I can see itc is aggressively promoting their products in television channels . In kerala in between popular tv shows I can see ads of ashirvaad ,bingo, sunfeast loop, vivel, ashirvad salt back to back. Itc is top third advertiser after hul and reckitt.

1 Like

2 Likes

The author has mentioned one of the reason for price of share going down is due to high float. Can some one explain ?

Growth vs Exit Multiple Sensitivity Table from current valuations. Assumptions are mentioned in the thread.

Just change the CMP cell marked in yellow. Cell no. C7. It should give you the expected return from your desired entry price.

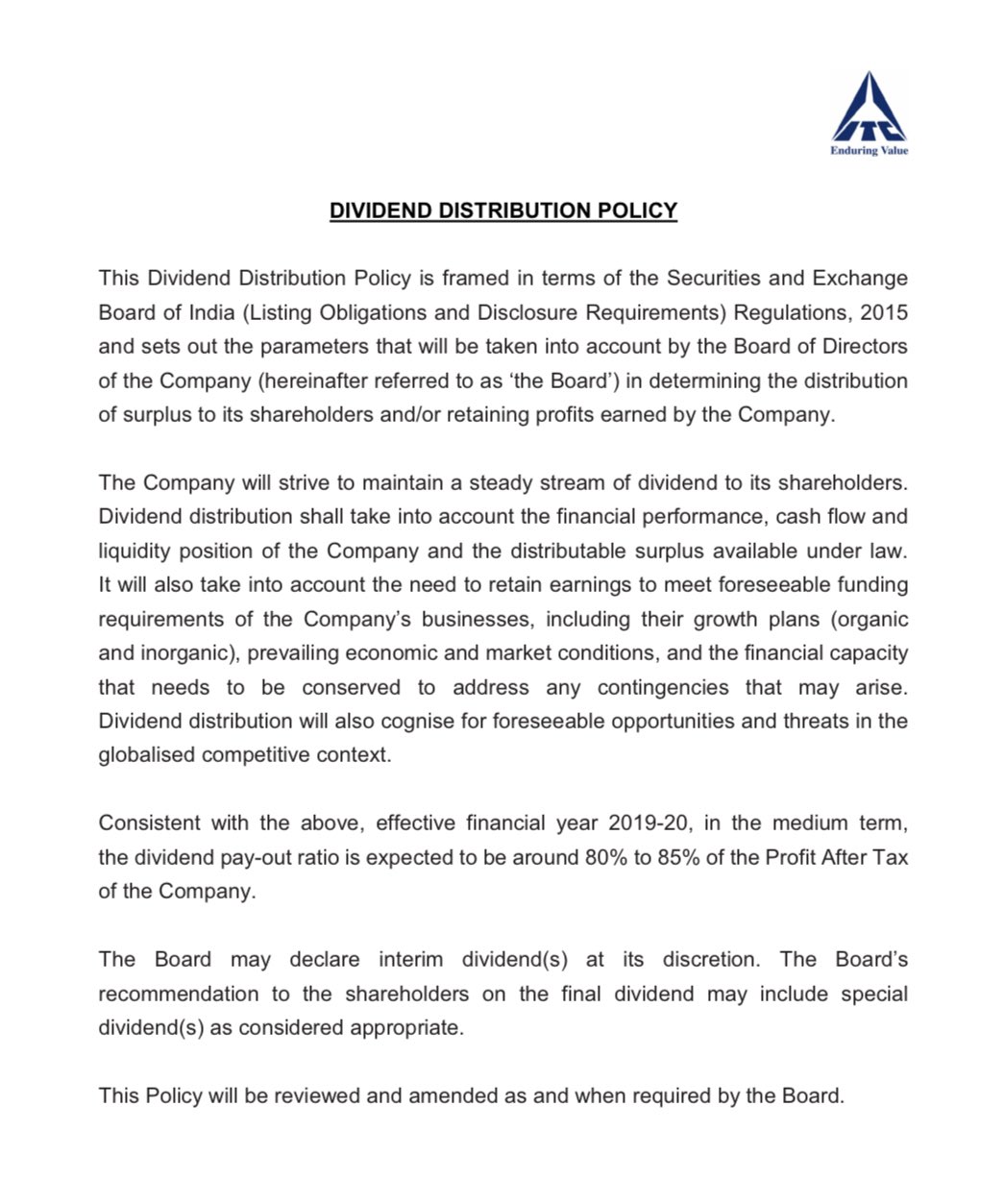

PS: Have updated the model for new dividend payout ratio (DPR), previous DPR was 55.98% have revised it to 80% as per new guidelines.

