Does anyone know the client list of the company? Because I couldn’t find it on their website.

I also couldn’t find any clientele list for this. However, I did find some risks (from the time of IPO filing):

- Company and its Promoters, has in past defaulted in payment of income tax and has certain outstanding income tax demands. Lot of Income Tax Defaults in the past does not augur well for the company.

- They are raising ~16 Cr from IPO to fund a manufacturing unit. Total cost of Project is ~40 Cr. Out of this ~31 Cr will be for purchasing machinery, and out of that ~20 Cr of Machinery will be purchased from their Related Party. This is risk in the business because we do not know whether the deal is happening at Arm Length price basis or not.

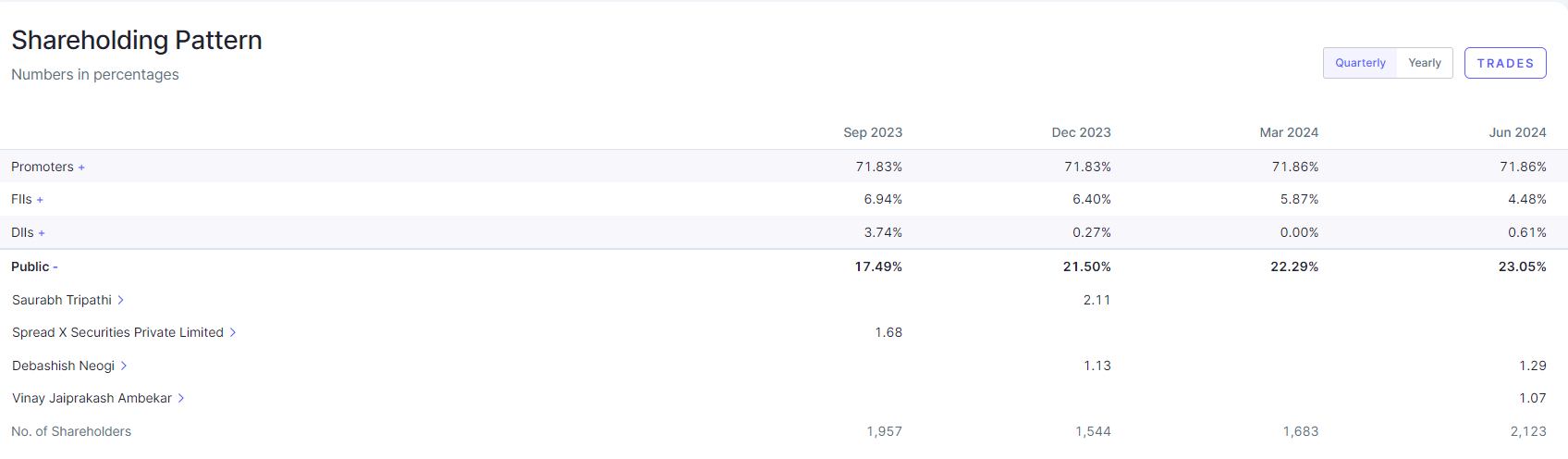

- The high valuation demands close scrutiny, especially in terms of the company’s ability to meet growth expectations. Also, investors should consider the ownership structure, as RNG Finlease Private Limited holds a majority share of 71.58%.

2 Likes

RNG Finlease can be considered as holding company only. It is a company of relative of Shaileshbhai Makadia and Amitkumar who are other promoters, main decision regarding company is taken by both of them.

In past due to some financial issues they had to sell stake to RNG Finlease which is situated in Morbi, Gujarat. These issues were before the company was listed.

Know all this due to past business relations with some promoters

regarding tax defaults, yes in past in other companies of promoter group also (unlisted) there are problems

2 Likes

Jimmybhai

ive came to know about the promoter group when coal gasifiers (Radhe coal gasifier) business around morbi and places were blooming.

I see this “hi green” technology as an extension to their gasification/pyrolysis know how. I presume their cost of production would be competitive.

1.Are they also into business of doing EPC of "carbon black plant ?

2.What is your feeling about standard of governance at the group ?

No idea aboit the first question as I was involved with group upto 2011-12 only. One of my relative was director in Radhe group, Rajkot

Std of governance as far as I think/know is they can do some odd/wrong things but won’t let share price down due to that. Minor govt governance issues are always there in SMEs , we can’t expect TCS/HDFC lvl of governance from them. Minor hiccups can’t be excluded here but no dark clouds as per me

