Very Nice presentation

Attached is my presentation on HIL- Presented in Valupickr Forum Bengaluru Chapter on 19th May 2019.

Disclosure: Vested interest and biased viewsHIL-Presentation-WithoutVideos.pptx (1.5 MB)

3 Likes

@atulastra Normally, i worry when company do foreign acquisition (big size) and increase debt. There are many examples where such attempt failed and company gone in trouble.

Hence, i will wait and watch to stabilise the new acquisition done by HIL.

Posted results are not so great as interest is eating in to low margin business. let’s see if the bet pays off. I invest for minimum 5 years. Thats the time company with strong base normally shows good returns. Happy investing

Disclosure: Vested interest and biased views

I was a bit more taken aback by the Parador acquisition. A quick back of the envelope calculation suggested that the business was loss making and that was what was pulling down the margins.

Maybe I’m a pessimist, but I fail to see how buying Parador outright is going to benefit the company without some major restructuring. It is irritating how the MD is quick to point out the revenue potential in interviews and presentations, but goes silent when it comes to the margins.

3 Likes

Hi Atul, Thanks for your ppt on HIL.

The Parador acquisition as few ppl above have also pointed to be costly.

I wanted to bring this to the discussion:

acquisition cost of Eur 82.8M, however only 32M was raised in Euros with interest cost of 1.6% while >60% was raised in India at 8.6% interest rate.

Do you think the Euroean banks may not have agreed to pay more loan for this asset. and if true, does it mean a costly acquisition from HIL perspective.

Thanks,

Mayank

1 Like

Very interesting to see the margins as one cannot earn from a business having 4-5% margin but paying interst at 9%.

On contrary if you see it as complete solution under oneroof for the customers it becomes a different story altogether, as a whole they can extract more money from every single customer. They don’t have high margin business and cost needs to be watched closely.

Annual report post acquisition is not available. I will be able to make more comments post going through the annual report of the company. The stock to me seems to be a safe bet with atleast 3 years of investment view. The bet is on sector revivial with PM promising to double farm income by 2022. Volumes will bring in the profits not margins.

Hope I could answer some part of your question.

Happy investing.

Disclosure: Vested interest biased views

2 Likes

Hi,

I have done a comparative analysis of quantitaive data of HIL Ltd. with its peers, Everest Industries and Visaka Industries. Though both peers also have different business to go with the core business is same for all the three companies.

I have taken standalone data from Ace Equity for all the three companies for comparison purpose. I have analyzed them on parameters which I felt were necessary to judge them better. Will be following this with conference call analysis of the three companies to understand the nuances of their businesses much better.

Please find the analysis on the link below

1 Like

into new technologies to bring more efficiency

The industrial thermal insulation business includes manufacture, sales and export of calcium silicate insulation products sold under the brand name HYSIL. The products are in the form of pipes, blocks or specific shapes, including calcium silicate, which are used for insulation in various industrial applications, the sources added.

HYSIL has the largest manufacturing capacity of calcium silicate insulation products in India and South-East Asia.

HIL Limited Q3FY20 Concall Summary

Business Update

- Challenging quarter considering all perspectives

- Birla Aerocon maintains its leadership position and is operating at more than 90% capacity utilisation

- Contemplating capex in building products division going forward

- Parador is focusing on penetrating the markets in China, USA, Spain & UK

- The Chinese JV is working on a positive EBITDA

- Roofing solutions business de grew by 15% due to a slowing down rural economy

- Will utilise proceeds from HYSIL sales towards pre payment of long term debt

Participants

• Unifi Capital

• Equitas Investments

• CARE Portfolio Managers

• Securities Investment Management

• Ratnabali Investments

• ICICI Securities

• Finvest Securities

QnA

- The roofing business has seen a lighter business in January and since Q4 is a primary stocking month hoping that things pick up

- Availability of fibre is not an issue but prices are up almost 20% yoy and cement prices are also higher than last year

- Have raised prices slightly in January and hoping to pass on more price increases

- Polymer business has been challenging but encouraging also

- The strategy of the management in polymer business is to approach the plumbers rather than selling through big dealers

- In terms of Parador focus is on bottom line and not revenue growth as of now. However have been working on measures for top line growth as well

- The leverage should reduce by 50% over the next one year

- Fibre contracts are annual in nature and it constitutes 20% of total raw material costs

- The pipes business is working on a capacity utilisation of 30%

- The steps taken in the polymer business should see revenue doubling in the next six months

- Competitive intensity in roofing market is very high and the management has not seen competitors raising their prices and the premium between the company’s products versus competitors is very high

- Have been working on cost reduction and efficiency initiatives in the roofing business

- The management has been taking many initiatives in the polymer business and also looking for a new management person to drive the business going forward

- The revenue contribution of pipes and putty segments is about 50% each

- The company is selling its pipes at a similar price to what top players in piping segment are selling at

- The advertisement expenditure will continue in the same proportion as it has been continuing

- Indian consumption is 30% of the total fibre production in the world

4 Likes

Is covid risk rising again…?