1 Like

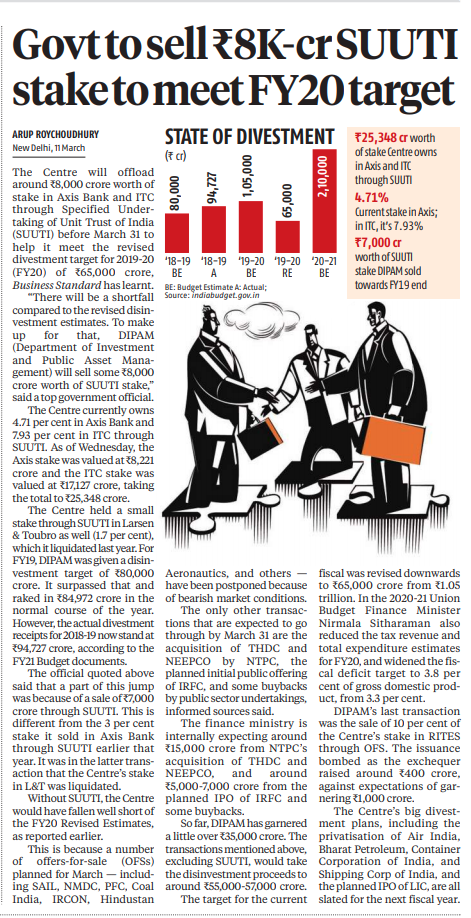

I assume that he means that since there are no promoters for ITC, funds which were holding the shares and now conforming to ESG are selling, also selling due to frequent ESOP issues in the past, there are more shares available in the market hence price is going down. Plus overhang of SUUTI stake sale. But he fails to mention that BAT holds around 30% of the shares and now ESOPs have been stopped.

1 Like

So much for Efficient Market Hypothesis. Government is selling at the worst time for ITC stock in the last 5 years.

Great times ahead if someone wants to invest a fresh.

ITC with a 5% dividend yield(with further price falling), the youngest world demographics in India and a compelling FMCG arm makes for a juicy long term bet.

3 Likes

What can happen if they announce buy back at this prices ?

Wouldn’t it act as a positive trigger and more rewarding to shareholders too

That’s what we believe as an outsider but Management believe that’s the future of the company.

Unfortunately management hasn’t clearly shared their fmcg strategy with reasonable details so

I think apart from fmcg contribution to bottom line use of cash to buy back shares at these levels can provide some positivity and trigger for price action in near term.

If management feels that current market price are significant lower vs fair value then they should go for buy back instead of putting capex into some new venture…

1 Like

Buybacks are ruled out as ITC does not want BAT to increase its stake in ITC …

Hence they have continuously diluted BAT holding through ESOP …

Hi, ITC Ltd hotel business is generating return on capital employed around 4% for last ten years. The capital employed for the hotel business for the FY 18-19 is 6665 crores. Could some experts tell me why ITC has been putting cash into this low return business ? Isn’t this capital mis allocation ? Thank you

It surely is not just hotels but for also other businesses too

That’s the reason market has lost their patience and giving such valuation to entire company .

Let’s hope the new management/ charman gets the message and do something about it

Nope. Agri and paperboard business doing well and supporting FMCG business too. The return on capital for FMCG - others might seem low currently but return on capital employed, margins, revenues, profits improved very much. The only issue is their hotel business is doing bad.

Why ITC invest in Real estate assets like Hotels , Corporate / Division / Branch Offices , employee housing , Factories etc unlike other FMCG

Imagine you are cash Rich … and you pay 38% - 40% tax + 20% tax on dividends

so effective money you can give out to your share holder out of Rs 100 profit = 1000.60.8 = 48

So effective ROCE calculation has to be done on Rs 48 and not on Rs 100

Avg ROCE for any hotel Co is 8% at portfolio level - with Mature properties earning in high double digits and new hotels earning in low single digit –

ITC has lot of new hotels added in last 5 / 6 years so many are still at infant stage in terms of ROCE …

++ thru depreciation you can writedown the property value over period of time and claim tax rebates

2 Likes

First things first, I agree with you that dividend distribution is tax inefficient. But even roce of 8% is very low and not justified to deploy cash into this business. For your reference, the avg roce of ITC other business is 75% (excluding FMCG as building brands takes time) and now you can understand how bad are their capital allocation skills towards hotels.

Secondly, you are talking about depreciation, tax rebates, so have they built low return hotels just to claim tax benefits ?

Lastly, 8% of op cash flow on average being spent on hotels every year which is 20% of cash flow retained as it pays 60% dividends.

This would mean a jump of over 40% in dividends, taking the dividend yield to around 6% at CMP.

Also, does this means no big capex going forward?If true, this could further boost the earnings in the coming quarters

3 Likes

My reply lies in New Dividend policy of ITC : 85 % payout …

With Reduction in corporate tax and removal of DDT … post tax IRR thresold for new investment will change

1 Like