be silently growing its Pureit brand. It lists it under the category “Life Essentials” and it has only this water purifier brand under this category. Interestingly this brand started as a very simple water purifier catering to the then mass market and very basic filtering but now I observe it right at the top end of the spectrum with intricate ROs and presence in all types of water purification. The product looks like from a top notch consumer durable company and competes in all leading stores and ecommerce site with top players in the category.

Point is - 1. Does Unilever operate in any consumer durable area worldwide other than water purifiers?

2. How and Why did HUL venture into consumer durable area?

3. And How well is it faring in terms of growth, investments and margins?

I am sure it is currently not moving any needle, but seing the quality and depth of their water purifier products, it shows their seriousness in consumer durable area - I fail to understand why such seriousness in a non core area and what maybe the strategy around it, if any…

In fact the successful foray of HUL in durables category made me very much bullish on HUL’s long term chances. That they can become successful in new territories as well.

Afternoon.

I was reading HUL on screener and going thru ratios.

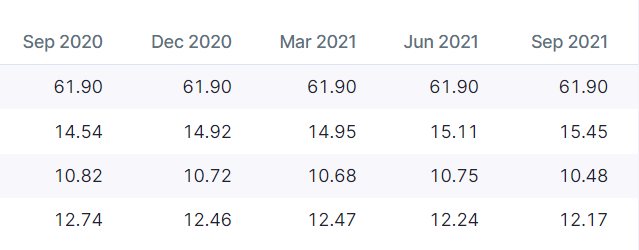

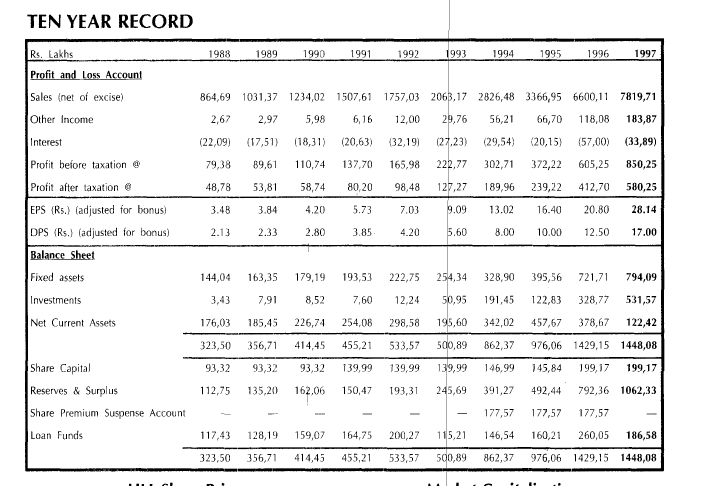

There is “ROCE” and it is 39%, way too low compare to past 10 years where it is always stayed around 3 digit.

Can anyone please explain why such a deep fall?

HUL management has tendency to operate with lowest capital employed possible. They have in past, taken approval to utilise accumulated reserves for past years to be approved as dividend and optimise networth (hence capital employed). Since GSK accumulated reserve got added in networth, the networth got bloated. I would expect same to be distributed to shareholders as dividend over 2-4 years period. My understanding may be wrong.

Discl: Hold nominal position in the company for last 8 years. No change in last 1 month

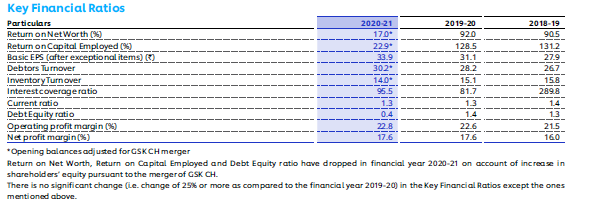

Return on Net Worth, Return on Capital Employed and Debt Equity ratio have dropped in financial year 2020-21 on account of increase in shareholders’ equity pursuant to the merger of GSK CH.