HIL shutting down Chennai plant till further notice again…

1 Like

1 Like

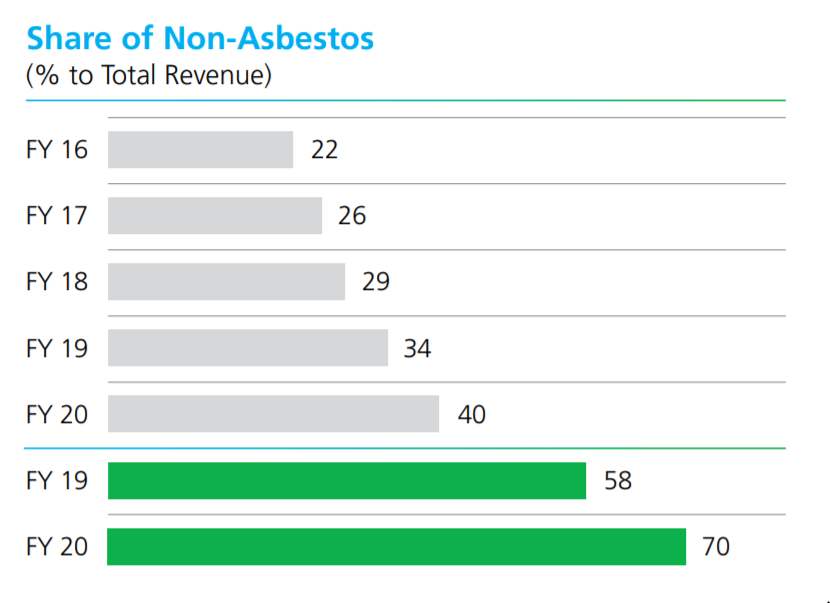

I see the interest here has died down and one of the key risks here was the asbestos was the primary contributor to revenue. This has come down over the years and as of FY21, it should be < 20% and reducing further.

Source: FY20 AR: https://www.bseindia.com/bseplus/AnnualReport/509675/5096750320.pdf

The earlier cheap valuation was primarily on account of the asbestos and also the debt situation post parador acquisition. The company has reduced debt from 740 Cr to 480 Cr in FY20 and recently even further by 250 Cr (have to see FY21 Balance Sheet to see where the figure lies).

Also seeing significant growth in pipes and flooring business

Source: Q3 FY21 Investor Presentation https://www.bseindia.com/xml-data/corpfiling/AttachLive/e500eb43-86d5-43a9-9d9c-e5e0cf3bf059.pdf

I think there’s a chance of a re-rating here as there are significant changes in two things from the past (debt reduction and new high-growth lines of business).

Disc: Invested recently

6 Likes

True. The average PE ratings prior to the September 2018 acquisition of Parador seems to be in the mid teens and upwards. The valuation seems to have taken a plunge post September 2018. But now, with the considerable debt reduction and growth being showcased by Parador, and the Polymer verticals stock seems to be in for a re-rating. If the real estate space picks up further, we could see some additional upside too.

Disc: Invested recently

I think this company has a great positioning in the roofing solutions martket - would be interesting to hear opinion about the management quality.

The investor quality looks quite good!

Disc: Invested a few weeks ago and topped up after Q3 results

Tried to gather the contribution of different segments over last 3 years and this is how it looks. The valuation has been sub 1x Price/Sales due to sub 10% EBITDA margins the business has had and Asbestos/ESG overhang and post Parador acquisition, the perception that it was a poor one and the debt on the books.

At 2850 Cr sales now and EBITDA margins hovering around 12%, with bulk of the contribution from non-asbestos from high-growth businesses, with Long-term debt reduced to 92 Cr (as per most recent concall), the character of the business has changed substantially of-late.

I have been going through recent ARs and concalls and here are some notes to some of the questions I had in mind (in no particular order).

-

Parador Sales - 142.2 million euros in 2017. HIL bought for 82.8 million (687 Cr). Parador was loss-making then. Modular One was introduced post-acquisition and is doing quite well in Germany and Austria.

-

Most of the sales is from online so I checked with a friend in Germany to see if the store locations are valid ones (can never be too careful with these foreign acquisitions) and turns out they are big DIY retailers (DIY flooring is very common in Germany). Some of the vendors I checked are OBI and Hagebau. Reviews for the product in these sites is very positive. Reviews are scattered across SKUs and not consolidated so absolute count could be small.

