Good operating margins. Huge Capex is added but I prefer to wait till Earnings start to rise along with trend. Currently not comfortable with Interest Coverage Ratio

1 Like

Highlights from earnings call

- Q1 FY’23 performance was adversely impacted due to the unprecedented levels of high raw material prices, inventory correction

being undertaken by major retailers across markets, a softening of demand and continued supply chain disruptions. - Capacity utilization is quite low due to above. So, capex plans are put on hold.

- Overall revenue came down by about 15-20%

- Going to be challenging for coming 2 quarters due to clients doing inventory correction, supply chain issues and rising inflation on raw materials

- Last quarter was a loss of 54 Cr vs a profit of 82 Cr in prev year

- There is a slight increase in debt level

- Mgmt says it has never seen this level of inventory correction & inflation since last 15 years.

- Mgmt frankly admitted that they were unable to bring leverage levels down, but are aggressively working towards it.

- Expecting the FTA with UK to be a positive development for textile industry

The theme of investing is as follows:

- Good Management which seems to know what they do

- It is a tough time for the industry and the valuations are attractive if we look at a 2-3 year horizon. This is not for people looking for quick turn around at this point.

- A lot of capacity is unutilised at this moment. So, the company can claw back to high revenue realisations without much capex. Furthermore, the already planned capex will come into play after the demand picks up.

- TTM PE is quite high. For cyclical companies, this is the right time to pick the stock as earning pressure will ease out in coming quarters.

Things to watch:

- Industry cycle, cotton prices and capacity utilisation across other players

Disc: Invested. Might nibble a bit more.

3 Likes

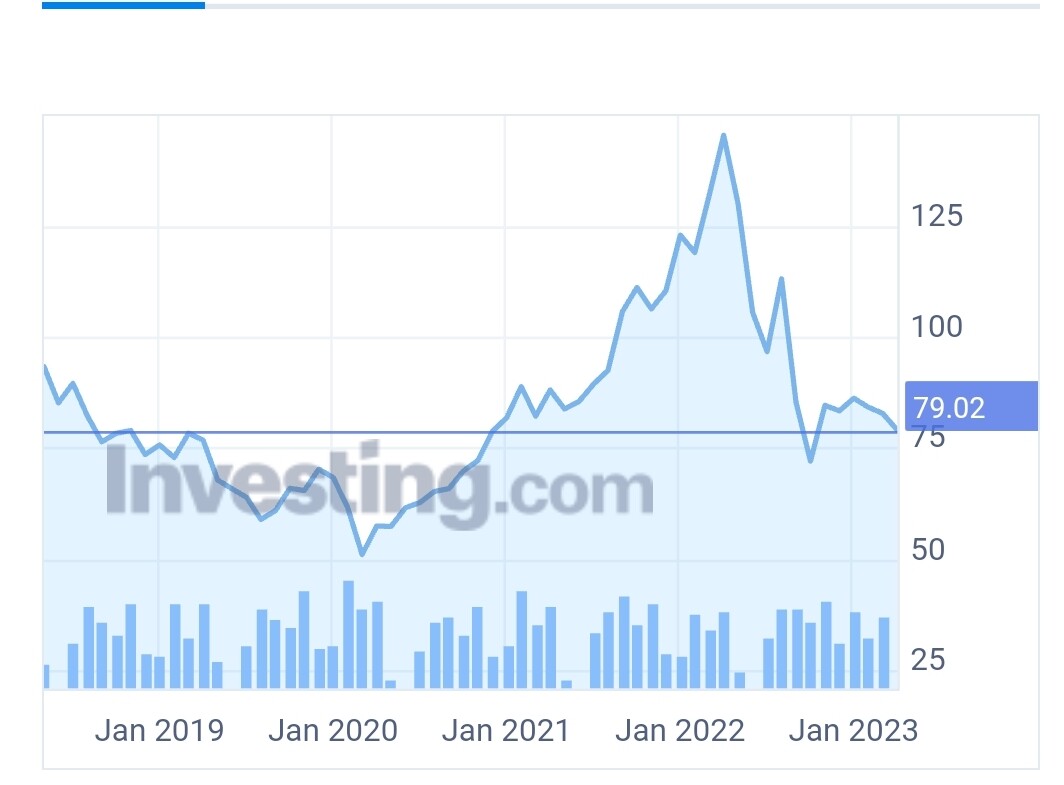

Mills are reporting unbeleivable losses, due to high cotton prices. Many mills have shut their operations. But Cotton prices are already down a lot from the peak, however still above multiyear average. I saw an interview on CNBC wherein the official said that from mid october things should become fine. However benefit of low prices will only be available after 2-3 quarters as most of the companies and mills keep inventory of 11 months, however this time at such high prices mills and textile companies have not added to their inventory, and currently the inventories are reduced to around 7 months. Almost all textile companies are waiting for low prices in cotton to buy inventory.

Also do you have any idea, that how much of the cotton that they use are produced by themselves in their farm. I still wonder that if they were fully integrated then why, cotton prices affected them so badly. If you can help me understand?

Yep. The demand of cotton should come down and supply should ramp up. Seems the prices have already corrected significantly to pre-COVID levels.

