Agreed… but it was evident that something like this was likely when they announced special dividend on 3rd Jan

Promoter are ultra greedy

Why announce huge dividend and pay high taxes…

Anyway we all need to be more vigilant…

3 Likes

CEO has clarified in the ZEE business interview today. ~7200 Cr cash coming in after-tax. 4000 Cr will come to foreign operations which will never be repatriated to India as it is tax-inefficient. So Indian investors will never see this cash. This can fund some global acquisitions, which can later add to consolidated earnings. Of the remaining 3200 Cr which has come to India, wait for the results. Once the net worth is boosted he will mostly go for a buyback say up to 25% of the net worth as per guidelines. So overall, expect a maximum distribution of only ~1500 Cr including the 300 Cr distribution announced. The rest of the cash can be valued at a discount or in the worst-case scenario valued at zero.

2 Likes

Gone through the entire thread since 2015 and observed that the most part of the discussion is concentrated on reasons to find out why the share is trading at such low valuation … I hope now we have have got the answer  …Hats off to market

…Hats off to market  … The market gives valutaion to stock it deserves…

… The market gives valutaion to stock it deserves…

Discolusre not invested but tracking for learning experience…

6 Likes

The amount has further dwindled due o expensive lawyers and i-bankers

2 Likes

The CEO is talking about 1000’s of crores like it is some loose change. Obviously not going from his pocket…

1000 cr accounting adjustment

1500 cr lawyers, investment bank fees etc

1000 cr capital gains

Getting more disappointed with all these calculations and effort to justify the payout…

Nikhil

3 Likes

It’s a broad daylight robbery in the street in front of impotent SEBI and ED.Minority share holders should not live in the world of dreams and thinking sweet words like “value unlocking”. Promoters are involved in many scams starting from Bofors arms deal, tax evasion, human trafficking, and residency fraud and many more unknown scams(source: Prakash Hinduja Wikipedia)*. What the regulators are doing? may be they are the hand in glove. Company is listed in india still they intentionally don’t want to bring all the money here. No good company will sell the profitable business and invest that money in promoter group, mf, debt. We are invested in IT company not a finance company.

If the regulators really care about minority share holders they must first ban ICD’s and loans to promoters. Also they should make a law to return excess cash to share holders by paying legitimate tax if companies don’t want to invest in their core business.

Retailers must never invest in such chor companies.Watch Nigel D Souza grilling Partha

2 Likes

On a lighter node there is already a law which does not forces us to invest in such company… somewhere it is our greediness which prompts us to invest in such companies and in that case we should also be ready for its consequences … we also know how SEBI works…

