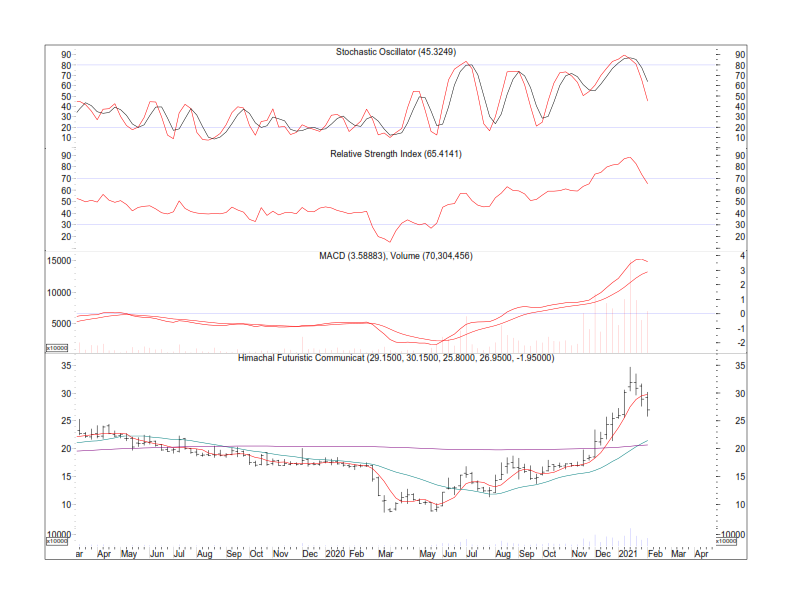

Q3 results summary - also summary from interview of Mr. Nahatha

a. Results have been quite good. pls check numbers on your own. what caught my eyes is increase in employee cost , decrease in material cost and increase in finance cost.

– Clarification from Mr. Nahatha

. Employee cost due to R&D new hires. expected to go up in near future as Bangalore R&D center would be fully operational.

Finance cost ~9.5%

Raw Material prices have fallen in the market and has helped the company. expected same for Q4.

–overall EBIT improved by 1.8% which I think they will make it again.

key factor contributing is product revenue is increasing - WIFI Router + Telecom products + OFC % improving v/s turnkey solutions. as more products are inhouse designed and manufactured the trend is expected to continue.

HYD facility is operational . They have invested to expand capacity already + more capacity to be added in FY21 as well. THey are extremely bullish on the FTTH cable story overall.

Market reception of WiFI router has been very good. - 54Cr contribution in Q2 and about 70K in Q3. (telecom products excluding cables)

Export sales has increased about 40% QoQ. they have invested in sales people in key markets to improve this further. Internal target of 300% export revenue growth

Overall demand is strong, EBIT has improved and Q4 would be inline with this EBIT.

Key Risks noticed

a. Debtor days have increased. key reason being COVID related receivable delay. some project exectution delay due to Covid as well. expect to come to normal levels in Q4.

b. Defense product sales - eFuze , Night vision & High Capacity radio - products are ready, tested etc. Approved for RFP by defense but decision to award will take time. for eFuze - 4 key players in the round , L&T., BEL, ECIL and HBL. Only HFCL is designed and made in india . others have tech tie up and IP is not owned by them.

for eOptics as well - story is same. they have designed and made 3 products already and have been shortlisted by defense . trials are to start.

High Capacity radio is where i think story is better. still no decision on RFP. .

Defense deals will take time and this could be end of FY21 or even FY22 before it hits the books.

Short term uptick hence is depending on FTTH and Telecom products story. Which has a huge demand pipeline as well and hence not very concerned about defense not materializing into revenue anytime soon.

One good thing i noticed is that for Railway communication network - they seem to be the only player in India who has deep expertise owning to lot of key projects that they have delivered already

a. Dedicated freight corridor project

b. Delhi Metro

c. Dhaka Metro

d. Mauritius Metro

Final Summary - 2021 revenue uptick is lot more dependent on

a. On time execution of projects and revenue realization

b. More secular demand for telecom products (WiFI , switches , UBR etc) - some export order would be nice. there are trials ongoing in ASEAN and Eu at the moment already.

c. OFC, FTTH - more installation and export

d. Improvement of the working capital cycle

e. R&D center - fully operational.

Discl : Invested