This is huge positive. One negative overhang has been capital allocation issues. This removes that.

1 Like

we should also consider valuation increase of the hotel assets which should be in the range of 3-4% but not factored in the financials as they are on the book value …

Increase in value of hotel assets can be useful only when they are intending to sell some in the future but that is not the case.It is the return that they generate on assets which will be the value driver and they have done it badly in that aspect. From my understanding, hotel business is capital misallocation and might be one of the factors for the stock under performance.

That’s the reason you are able to increase the rates on annual basis. If there capex cycle is over then down the line in 3-4 years, there will be significant cash flow from hotel business without putting any additional capex. This is similar to RJio strategy who builds the Telco infrastructure for first 5 year now it’s become permanent cash cow business for them…

Good point to note down. But even if their capex cycle is over and hotel business becoming a permanent cash cow, will it be able to generate roce of atleast 10% on average ? The other listed pure play hotel businesses are still unable to generate good return on capital.

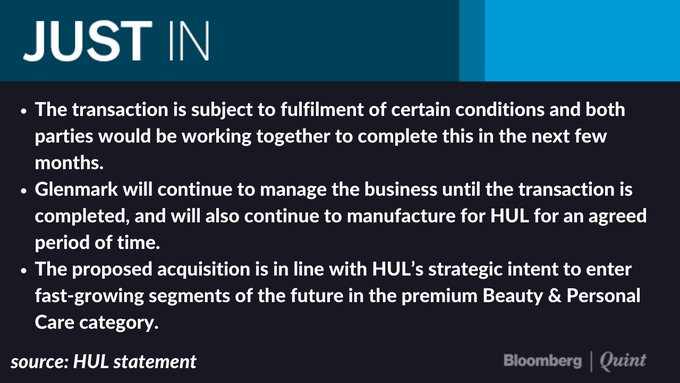

The deal includes acquisition of intellectual property rights, including trademarks, design and know-how related to the VWash brand. The consideration has been split into two parts involving an upfront cash payment upon closing of the deal and a deferred consideration over the next three years,… Glenmark will continue to manage the business until the transaction is completed, and will also continue to manufacture for HUL for an agreed period of time," HUL said in a press release.

3 Likes

“HUL at present has a 4.4 percent weightage in the Nifty and this will increase to 5.5 percent.”

2 Likes

Hi Ranvir

Was reading this very old post of yours and looks like an excellent strategy over last decade. Wanted to know how did it fair for you and what was your practical experience in this since your post from 2012.

