Company recently launched Himeya brand under its flagship. In my view, a very good move!

1 Like

what are views on yarn exports in general and the textile sectors potential in the next 6-18 months.

Q2 Results are out. Some observations:

- Their revenue has grown QoQ and YoY. It looks like the industry is slowly recovering. However, we need to see the effect of inflation.

- Cost of cotton has decreased over last year. But, in quarterly report it shows that the cost of raw materials have increased. Not sure why.

The cotton futures prices are trending upward. It is expected to have upward pressure in coming months. So, the industry is still not out of the woods. - The primary change in operating expense is the change in inventory. It appears that the inventory is still piling up as can also be seen on balance sheet.

While the company’s numbers have stabilised since last year, it appears that they still have a long way to go and repay their debt.

Disc: Invested.

2 Likes

Have you attended concall…can you share notes

Thank you

I found the management quite bullish on this concall, which is different from the usual very conservative style. They maintained their stance of ‘stable demand outlook with an upward bias’ whilst answering all questions.

- In further questioning, they sounded more bullish when guiding that capacity utilisation should reach in high 90’s before 3 years from high 60s currently. When I asked them about triggers for this on the call (below), their reasons were pretty well outlined, though obviously it still has to play out.

-

On debt, they are happy to work on it to reduce it year by year, rather than doing something like raising capital at these valuations.

-

IMO, valuations are very attractive versus peers still for the kind of business/management this is purely because of above debt. Versus the likes of Welspun/ICIL, I think Himatseide can do some good catching up on P/B P/S in case they are able to pare down this debt (even if in a longer timeframe/maybe dilution at better than current valuations over time in a favourable business environment)

-

There is significant capacity headroom here without needing Capex in case a bull cycle is coming with all the triggers in the sector (coming out of destocking, issues with Chinese cotton ban, Pakistan industry issues, potential FTAs, new products/divisions, domestic product launch). Currently capacity utilisation for them is in the high 60s.

Essentially, I invested as I thought in the next few years the R/R was favourable and there is a chance of the dual engines of earnings growth + multiples expanding in case the situation plays out for the company.

Disclosure : Invested as core PF position in self and family accounts and hence I am biased. I am not a registered SEBI advisor and this is not investment advice. I have made transactions in the last 30 days at lower levels.

4 Likes

While I agree there is ample scope of operating leverage to play out and the possible near term triggers for the sector (FTAs etc), I am not so much sure how such downstream players shall perform when cotton/yarn prices begin to rise. With discretionary demand already tepid not sure there will be too price taking from the ultimate consumers. Also, I felt the sudden QIP done was quite contrary to the management’s tonality in the Q2 concall. Scope of RoE and RoCE expansion is also very limited as compared to its peers.

Valuations are ofc in favor but that’s across the textile industry.