5 Likes

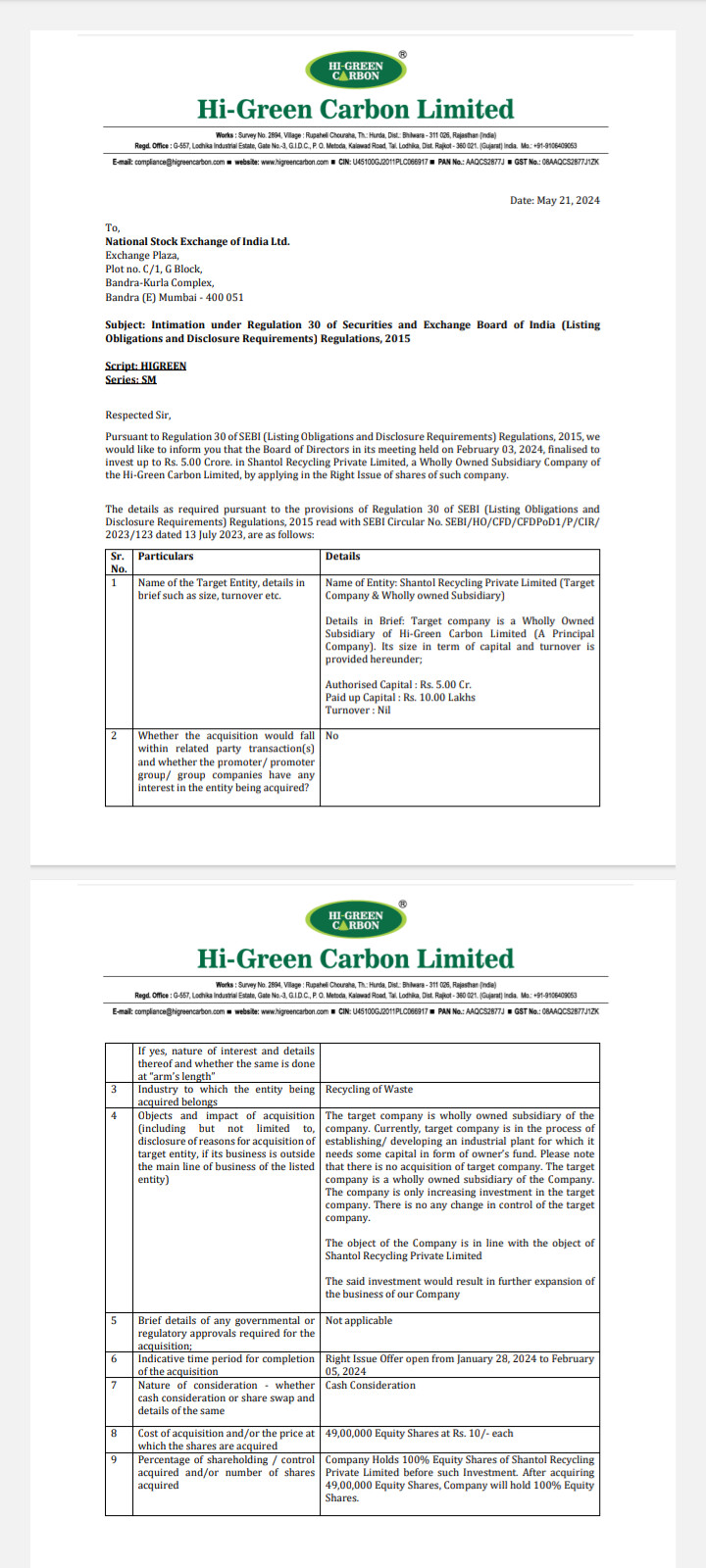

Can anyone explain what is this latest investment of ₹5Cr in Shantol Recycling Private Limited by company is all about

1 Like

Would Hi-green be a beneficiary from the EPR regulations? Any idea on how we can check for EPR listed recyclers?

I searched a lot but could not find a way by which tyres can be permanently disposed off apart from pyrolysis. All other methods e.g. conveyer belts etc would still at some point end in a landfill.

Does anyone have an idea if tyre companies would move to recovered carbon black instead of using virgin carbon black?

Also in an older video, the founder spoke about further enhancing the quality of carbon black that should help replace carbon black, did that happen?

Disc. Invested

3 Likes

hi let me try to attempt to respond:

- short answer - yes. they would benefit from EPR regulations. they have already booked appx 2cr as income from the same last year (if my memory serves me right).

- absolutely right. that is why pyrolysis is termed “cradle to cradle” whereas other forms of recycling tyres are typically “cradle to grave”.

- tyre cos do use rCB in varying proportions. today capacities of rCB are less compared to the requirement of tyre companies. but if the rCB is of sufficient grade and quality, it can be used to partially substitute VCB in the process.

- for now the higher degree purity rCB is still in lab stage. the same can be used in filtration systems and uv applications. however, the company is right now focused on their basic business and expanding it due to the buoyant demand for their products. My guess is that parallelly they are working on developing these higher end products, however it is not a core focus area for them at the current juncture.

10 Likes

Similar company of US look what they do

1 Like

Hi Green Carbon Certificate.pdf (1.9 MB)

Hi-Green @ Industry Outlook.pdf (321.8 KB)

3 Likes

Good company delivery value wrt products in its industry

-

How does the pricing of its products compare wrt competition. Given they are commodities so relevance of low cost of production, and hence the query.how big is margin risk and does company suffer higher cost of production relatively to compete.

-

How strong is r&d moat and tuff to replicate as pyrolysis is commonly done internationally

-

How easy it is and how strong are incentives for customers to adapt to recovered carbon black compared to their systems already aligning with virgin carbon black (has higher carbon content)

1 Like

While most of the below has already been covered in various posts above, i am trying to give a high level summary of the business model in the framework of the below 4 pillars:

1. Raw Material -

- end of life waste tyre. abundant availability.

