The company is primarily diversified and operates under two niche verticals, which operates independently yet strategically positioned to interlink and compliment the group’s core aim of generating optimum value to all its stakeholders.

The two primary divisions are :

Div 1 - EPCM (Engineering Procurement and Construction Management)

a) Oil & Gas sector

b) Water Sources / Hydro projects

c) Waste management

d) Infra & support services / Consulting

Div 2 - Allied media services (M&A)

EPCM division currently accounts for over 80% of its total revenues, while the rest being constituted by the Allied Media division

The company with its strategic partners has its presence and footprints spread across India with technical collaboration and clientele overseas.

HIGHLIGHTS – EPC div

The Company has built an envious profile in EPC in a very short span of two year and is now eligible to bid and execute for Central as well as various State governments and PSU tenders for variety of category and sectors under infrastructure development which includes Oil & Gas, Power, Telecom, Road construction & maintenance, Signage/Electrical, Installations, Civil work/Construction management and Complex engineering consultation

The Company is already working in various states of India for infrastructural projects and has presence in all states for Consulting assignments, signifying the capabilities to work PAN India. Highlighting on this front, company proudly claims to have worked in more than 1000 cities of India for a consulting job (TPC-third party certification of petrol pumps) with ‘Indian Oil Corporation Ltd’

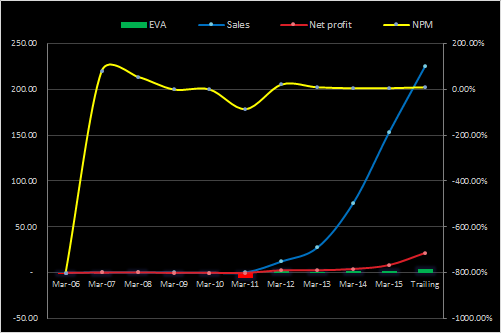

The Company has shown a consistent Y-O-Y (year on year) average growth of nearly 150% in last 3 years.

The Company currently enjoys banking limits to the tune of INR 2500 lacs from Bank of Baroda & Karnataka Bank and is slated for an appraisal of additional 18 crores

Expansion Plans – EPC / Infra Div

- The Company has constituted the Crack Committee which will focus on expansion and diversification into new areas of activities namely:

• City Gas Distribution – certification and verification including design and drawing.

• Water Resources - There is a lot of thrust by central government on water resources. Riverbed cleaning & rejuvenation, Irrigation projects are being negotiated by a consortium of Indian companies with prominent International experts for technical collaboration. We look forward to participate in the consortium to facilitate and execute projects in this sector.

• Solid Waste Management : This is a crisis area in most of the Indian Urban Developments. Disposal of solid waste is a problem for which the government is yet to find solution. The company is in discussion with very senior members of a US based consultancy for collaboration in order to participate and push for work in this sector.

• Telecom: This sector is looking up again after 4 year slump. Infrastructure development for 4G would be a promising field.Consolidation and improvement of service by operators is the requirement of the day. Government would push for reforms to improve the service and this would generate business.

• The Company has identified openings in niche Fire & Safety industry and is to negotiate strategic partnership and acquisition of experienced team/companies to enter in Fire detection & protection system installations & maintenance for industrial & commercial Establishments.

• Consultancy: There is a tremendous scope in the professional consulting assignments. Areas of interest would be petroleum, telecom, water resources and information technology.

With more than 150 experienced professionals on field and a strong team of 35 professionals to manage projects, company is poised for major expansions.

HIGHLIGHTS- M&A Division

M&A activities of HGEL though currently contributes only 15-20% of HGEL’s topline revenue but looking at the team expertise and its network, has the potential to expand and grow rapidly with healthy bottom-lines.

This division currently has two channels of revenue viz. Domestic and Export sales of its services, which are offered not only on the standalone basis, but also as a combination of more than one:

Content Development & Integration

Development and acquisition of finished or unfinished content for theatrical, broadcast (Film&TV / IPTV) or Online/internet.

Integration of content with Value Added Services

Distribution of content/IPR locally & overseas

Post-Production& Technical media services BPO

Editing, VFX/Animation, Grading, Special Effects, Sound Mix & Packaging.

Stereoscopy / 2D-3D conversion.

Restoration, Archival, Migration, Encoding, Transcoding, Compression & Authoring, Standards & Format Conversion

HGEL has recently set-upa boutique digital post-production/technical media facility in India, to cater to its domestic and export market; The facility is located in Mumbai and is now fully operational.

Alongside HGEL continue operating and servicing overseas/export clients via sublet mechanism through strategic partners in Georgia, Russia and London.

HGEL also has line production and operational arrangements in UK, US, Fiji Islands, Georgia, Australia and Malayasia for co-productions and consultancy services.

Expansion– M&A Div

-

HGEL is in advance stages of negotiating with an American company head quartered in Los Angeles. The strategic co-production and post production tie-ups are being streamlined to leverage and optimize the available production incentives in the state of Georgia, USA through their integrated Studioplex. Simultaneously working out their technical outsourcing and IP collaboration in India.

-

Additionally HGEL in partnership with them will be leveraging the Malaysian tax rebate (FIMI) to create:

a) A production slate of 4 MULTI-LINGUAL films to be shot in 2015-17

b) A production facilitation service that will bring mainstream Bollywood film makers to Malaysia

c) A post production platform in conjunction with the Malaysian Government’s Vision 2020 program to maximise digital content creation

d) A stereoscopic conversion facility to create 3D versions of superhit Bollywood movies

-

Adding value to our current production expertise and to compliment its in-house post production arm, HGEL is looking to expand its line production streams to develop and create varied content for advertising, internet/IPTV, broadcast and other digital platforms; regarding the same company is in advance stages of negotiations to acquire majority stake in an established production house specializing in corporate and Ad-film production.

-

On a retainer ship model HGEL is in advance talks with a prominent shopping channel-network to set up 2 shooting floors/studios to do video cataloguing / making Ad-films of various products for their teleshopping channels. Further HGEL plans to rope in other e-retailer clients like ‘Jabong’ and ‘Snap-deal’ to do their still cataloging as well.