-

It looks like the Germany & Austria business is now primarily B2C, with the company using Augmented reality software Roomvo. The live version that is bringing in business is here. Shipments go directly from factory to Customer and no other competitor in Germany is currently doing this.

-

Pipes business is actually Pipes + Putty (50:50). Pipes alone can do 350 Cr in next 1-2 years

-

Building materials business will catch up with RE pickup

-

Flooring - 60% from Germany+Austria. China probably after that. Only 8 Cr in India as of now.

-

Would have fully repaid Parador India debt by Q4

-

Parador EBITDA margin at 12%

-

200million euro parador. will be going to 350-500 million euro in the next couple of years

-

Parador at 70% capacity utilization

-

16% market share in Australia in Parador

-

Billion dollar sales target is what the company is working with before 2025. Main contributions will come from Pipes (expecting exponential growth), Parador, non-Asbestos roofing from industrial Capex and building materials (currently at 100% capacity utilization)

Risks

- Once lockdown lifts in Germany (yes there is still lockdown there), there is possibility of competitors gaining back market share

- Margins in roofing business could be hit slightly due to fiber imports from Russia instead of Brazil

- Pipes margins can come down with Resin prices (There could have been some inventory gains in last quarter)

- Parador margins are at 12%. Although company has hinted that margins could go up owing to large fixed costs in Europe as volumes pickup and utilization goes higher, they still keep giving conservative guidance of 10% for this business in Europe. There is also perhaps currency risk if INR appreciates, in terms of revenue recognition in INR.

Disc: Invested around 2500.