- which otherwise would have been burnt as fuel (causing lot of pollution)

- or else just dumped in landfills, where it doesnt decompose.

- and how higreen is solving this problem.

- 100tpd is currently their sweet spot in terms of being small size, so less risk, faster to set up, easier to sell the quantity of products produced, easier to buy the raw material, easier to operate and replicate in different locations, thereby spreading the risk.

(to arrive at this, they did lot of testing in lab - starting with 100kg reactor, micro reactor, vertical reactor, electricity fired, diesel fired, screw, barrel, double pass etc. practically every technology available in the world had been tested by them to arrive at where they are today) - they claim to be the largest single location plant operating at commercial scale in the world.

2. Finished Products -

- cradle to cradle concept.

- the rcb is reused in rubber products.

- which again can be recycled (ofcourse with lesser efficiency).

- it replaces vcb which is a crude derivative.

- the pyrolysis oil is a fuel alternative.

- the heat energy output is being used to make raw glass (currently), but going forward is likely to be used to generate power (about 1.5-2 Mw per 100 tpd plant, which is not very large).

- wide industrial usage of its products.

3. The Process -

- how continuous pryrolysis is so much better than batch process in terms of efficiency, power consumption (and wastage), reduced pollution (nil solid discharge, nil liquid discharge, flue gas composition meets stringent pollution norms), and quality of the finished products.

- its a suction based process, so no incidence of any pressure points in the reactor / kiln.

- various domestic and international environment and pollution certifications already obtained.

- how the company’s pyrolysis process is self sustaining in its energy needs (the heat produced from the process is used back into the process) and excess heat is used to generate power.

- how plant can be run 24x7 with just a monthly maintenance shutdown.

- small amount of external energy is used only at the time of restarting the furnace after maintenance, post which it is self sustaining. their own pyrolysis oil is also used in restarting the reactor.

- how the plant can be remotely monitored and partially controlled from anywhere in the world on computer / mobile phone.

- how it requires very less manpower to be actually present at the site.

- the capacity of the furnace (100tpd) has been arrived at after lot of iterations so as to run with optimum efficiency, optimum (low) cost, and to give optimum (high) quality of products.

- how the output is easily consumed by customers within a 100km radius thereby avoiding long distance transportation.

- the process is “simple but not easy” and therefore these iterations (in kiln rotation speed, different horizontal velocities and different temperatures at different sections inside the kiln, and consequent learnings) have led to the point where the factory has now become replicable.

4. Optionalities -

- with higher volumes, company can supply to tyre companies (whose requirements are large.

- with RnD efforts leading to rcb content improving from 80-85% to 99%+, the applications can be high-end UV / activated carbon filtration systems, where sales realisation is 4x the current.

- EPR income.

- Carbon credits (company has employed a consultant to conduct carbon accounting under categories of raw material, finished products and process).

- Export of its product.

- Domestic and Overseas expansion.

- Capex incentives being provided by various states to set up this plant (which will flow in over the years) will result in incremental ROCE.

(PS: invested and interested; risks have not been covered in this post).

23 Likes

Great points Vinay. This is helpful and exhaustive about company’s business and manufacturing strength/relevance. Thanks.

2 Likes

A lot of learning to start for someone who has no background on the company. Thank you Vinayji🙏

1 Like

Very well covered Vinay .

My quick short investment thesis :

Right to win :

- Its not what Hi Green do -its how they do .Normally a capex for 100 Tons per day cost around 180-200 cr globally (leaving china ).Hi Green is able to match Chinese cost of 40-50 cr per 100 TPD .Technology / capex cost (which is an edge for the group) .Its zero solid and liquid discharge plant .

2)Huge tailwind of sector in India being truly part of circular economy .

-

Scalability of the proof of concept .Already got approval for 2 more plant and hence 3 x capacity expansion in 2 years .Will be surprised if its not 5 x in 5 years .

-

On Plant and Machinery /capex cost they get subsidy from different states which is between 40-80% of the cost which will help in ROE over years .

-

ROI /ROE is a factor of rotation of capital x net margin % .Here Hi green Core ROE/ROCE will be high as converting waste into finished product (input cost 16-18 per kg but 3 finished products are sold between 25-45 per kg ) .See the enclosed tweet if interested for the concept .

https://x.com/debu_neogi/status/1815222164124999976?s=46

Risk :

1)Regulatory (very complaint now)

2) Getting Bigger customers at scale (can be achievable )

Discl :Hold more than 1% of company hence views may be biased

18 Likes

Debu da , Vinay - I have learnt so so much from you. Debu da i thank you all the time. In last 4 months i have learnt so much about small cap investing in India. All the good blessings for all the goodness you spread will only come back to you in full circle.

6 Likes

@DEBASHISH - For a second, I read it as 1% of your portfolio, then I re-read and realized you hold over 1% of the company! Wishing you all the luck ![]()

1 Like

I think both @DEBASHISH and @sammy11 holds more than 1% in the company.

6 Likes

Indeed fortunate to have 2 esteemed investors share their thoughts on this forum so openly. ![]()

4 Likes