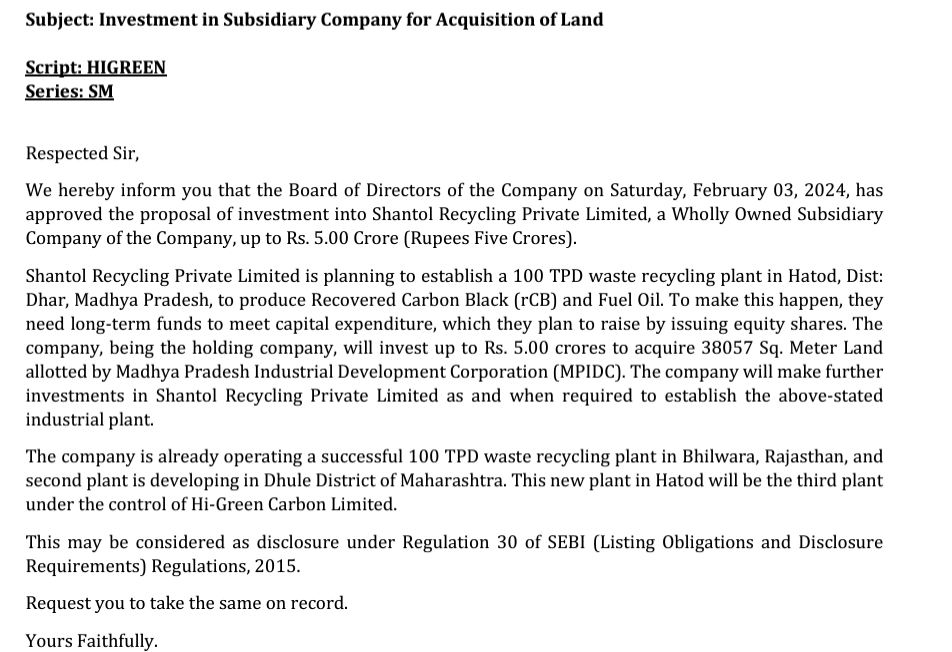

Further to my previous post, the company said it is acquiring land and is gearing up to set up a 3rd plant with 100 TPD capacity. This time in Madhya Pradesh.

4 Likes

Company seems to be good, high TAM, no close national competitors. However, I had three questions-

- Since the company manufacturers Recovered carbon black (rCB), which is essentially a commodity business, how does it compare in price to virgin carbon black ( the product the company is trying to replace) ?

- What are the import risks the company faces and how is it mitigating that >

- As the Capex is only 40-50 crore for a new plant, what is stopping a big player to enter the market and start a backward integrated plant ?

Disc: Not invested, but looking to enter.

3 Likes

Thank you. Do we have any guidance on when can some returns be expected from this investment?

Not a subject matter expert. My answers as below.

- I think the cost of product varies with each grade. As an example, one of the largest manufacturers of virgin carbon black in India (PCBL) N550 sells it around Rs.150/kg, whereas Hi-green recovered carbon black SS550 is available at Rs.35/kg. I guess, at the end, the choice of grade depends on the end user application.

- India imports most of its carbon black from China, US and Korea. I think the key risk whether it is import or local is going to be price, which I think the company has already mentioned as one the risks (Price is the main factor in most cases for client making decision to have their products). I am assuming they are mitigating this risk through good relations with the clients and offering a quality product at competitive price.

- Yes, it is quite possible as increasing environmental regulations, rising awareness about sustainable materials, and the need for circular economy solutions are expected to drive the market further, so are the new players entering the market. However, as the company claims they produce the product using a patented technology which matches or even surpasses the costly virgin carbon black gives me an impression that they have some kind of moat over other unorganized domestic players. Also, the recovered carbon black business is built on a waste management of tires. So if a tire company decides to put a new rCB plant, that may not be more for a backward integration, rather to manage the tire waste and to comply with govt’s EPR policy.

Disc: My views may be biased. Not a buy recommendation.

6 Likes

No idea. The investment is only to buy land for their 3rd plant. I think prior to this, their 2nd plant which is under construction should come on stream and generate returns by mid 2024.

Ok, thank you…

I was just trying to flavor in some predictability in the earnings.

hi,

to add to this, as per the company, to set up a similar plant overseas in USA / Europe will cost 2-2.5x. Their cost of operations and therefore cost of end products would be that much higher, and conversely, their ROE/ROCEs and payback periods would be that much lesser.

Regarding an Indian company setting up this plant, it is very much possible. To some extent, the company currently has the advantage of low cost of plant and machinery, which is developed in house. But whether any other company can also do the same? Yes, its possible. Will they also take 5-7 years to develop the process efficiency? Maybe they may be able to do it faster. We need to monitor this and find answers.

rCB is used as a part substitute in making VCB, which continues to remain a crude derived product. Will it make business sense for a tyre manufacturer to make VCB? We only have Balkrishna Tyre’s case study. None of the other tyre manufacturers have gone into this backward integration.

6 Likes

Hi, thanks for the thread! Very interesting company.

I have two queries if someone could guide:

-

The revenue contribution of the recovered Carbon Black is just 22% whereas Fuel Oil is 46% and Sodium Silicate Glass is 31% (taken from the initial post by @sameernics) whereas the company narrative is just around recovered Carbon Black. Is there some guidance where the revenue proportion of rCB will increase as compared to the rest? If not, is it a cause of worry or deeper inspection?

