Established by Mr. Madhusudan Bagla, a first generation entrepreneur, pioneered self-adhesive water based Carton Sealing Tape manufacturing in India when he set up Hindustan Adhesives Limited in 1988. Currently his son, Nakul Bagla(CFO) is the driving force behind the company

Company operate 3 plants in UP, Uttarakhand and Gujarat respectively and employs around 300 employees

Promoter & family owns around 70% stake in the company

Company is manufacturer of Acrylic Packaging Tapes which is suitable for all type of Carton Sealing applications. The product range includes various tapes like heavy-duty tape, tear tape, low noise tape, printed tape, coloured tapes, jumbo tapes, freezer tapes etc.

It also manufactures Polyolefin Shrink Film which is fully recyclable way of packing FMCG goods

It is catering big brands like Unilever, PepsiCo, Coca Cola, P&G, Reckitt Benckiser, Cadbury, Nestle, ITC, Amway, Colgate, Dabur etc. since a decade

Co. has over 500 total customers

Industry Scenario

BOPP Tape market size in India is estimated around Rs.100 crore/Month. This market is divided primarily into two parts – Organized sector and unorganized sector.

The organized sector contributes around 40% of the demand while the remaining demand is fulfilled by organized sector.

Growth Visibility

Company operated via 2 legacy manufacturing units in U.P and Uttarakhand each with combined capacity of 62 Million square meters and catered to the domestic market

In 2017 co. planned on expanding its adhesive tapes manufacturing capacity substantially by adding 216 Million square meter plant, taking total capacity to 278 Million square meter at total cost of 35 Crores

By April’18 the new plant(imported from Italy) was commissioned near Special Economic Zone (SEZ), Mundra (Gujarat). It is an Export Oriented Unit (EOU) and management aims to cater the export market via it

The plant was set up near port to mainly cater export markets as there was demand visibility and higher volume offtake in export business compared to smaller order size in domestic markets which it caters through older plants

Mundra plant is also vertically integrated as it manufactures Adhesive solution which gives stickiness to the tapes and corrugated boxes wherein the finished products are packed and shipped

Co. also set up one marketing unit in the US with branches in various parts of Europe under the name Bagla Films LLC for catering to foreign units of its Indian customers and subsequently new clients in foreign geographies

Co’s Realizations are around Rs.13-14/ square meter. At optimum utilization (85%), Co. has the potential to achieve top-line of around 300 Crore of topline without incremental investment vs the FY19 Sales of 140 Crores & 75 Crores in FY18

Financials:

Annual revenue was around 75 Crores until FY18 which was constituted- 50 Cr sales of adhesive tapes and 25 Crores sales from POF shrink films FY19 Could see clear growth in numbers wherein the top-line increased to 140 Crores due to commencement of the Mundra plant vs 75 Crores YoY

FY19 export sales stand at 77 crores vs 10 crores in FY18. Exports also fetch export incentive of around 3 crores in FY19

Currently debt stands at 53 Crores. The overall gearing remained stable to 1.29x as on March 31, 2019 as compared with 1.30x as on March 31, 2018

The operating cycle of the company improved to 59 days in FY19 vs 100 days.

The improvement in operating cycle is on account of improvement in collection period to 50 days in FY19 from 72 days in FY18 due to increase in export revenue. The improved collection period and more export demand led to improved inventory holding period to 58 days in FY19

Despite almost double top-line YoY, the OPM largely suffered mainly due to commencement of new plant at Mundra, Gujarat and FY19 being the first year of operations.

Volatility in EBITDA % suggests that company’s margins depends on the volatility in the RM prices- crude derived which needs to be monitored

Cumulatively past 10 year EBITDA is 100 Crores vs cumulative adjusted cashflows of 76 Crores which signifies that the reported profits is converted into cash and it is not only accrual based earnings

Weakness

Co. operates under single brand- Bagla group wherein they also operate their private entity- Bagla Polifilms Ltd which is involved in POFF Shrink film manufacturing.

However, their product profile is different from Hindustan Adhesives Ltd because proportion of POFF shrink film to top-line is around 18%

Raw-material susceptibility: As the core raw material are crude derive, any fluctuations in the crude affects the realizations of the co and impacts the profitability and EBITDA %

Valuations

Currently the stock is trading at lucrative forward valuations of 2.8x EV/EBITDA

If co. successfully ramps up the production from Mundra plant at optimum utilization, it could generate EBITDA of 30 Crores (300 Crores Topline * 10% OPM) whereas current market-cap is only 35 Crores

Sources: AGM, Website, Credit Reports.

Disclosure: Invested but no transaction since past 3 months

Going through last few years of financials and I see some issues with the way management is running the business. On a business level, company is doing fine but the gains are accruing only to management and not to shareholders. Some of the points, I noticed

Company has not been able to reduce its debts over long term. Estimated Interest paid is coming up pretty high. Company has been refinancing its loans very frequently, switching from bank 1 to bank 2 almost every year. Also they seem to have high requirement of vehicles as almost always they have some or other auto loans.

Many times, loan are being sourced from unknown sources by promoters. High interest rates might signify that promoters are raising loan from their relatives or friends and hence don’t want to clear off debt, but siphon off money from company.

Management and its relatives are withdrawing exorbitant amount of money using Salary, Commission, Rent Paid and several other ways.