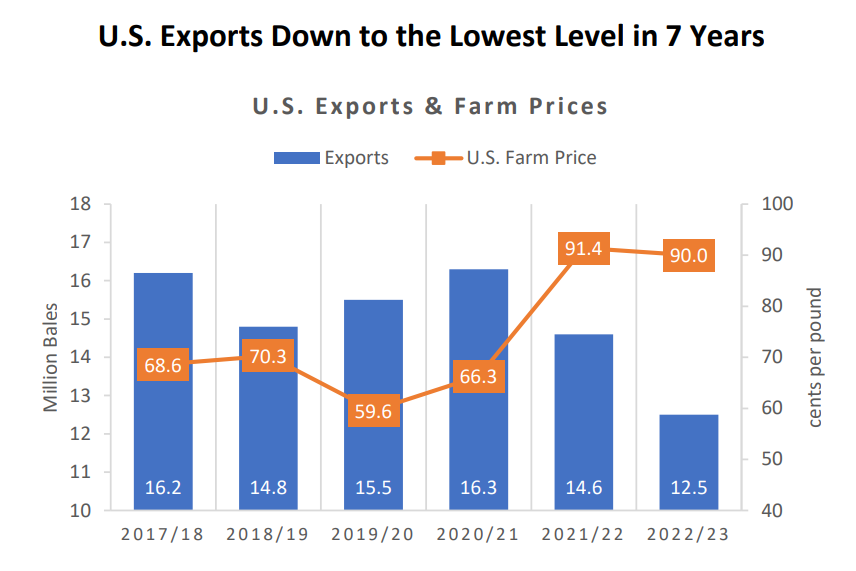

Meanwhile, I am also expecting the production volume to trend upwards. Below is a view specific to US, but it is relatable to Himatsingka as it consumes american cotton as well.

Most of the indicators say that the cotton prices should stabilize and therefore margins should expand in another quarter.

In terms of vertical integration, it is better to assume that they are not producing significant amount of cotton themselves.

IMHO, the integrated biz model is on following aspects:

- Direct Sourcing: They may be having contracts / agreements with farmers and thereby do direct sourcing. Cotton is about 60% of the cost. So, the co is almost directly affected by cotton price as others.

- Yarn manufacturing: About half of yarn requirements are met in-house. This avoids inefficiencies in passing on cost adjustment from cotton to yarn to end products.

- Branding and private labels: This is their strong relationship with clients and also the way they differentiate themselves in the industry.

Info on sourcing cotton from partner farms (annual report)

More details on their integrated business model in the report below (section - Integrated Business Model)

2021-10-01_5300_Ashika - Stock Picks – Himatsingka Seide Ltd. - October 2021.pdf (600.9 KB)

2 Likes

Cotton price forecast report in public domain. Looking at a possible recession in US, we also have to look at the exports of the company.

Was researching about the company in LinkedIn to see what they are upto.

They seem to be moving ahead in terms of recruitment, which is a good news.

From Linkedin data, it appears that they had added at least 22 people in Jan 2023. It is a good sign that shows the confidence mgmt has in the business.

They also hired a very qualified person for business development. (https://www.linkedin.com/in/manu-kapur-46969066/).

Eagerly waiting for the quarterly results, which I expect would be below general expectations. Debt is already high and interest coverage is under pressure. Hopefully they come out of this tough time unscathed.

Disc: Invested, less than 5% of portfolio

2 Likes

Positive results, but the debt is too much

If they reduce it? See what happened to Trident.

yearly profit 120cr avg and debt is 3000cr

I think better number would be to see cash Flow from operations minus cash from maintenance of fixed assets(since a major capex has already been completed) vs the total debt. I think it is a buy for me at 50rs. I may be wrong.

Disclosure. Carrying out SIP regularly in this

2 Likes

Management saying this too often that “we will take this with you offline.”

Cotton needs to correct 20 percent from here (65000bucks per candy) in order to see normalisation

**When asked from the management about the future outlook **

Pricing power is one of the biggest challenge in the industry. Management calls these year as a once in a lifetime exception.

3 Likes

Just went through their earnings call

Positives:

- Capacity utilisation improving gradually.

- Profit margin is inching back up.

- Mgmt commenting that there is uptick on orderbook.

- Improvement on raw material costs.

- Taming down on the energy front in terms of costs.

- Some easing out of supply chain costs

- Potential for India to sign FTA, which could unlock more opportunities.

- The inventory correction initiatives sort of coming to a closure, which should unlock more demand.

- There might not be much capex in the immediate future.

Cautions:

- Pricing power is generally a challenge in this industry.

- Debt and working capital is a bit too high. This will have negative impact with rising interest rate.

- A lot of tailwinds allude to FTA, China+One, Pakistan economic crisis etc. which could not materialise or might take much longer to pan out.

The pricing looks attractive at this level. But, this should be a long term play for at least until interest rates come down (2-4 years)

Disc: Invested

What are you views on sportking India, I think they have a major benefit that they are getting power @5 per unit as per their presentation.

What explains cotton prices in India crossing previous highs. No one would have expected this, in my opinion

Lets see if the same happens in USA May futures

It looks more like supply contraction and some offshoots of demand picking up. Not sure how long this (supply contraction) will last…

Did not think about it that way, but a fine perspective and a possibility. lets see.

Can someone explain me how is this fundraiser effect us, definitely a positive but pls explain?

Intimation of Securities Allotment Committee Meeting to be held on Tuesday, March 21,

2023, to open issue of Foreign Currency Convertible Bonds (“FCCBs”) and Non-Convertible

Debentures (“NCDs”)

The company has issued debt, the money received will help the company in meeting working capital requirements/ functioning/ operations, The debt to equity which already is high will increase more. The good thing is that company will now have sufficient capital to handle the tough times, and that the equity has not been diluted. The thing of worry is the increasing number of debt and thus the high interest cost which you will see in quarterly results.

1 Like

Some more pain for FY2024. The margins will have sustained pressure for this year.

1 Like

Textile brokerage report nuvama.pdf (493.8 KB)

A report by nuvama on textile sector.

Apparently they see better margins going ahead.

I still see a huge spread between Indian Cotton and US cotton. I expected it to close in, but the price of Indian Cotton has sustained

This is for US cotton

This is for Indian Cotton

3 Likes