Thanks

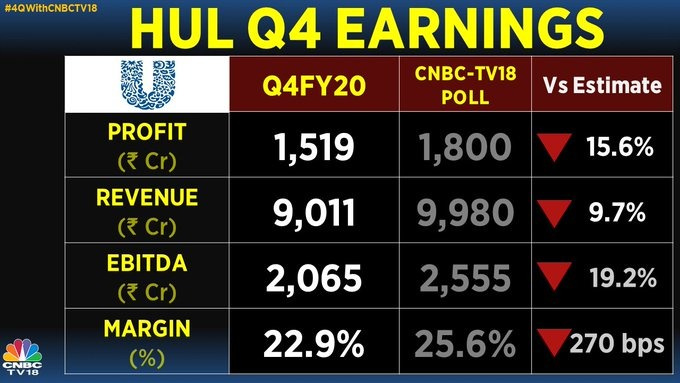

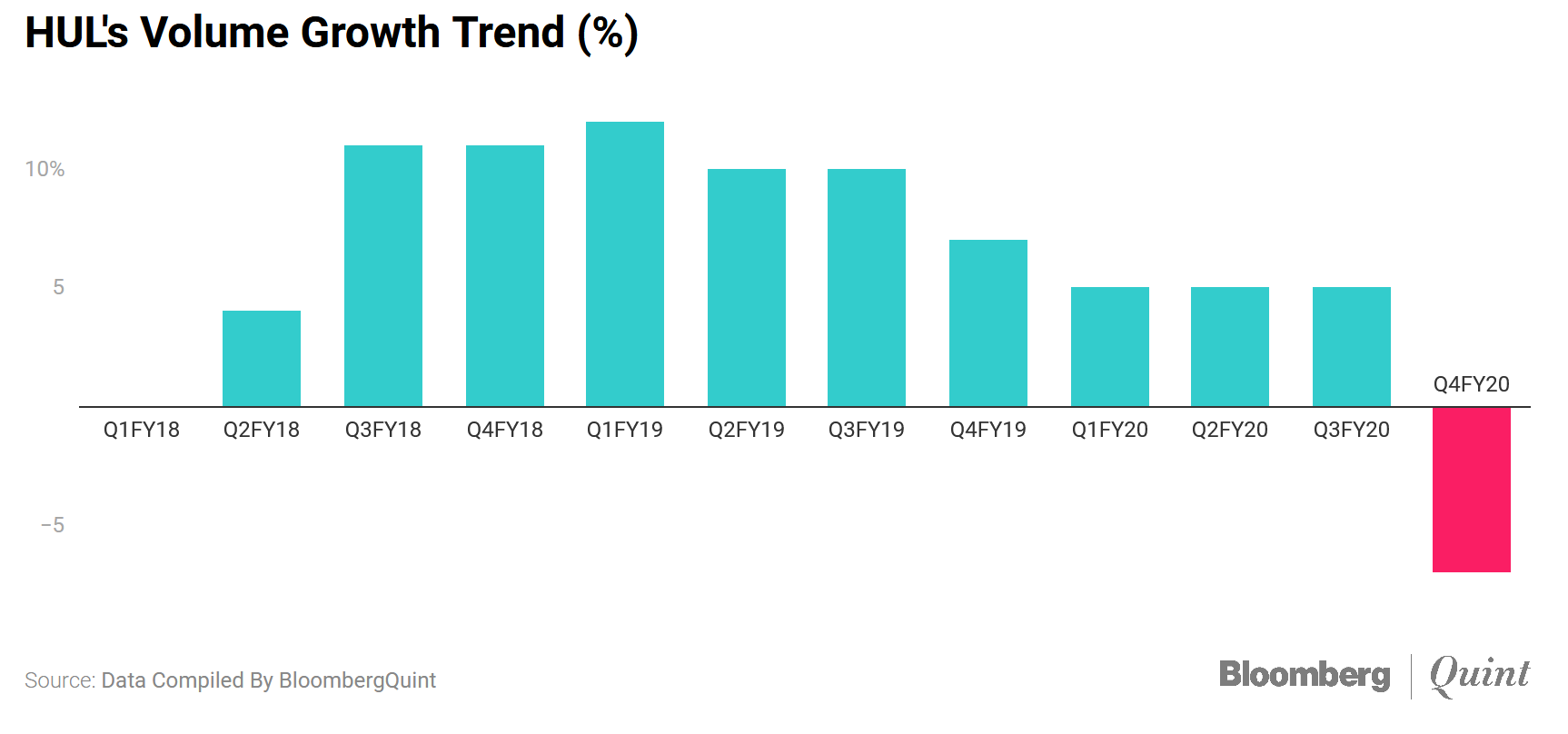

I am not comparing with the CNBC poll estimates,I have just shared the screenshot,I have also shared the volume growth trend from the other screenshot over several quarters.

I have also shared the link to the investor presentation and the management concall which goes into much greater detail.

2 Likes

HUL Q4 FY20 Results review by ICICI Direct & HDFC Securities.

2 Likes

Yeah, it gave me a nice chance to quit, after 20 years. Good line of thought!

2 Likes

Dear all, it would be best if you share your queries regarding ITC in the dedicated thread for ITC.

https://forum.valuepickr.com/t/itc-will-s-gold-flake-assist-ashirwad-to-win-bingo/

Please use this thread for HUL related discussions only.

PS: I am renaming this thread to remove reference to ITC so that no further confusions arise. Moderators are welcome to undo this if deemed fit.

6 Likes

I have tweeted few days back regarding Valuations of HUL…

HUL undoubtedly Great Co but price is not…

Business Growth is not as big as Valuations Expansion…

Views are welcome

1 Like

IMO HUL may post around 20-30% contraction in Volume Growth for FY 20-21. (Bull case Scenario)

Mr Market giving Premium Valuations against Historical Growth Phase.

Finally it happens,GSK is selling their shareholding tomorrow via a block deal.

After this HUL’s weightage in the Nifty will increase to 5.5% from 4.4%.

“We have a hand on consumers’ pulse and follow their consumption behaviour,” said Mehta. The government can leverage this know-how to push the use of products including soaps, sanitisers, and nutritional food that can help fight Covid-19.

For instance, HUL can educate people in slum areas like Mumbai’s Dharavi—a hot spot where positive Covid-19 cases have touched 962—about the importance of eating nutritious food and following hygiene, suggested Mehta.