14 Likes

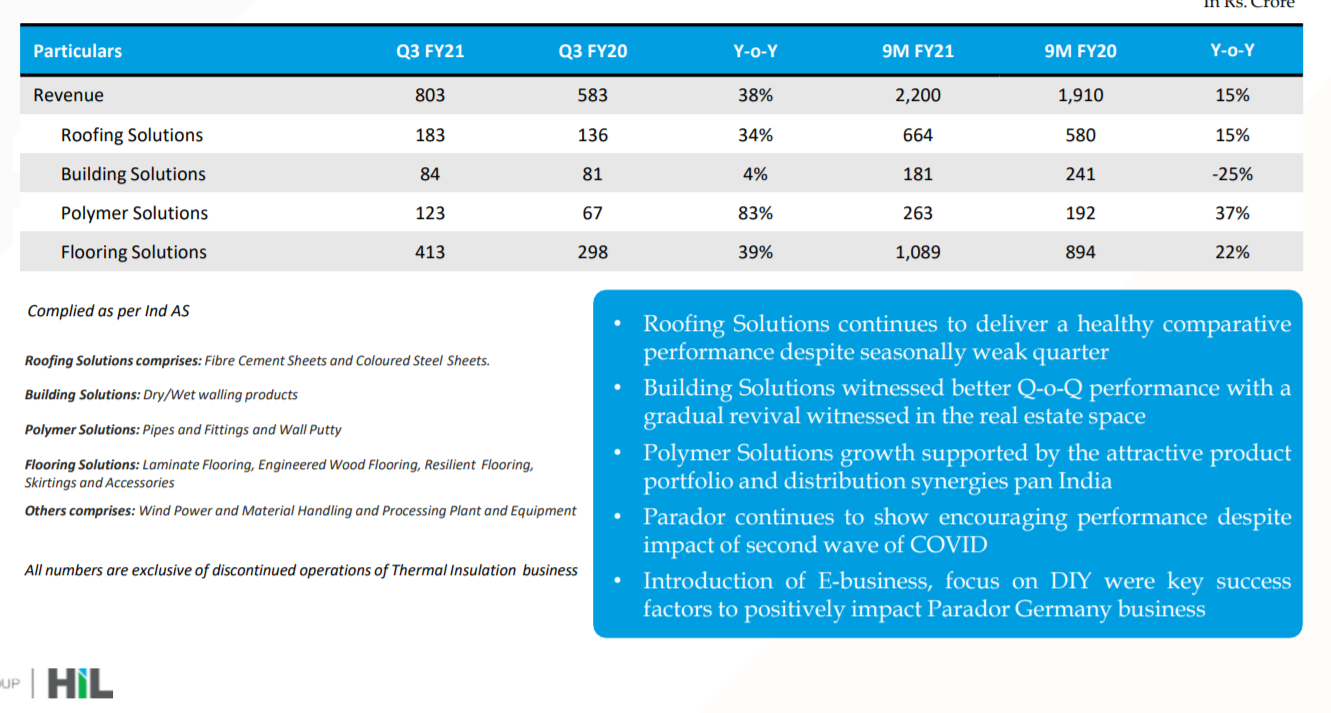

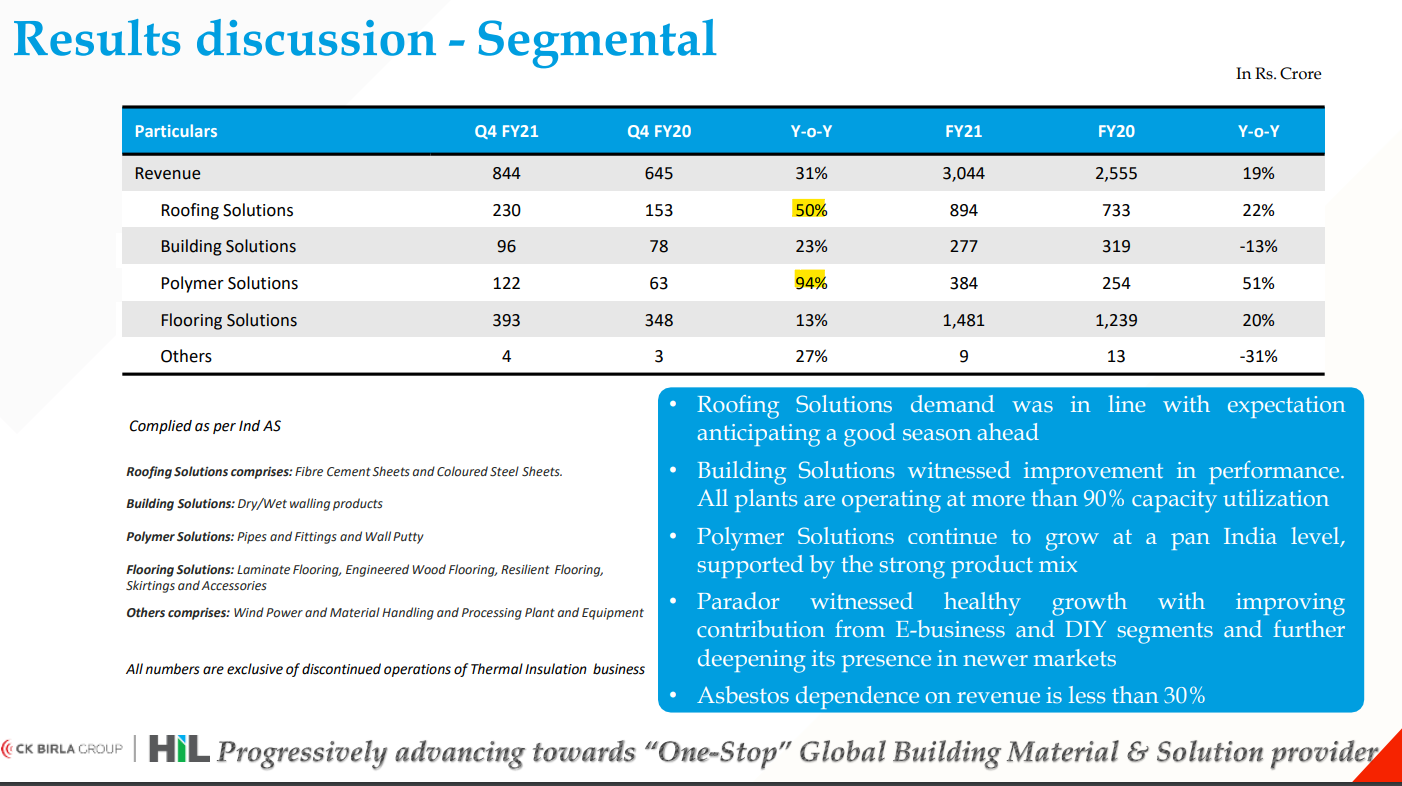

Numbers look quite good for the quarter as well as the year. (Even QoQ there is pretty good growth)

All segments continue to fire. Even building solutions which has been a laggard has grown 23% this quarter. Parador looks to have normalized on the large base, still showing a 13% growth.

Overall EBITDA margins are around 14% for the quarter and also the whole year.

There is significant cash-flow as well with a CFO of 466 Cr in FY21 and a FCF of about 350 Cr (Debt reduction in FY21 at 330 Cr).

Post this, the business is now trading at a TTM P/E of 11 and a EV/EBITDA of about 7 which still remains cheap considering the growth and the runway for growth.

The product mix has considerably changed from the past and current FY21 D/E is 0.41x compared to 1x from FY20 which are both good for a valuation re-rating if it happens.

Disc: Invested from around 2500 levels. No recent transactions

11 Likes