1 Like

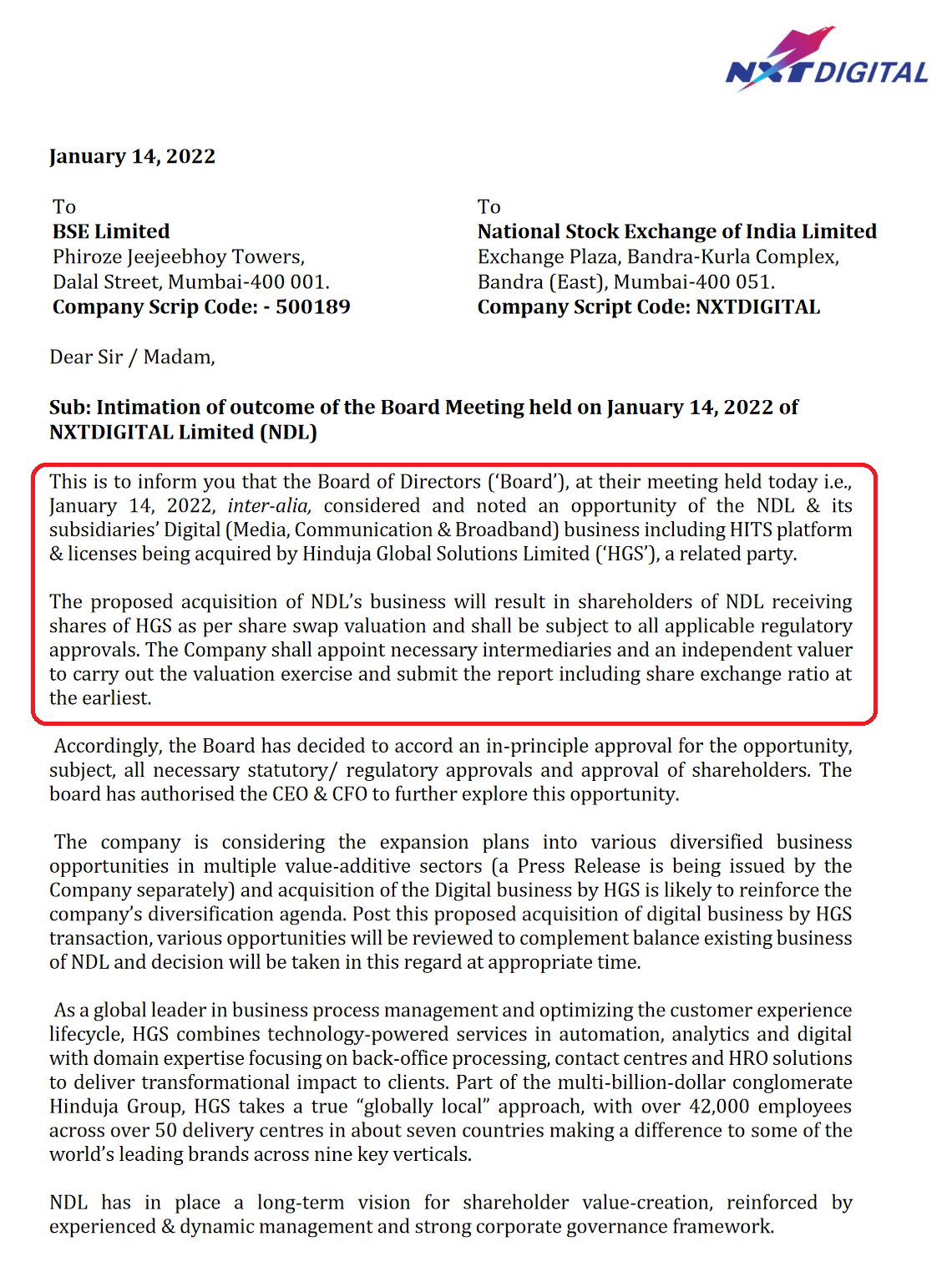

Board Meeting scheduled for 14th Jan 22 to consider terms of the proposed Buyback

Guys please go through rules and regulations wrt buy backs

Ie quantum that company is eligible of doing

Promoters with this track record shall not be trusted. Please fully understand the quantum of buyback.

Don’t forget about 150 dividend

1 Like

The wording of today’s announcement seems little different to TCS buyback announcement or Ajanta pharma (go through them)

Based on my understanding, HGS can do maximum 10% of Paid share capital + free reserves (if buyback is through board approval option) or 25% of PSC + FR(shareholders Special resolution is required) As on 31st March 2021 (about 1800 cr is psc+ free reserves)

The resolution which enables them to give more loans to the promoter entity is a special resolution and requires 75% of votes in favour to clear. Since promoter shareholding is high it will get cleared, but it will be interesting to see the ratio of votes for and against excluding the promoter.

1 Like

HGS wanted to wait till the net worth is shored up after the 4th quarter results before taking steps for the buyback. But the media and negative press is probably forcing their hands. I think they may just give an idea of the amount they plan to distribute through buyback, which will be done only after the 4th quarter results.

2 Likes

Why send for buyback. I think the bonus will b earlier & allow us chance to get arbitrage.

1000 crore allocated for buy back after March 2022. Buyback amount seems good. However buying another Hinduja company and its valuation has to be seen

I think the merger process by the issue of shares will help promoters in tax savings in buybacks. Not sure. But I don’t see any strategic angle here.

If any CA/tax expert can comment it will help. Also not sure if the announced buyback will be affected.

1 Like

While I know i am being condescending… but wil disagree with you… 2015 stock was roughly 500 now 3000+. And still market was efficient?

As a value investor, it is hard to ignore this stock for further inspection. It’s hard to find an IT services company trading at 60% of its liquid assets i.e. Getting the company for free plus north of 2000 Cr in cash. And as a value investor, it’s important to distinguish value traps from value stocks. I guess the low price of this company is a culmination of multiple factors:

-

Anxiety over cash utilization

HGS received close to 6500 Crores from the sale of their Healthcare Business. Even though the sale has removed all debt and given them ample cash more than the market cap of the whole firm, it is now left with weaker businesses. Healthcare was the major vertical and higher-margin business. On the positive side, they were able to sell it at 3 times the revenue which is I believe good deal-making.The company has approved a 975 crore buyback which would be done after the merger is completed with NXTDigital. They have already done a small acquisition namely Diversify Offshore in Australia but their revenues will not make much of a dent in the income statement. They certainly need to make some bigger acquisitions.

The management has stated in the con calls multiple times that most of the cash will be used for acquisitions in their bid to become a technology company. It will not be given back to shareholders in form of buybacks or dividends. Hence, the quality of acquisitions is extremely important here.

On top of that, there are always corporate governance anxieties over cash which will bring pessimism among investors hence low valuations. It is always in the back of the mind that cash from the sale of the profitable business might be routed to provide aid to ailing promoter groups or worse, siphoned to offshore accounts like in the case of LEEL, Cox and Kings among others. I consider the second scenario as unlikely even though one should not be naïve enough to completely discount its possibility. The first scenario is more likely as north of 1100 cr is already given as a loan to promoter entities. And I guess this is a real concern that should be addressed and it will definitely be a red flag if this trend continues upwards.