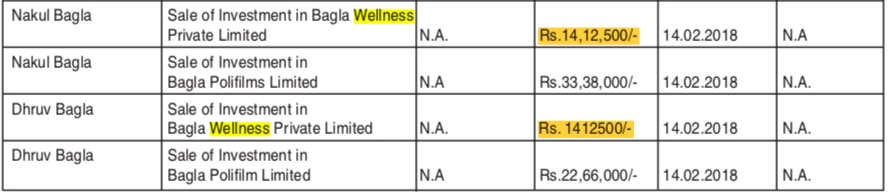

Company had established a subsidiary by name “Bagla Wellness Private Limited” in 2015 with investment of Rs 34.8 Lakh, which was closed in 2018. I don’t see any financial gains from this subsidiary to company after closing down, but KMP and Relatives got a nice 1 Cr gain from Sale of Investment. This was the reason why in year 2018, they received 2.8 Cr from company.

Company has paid dividend only once in last 10 years. While KMP has got a good part of company’s profit. Minority investors did not get much.

Company might get a good benefit out of export opportunity, but i highly doubt (given the past) that management would share such benefits with minority shareholders.

Thank you for raising counter points. This way, we can study a co. in an unbiased manner.

Following are some replies to points raised by you:

Co. used only Allahabad Bank & IDBI Bank since a decade for majority of the working capital need. Other bank credit used are barely in few lakhs.

In 2018, co. raised term loan from Allhabad bank and in FY19, it refinanced it from SBI. It’s very common for firms to refinance loans at cheaper rate. As per MCA documents I have, current rate of SBI term loan is 10.45% which is quite lucrative, given the size of the Co.

Debt would obviously go up as they are funding new Capex, and so would the interest outgo.

Over the years the interest is paid mostly only on working capital loans from IDBI & Allhabad bank. I went through the RP transactions over past AR’s and I am attaching actual interest paid by management:

I agree with the fact that the salary drawn is increasing is at a faster pace and doesn’t justify from the financials reflected until now. However, you seem to have also included rent, hire purchase, deposits etc. as well which is not necessarily detrimental to shareholders.

As per my limited understanding, Rent should not be considered as form of payment. It is backed by some legal tangible agreement and not necessarily bad for shareholders unless the rent charge is abnormally high than market rate

I agree - a packaging co. investing into a gym subsidiary always remain mystery.

Since 2016 the Bagla Wellness became subsidiary and was holding 1,62,000 shares- invested 64 Lacs. Per share value- Rs. 39.5

It decided to de-classify it as subsidiary in 2018 wherein it retained 49,000 shares and book value of 18 Lacs (Rs.36.7/share) and sold off 1,13,000 shares to the promoter family at 28,50,000 (Rs.25/share)

So, loss due to subsidiary is actually- 1,13,000 shares * Rs. 15 loss per share= 17 Lac and not 1 crore as stated by you. If I am missing something, please point it out.

Promoters also own another co. called Bagla Polifilms Ltd. which is unlisted. If they wanted, they could very well do the expansion in that entity. Why would they do it in listed company unless they plan to grow the Co.?

My concern about the company resolves around the line that why did they not try to reduce the debt during in past (before this recent capex)? when interest rate seems to be high >20% for most of the year between 2010-2017. I think they should have focused on debt reduction, during good times (OPM > 10% between 2013-17). If they could re-financing loan at cheaper rate, that is fine, but 20% rate does not seem cheaper to me.

Even taking your salary and commission numbers as percentage to PAT for that year. It comes to

Year - % of PAT,

2012 - 34%

2013 - 31%

2014 - 22%

2015 - 45%

2016 - 56%

2017 - 32%

2018 - 53%

So, even though PAT does not grow, but management keeps rewarding itself aggressively. At least percentage wise it looks to me on very high side. Promoter owns 68% of business, rather than behaving like owner, but they are just taking cash out by salary and commissions.

Don’t you think this is siphoning off the money? Company acquired shares at Rs 36 per share and sold to promoter family at Rs 25 per share. Think in this line, what minority shareholder (company) had gained out of this side deal? Wasn’t any opportunity cost of 64L of invested amount? I think in this case, company invested in this extra business, grew it and then was sold to promoter family. Regarding gain to KMP, I just summed up the “Sale of Investments” from related party transactions from 2018 AR. I do not want to do exact maths of loss in this case, because they can morph transactions in the way they want.

I have no clue why they might be doing expansion here in this company rather than Bagla Polyflims.

Domestic tape market is 4,000 Cr annually. The market is growing at 5% and our market share is between 2-3%

Margins are likely to increase going forward because of economies of scale

Export benefits: Govt plans to change export benefits scheme but co. is expecting to continue getting 3% export subsidy

Doing new CAPEX which will start during the second half of this year and over 12 months period, expecting 100 Cr of more sales. Even without new capacity, Sales are expected to increase by 50 Crores from existing capacity

Old plants at U.P and Utrakhand are operating at 70% utilisations and plan to manufacture value-added products there which are import substitution

New product: Co is developing many sustainable types of tape. Developed 50-micron packaging film

25% Income tax rate currently

Long term loans interest rate is 10% and the short term rate is 5%. Lower rate because short term loans are pertaining to packing credits and foreign currency loans

1st unit was 50 Mn sq mt. 1st phase of Mundra was the addition of 250 Mn sq mt. 2nd phase of Mundra will be another 260 Mn sq mt. Hence, total capacity effectively becoming 10x after completion of the new CAPEX

Dividend policy: currently using internal accruals for expansion so no immediate plans

Ashav,

Are you still following this company?

Any idea on the reason for their selling the bopp shrink film business to bagla polifim for mere 2.45cr when the topline contribution was 18.7 cr ?

Also, any idea on their capacity utilisation and expansion plans ?

Thanks