-

Looking at their Half Yearly Revenue, we see it has remained constant for Sep '23 (33 cr) as compared to Mar '23 (34 cr) and has dropped from Sep '24 (44 cr).

Do we know of any reasons for this, especially since the company says these are commodity products which are easily sellable and their factory is working at a 66% annual capacity utilisation (16558.20 MT/24000 MT) so I am not able to understand if it was demand led or supply led reduction Y-o-Y?

Thanks!

2 Likes

The % contribution of various products is linked to the chemical composition of the tyre.

for eg. Carbon black as a proportion of raw materials is about 20-25% in a tyre, which gets recovered.

Its just the nature of the pyrolysis process.

Even the fuel oil is a recovered oil. Which acts as a substitute for crude oil product used as fuel by their customers.

Sodium silicate is more to do with using the immense heat generated from the process as effectively as possible. The company evaluated several options, including setting up a power plant, before deciding that this is what makes most economic sense to them. There is no issue in availabilty of the raw materials (silica and soda ash), the capex for this plant is very small, and the end product has wide usage and is easily saleable.

Regarding revenue - for now they have just one plant. So I am guessing that the volume they are able to produce would be fairly constant, with normal fluctuations. Any change in numbers would then be driven more by realisations till their new plant comes up in a few months.

11 Likes

Hi green ISCC plus certificate.pdf (1.3 MB)

Hi Green got reputed ISCC certificate from EU -this certifies that Hi Green is sustainable manufacturing company and produce material which are sustainable …so it will get premium price and also get ESG mileage .

Company worth studying in detail .Few pointers :

- Capacity expansion by 3x in 1.5 years with incentive on capex

- From waste ,products are made with zero solid and liquid discharge

- Huge scabality in India with edge in capex cost bcos of technology

Discl: Views may be biased bcos of my holdings

7 Likes

What could be the reason for this downward trajectory?

valuations probably. margins tend to affect by crude price. companies new plant to become operational by end of Q1FY25. mostly market waiting for new plant to operationalize. and result post listing was also flat.

Updates on Capex: Source

HGCL is under-going a capacity expansion project at an estimated cost of Rs.40.41 crore. The proposed plant will be in Dhule, Maharashtra having installed capacity of recycling 100MT of waste tyres/day. The project is expected to commence operations from May/June 2024. The project cost is funded through issue of equity shares, internal accruals, and term loan from bank. Till February 2024, HGCL has incurred ~Rs.30 crore in the project. With 25% of costs yet to be incurred, there exist project implementation and stabilization risk.

8 Likes

2 Likes

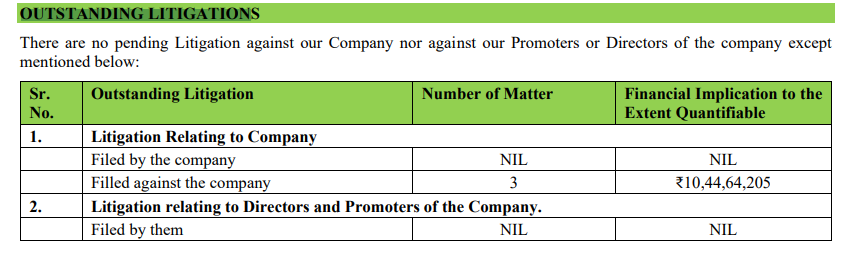

Does anyone have clarity on the Outstanding Income tax demands due with the company.

-

As per the DRHP, ‘the company has filled a response for the outstanding demand of INR 4.1 Crore for AY 2013-14 and the same is under consideration by the department’ - The response was submitted on 21.09.2022.

-

As per the DRHP, the company has made an appeal against the order passed by AO assessing total income at Rs. 6,09,50,000/-, as fictitious loan from RNG Finlease Private Limited is nothing but the devise to bring unaccounted money into books of account and claimed the same as fictitious loan. This is pending adjudication.

2 Likes

@sammy11 do you have any clarity about this issue? Thanks in advance.

Invested in both companies, however as on date, i feel Tinna is a long term hold, where as High Green Carbon is more of a trade and then can be moved to long term portfolio.

Also i think the related party transactions are quite a lot, which i feel should be examined.

i think this patent is also housed in one of the parent entities.

the company had given some explanation in the drhp…which sounded reasonable. there is no further update on this.

My view is to get good returns first step is to get industry tailwind in favour .In that if we can get some competitive edge in a company ,then the probability of getting good returns improves drastically .

My short Top of mind investment thesis for Hi Green :

Industry Tailwind -Higreen truly operates in a circular economy as they get 3 products from waste ,with zero liquid and solid discharge .The industry will shift globally , slowly from 100% Vcb to x % Rcb in slow and steady manner .

Competitive edge /Right to win :

1)Technology / capex cost (which is an edge for the group) incurred is only 40-50 cr for a 100 tones per day plant compared to outside India (leaving china ) at 180-200 cr per 100 tons per day

2)Have got approval for 2 more plants .One in Dhule and another in MP .Both should be operational in a years time .Hence capacity expansion is 3X in 1 year time .

As and when the manufacturing kicks starts ,operating leverage will set in ,lets see

Discl: Views may be biased bcos of my holdings

17 Likes