-

Low NPM retained Business

The healthcare vertical brought in most of the profits and had much higher margins. Selling that off had many investors in a jizzy. In con calls when asked about improving margins, management said that they intend to reduce the Real estate footprint at first. For that, they are closely watching the trends to WFH right now. As most of their operating centers are vacant today for which they are paying rent. Secondly, they are looking to improve digitally and sell services in larger deals.From AR, it might be rational to do some Fermi estimations on how much rent they can reduce. In FY21, they paid around 25 Cr as rent (down from 28 Cr the previous year) with 41 Cr on Power/Fuel and 37 Cr on repairs/Maintenance. (FY21 AR pg 144). They have already reduced expenditure on leased premises (including rent, power, and fuel, repairs and maintenance put together) from 136 Cr to 103 Cr from FY20 to FY21. We will have to see the figure for FY22 in the upcoming AR. But taking the best-case scenario, reducing the rental expenses by 30-40 Cr will only boost margins by a maximum of 1-2%. So, they do need to take certain extra decisions to boost margins. Cutting rents is not enough.

Currently, it has around 708 clients in the payroll business, and in FY2020, the total clients were 686 and 600 in FY16. The payroll/HRO business is an extremely sticky one where it’s hard for a company’s HR to change the software they operate on. This can also result in an ability to pass on increased prices to a certain extent I believe. But it’s also hard to snatch market share from its competitors due to the nature of the product.

It has 254 BPM clients at end of FY21. The number was around 190 in FY16 and 221 in FY20.

The growth of this retained BPM business is pivotal for better margins and profitability. 68% of revenues are of Voice CRM and the remaining are non-voice and transaction charges. The good part about it is that more than 60% of their revenue is from long-tenured clients of more than 10 years.

The management expects revenue to be around 3000 Cr in the near fiscal.So certainly, for better margins they need more clients and better deals as in software businesses, it takes no extra CAPEX for shipping more products and margins do shoot up after an inflection point. The profitability will also be boosted by the interest they receive on cash on the books. Assuming a 5% rate on 4000 Cr of average liquid investments will earn them around 200 Cr every year for a few years. The figure would change in accordance with the cash they hold in the company which can result in extra income between 100 - 300 Crores per year.

-

Lack of Direction regarding the company’s future

The company stated on con calls many times that they want to be a technology player in the field of AAA i.e. Automation, Augmentation, and AI. There is a complete lack of clarity over the kind of revenue streams they want to generate over the years and the areas in those fields where they will focus their attention on. Also, there is an anxiety over the quality of acquisitions they will make in the future.

Either way, I wouldn’t be quick to judge them as its barely been a quarter since the sale is completed. But we do have to watch out for the kind of acquisitions they make and the direction the company is headed.

Plus there is a bitter family feud going on in the Hinduja empire plus some tax evasion cases on one brother which makes the market more anxious about the future of management. Some of these are legitimate concerns. -

Bad and Beaten down market

The last reason I believe for the beaten-down valuation is the general bear market sentiment where every bad news is amplified multiple times by investors who are generally driven by emotions. Unlike the bull market, where the exact opposite happens. I think we as investors need to worry the least about sentiments as it doesn’t affect the business or earning potential. On the positive side can lead to great prices.

This is one of the more unique situations in investing that I have encountered. The business itself is not exceptional. Mediocre at best. The reason I am betting on this is due to its sheerly cheap valuation. Uncertainty regarding the above factors discussed has led to the dirt-cheap valuations here. If things were truly certain, the stock would have been priced accordingly. Uncertainty sometimes can bring great deals and even though not ideal, but it can be rational to bet on such situations provided there is a great margin of safety involved. And I believe at these levels here, there is. It’s like a free option call where there is not much to lose but a lot to gain if the management can actually deliver a good ROI on acquisitions. True, it has to be closely monitored as there are certain risks involved as well.

Going forward I have to very closely monitor these factors

1. Quality of acquisitions and buybacks

2. Lending to promoter entities

3. NPM and revenue improvement of retained business

Does anyone have any views on this to help for better understanding?

Disclosure: Invested a small percentage of PF while having understood the risks involved. Closely watching

9 Likes

Please refer to the thread discussing “Dead Companies Walking,” where Hinduja Global Solutions is discussed as a potential candidate.

1 Like

Went through the annual report and got the feeling that these guys have not done justice to the non-promoter shareholders. The related party NCDs they deposited in, give yield of 2.5-4% p.a. which I feel is very less as compared to Bank FDs but they repeatedly state on call that they get more than market rates and they know these companies well.

The NXTDigital merger transaction also seems like a way for the promoters to sell their loss making business to a recently wealthy company. I see no synergies in their operations but they keep on insisting on it. I couldn’t get old financials of NXTDigital but as per the segment reporting note it seems it was a loss making business which got a swap ratio of 20:63. The promoters must have pocketed somewhere north of Rs 900 crores by tendering these new shares in the buyback.

Entered this stock a long time back and gained a lot from it. Recovered my cost and but it still consists a good part of my portfolio. Now will exit seeing the level of corporate governance. I was excited about the stock seeing the new buzz around AI but I believe these allocation and governance lapses will outrun the cash flow from the remaining businesses. Teklink seems like a good acquisition but can’t stay just for that.

2 Likes