2 Likes

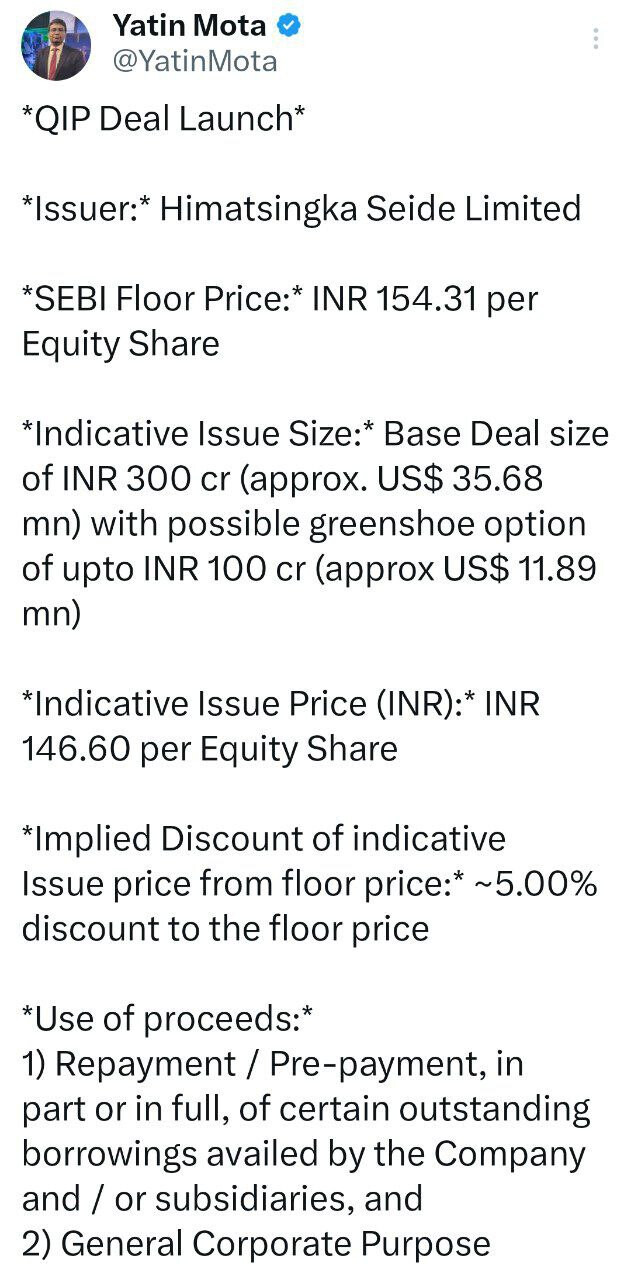

QIP placement initiated at Rs.154.31 per share (with a potential 5% discount). Not sure if they plan to raise the full Rs.400 crore that was approved, nothing mentioned in the filing here. https://www.bseindia.com/xml-data/corpfiling/AttachLive/ac63fb11-0298-4449-b740-fbc6d119e341.pdf

Results have continued to underwhelm over the past year with no change in debt situation as their cash flows have not supported debt reduction in any way so far. I am not sure if they plan to use these funds to reduce debt. Anyone knows?

Debt aside, valuation is reasonable and moderate textile tailwinds seem to be there. Guess this quarter’s result may indicate if they are benefiting.

1 Like

Given the management is going ahead with the QIP, it knows that there are better days ahead. I just exited the counter after losing patience on the subject of debt management.

2 Likes

KEY NOTES FEOM Q2 FY 2025 CONCALL

### Business Update:

- Q2 FY '25 total income decreased by 6.4% due to a recalibration of the brand portfolio.

Capacity utilization reported as follows:

- Spinning division: 99%

- Sheeting division: 61%

- Terry Towel division: 67%

- The recalibration process is expected to impact operations for another 4 to 6 months.

### Strategic Initiatives:

- The company is reassessing its brand portfolio to balance value proposition against revenue and costs.

- Aim to add new clients and explore new markets as part of the recalibration strategy.

### Domestic Market Performance:

- Significant improvements in revenue from India during the first half of FY '25 compared to the same period last year.

- Targeting to grow India’s market to approximately ₹1,000 crores over the next 5 years.

- Currently operating with three brands in India: Himeya, Liv, and Atmosphere, across multiple product segments including bedding, bath, drapery, and upholstery.

- Distribution presence expanded to over 460 cities with more than 3,000 points of sale.

### Financial Developments:

- Successfully completed a ₹400 crores Qualified Institutional Placement (QIP), with proceeds primarily aimed at repaying term debt, which will significantly reduce net debt.

- Net debt as of September 30, 2024, was ₹2,679 crores, marginally up from ₹2,671 crores at the end of June.

- Operating cash flow has averaged approximately ₹300 crores over the last few years.

### Margin Guidance:

- Current EBITDA margins are hovering around 20%, with management indicating they can fluctuate between 18% and 22% due to product mix and inflationary pressures.

- Management remains optimistic about maintaining margins despite cost pressures from container costs and high cotton prices.

### Export and Textile Demand:

- Outlook for exports remains buoyant, with ongoing efforts to enhance market share.

- The management anticipates increased interest from U.S. retailers due to shifting sourcing strategies (China Plus One) and geopolitical factors.

- Other jurisdictions (EU, UK, Middle East, India) are also expected to contribute significantly to growth.

### Challenges and Headwinds:

- The recalibration of the brand portfolio is causing short-term revenue impacts, particularly in the Sheeting division.

- Management acknowledges that some revenue streams may be subdued in the near term due to this strategic repositioning.

### Future Outlook:

- Management expects to achieve a revenue run rate of ₹4,000 crores at full capacity within the next 18 to 24 months.

- The domestic business is projected to grow to ₹300 crores to ₹400 crores over the next two years, aligning with overall EBITDA margins.

### Brand Portfolio Insights:

- Approximately 30% of revenue currently comes from branded products, down from around 40-50% two years ago.

- The company is actively working to optimize its brand portfolio, focusing on brands that provide a viable value proposition.

### Working Capital Management:

- The company is addressing increased debtor days, cash conversion cycle, and inventory days, with an aim to improve working capital cycles by the end of FY '25.

3 Likes

Lately in dec 24 quarter, Sunil Singhania and abakkus fund (which is also his fund) has entered in Himatsingka seide.

Any new developments in the company? Or any kidn of updates/guidance by promoters?

1 Like

There have been 4/5 announcements regarding top management resignations in last month or so . Anyone has any idea why so many resignations suddently ?

1 Like