Hexaware, an Indian IT services company, is doing an IPO. They will open for subscription between Feb 12-14 and list on the bourses on Feb 19.

The Offer

Hexaware is 100% owned by a PE fund, Carlyle, which has $447B (!) of AUMs.

The offer is entirely an OFS of 8750 Cr which would represent a sale of approx 20% of the promoter’s shares in the company. The company has no borrowings.

Business

Hexaware is an IT services business. They claim that “artificial intelligence (“AI”) at its core.”

After having examined their RHP, I conclude that they broadly provide the following five services

- Software Development

- Server Monitoring

- Data Analysis

- BPO - Phone & chat support

- Cloud Migration services

No breakup of revenues by these types of services is provided in the RHP.

Their AI first claims come from three “platforms” that they provide, namely

- RapidX - Seems to be AI code completion with some additional AI stuff sprinkled on.

- Tensai - Server monitoring & test automation with some additional AI stuff sprinkled on as well as stuff like chatbots, knowledge article generators, call summarizations etc

- Amaze - Just seems like a bunch of cloud migration tools with no AI stuff

I am skeptical of their “AI at its core” messaging since efficiency gains from AI should be reflected in profit margins but there has been no significant margin expansion nor any margin differentials relevant to its listed competitors.(See Relevant Financials section)

Relevant Financials

Revenues

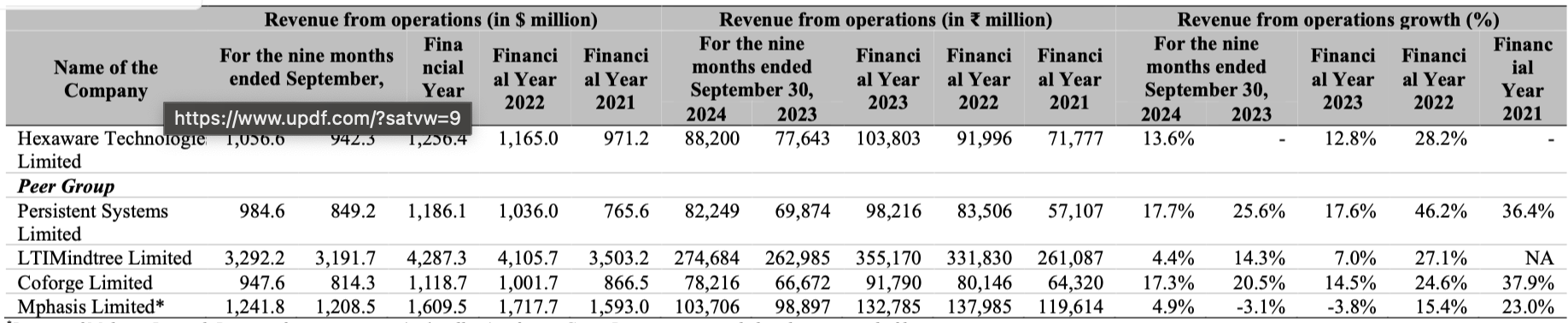

Hexaware has (correctly IMHO) benchmarked itself against Indian IT services companies of similar revenues - namely Persistent, Coforge, Mphasis (LTIMindtree is probably thrown in there to make Hexaware look better ![]() ).

).

Persistent and Coforge are the two biggest performers - not only when compared to IT services companies of similar revenues but compared to all IT services companies, including those larger and smaller than them.

As you can see, on a FY20-FY25 CAGR basis, Persistent and Coforge have the top two CAGR revenue growth rates of 22.7% and 19.2% respectively.

Because of Hexaware’s weird decision to consider CY as their FY its financials can’t be compared directly to companies in the above table compiled by BOBCAPS research.

However, in their comparison against Persistent/Coforge/Mphasis/LTIMindtree we can see that they ended CY22 with similar revenue growth as Coforge and LTIMindtree while Persistent left them all in the dust with their extraordinary growth.

In CY23, they managed to keep up with Coforge while LTIMindtree fell behind and Persistent was again in the lead.

In 9M CY24, they haven’t managed to keep pace with the leaders Coforge and Persistent but they have left behind LTIMindtree and Mphasis who have seen substantial revenue growth slowdowns.

Margins

The margins for all the IT services firm appear to be similar with minor variations. As mentioned earlier, there is no margin expansion from CY21 (when they launched RapidX and Tensai platforms) to CY24.

To me, there is nothing remarkable about margins in the IT services industry and the only differentiator is revenue growth which comes down to existing and new client relationships.

(Side note - No idea why Mphasis is doing so bad though - would be interesting to deep dive into it when I have time)

Valuation

BOBCaps on 1st Jan 2025 wrote a very detailed, informative report on the IT sector. I recommend going through it if you have time. It summarizes the headwinds to the IT sector very well IMHO. Link is below

https://www.barodaetrade.com/Reports/ITServices-SectorReport1Jan25-Research.pdf

To summarize the valuations part

It also includes valuations, summarized below

- They have based valuations on P/E ratio which is reasonable to me as IT services is a mature industry with a long data history of P/E ratios that can be used as baseline.

- They have taken average last 5Y P/E ratio of TCS (the biggest IT services company) less 1 standard deviation (as revenue growth should be slower in the future). The value of this comes to 24.6x.

- They have added premiums and discounts for certain companies based on projections from last 5Y revenues and their subjective judgements of management.

- Persistent and Mphasis get a 20% and 10% premium respectively from BOBCaps, bringing their valuations based on P/E ratios to 29.5x and 27.1x.

If we annualize their 9M CY24 diluted EPS with simple extrapolation, it gives us an EPS of 18.75, a 14% growth from CY23.

Calculating its P/E ratio using upper IPO price band of Rs 708 gives us a current P/E multiple of 37.76.

Therefore

- If we assume Persistent-like 29.5x as its valuation, its fair price is Rs 553.12

- If we assume Coforge-like 27.1x as its valuation, its fair price is Rs 508.12

Risks

-

High P/E Multiple - At the upper band price of Rs 708, its P/E multiple based on estimated CY24 earnings would be 37.76. This is significantly higher than historical median P/E multiples of Indian IT services companies.

-

Trump - Hexaware (like all Indian IT services companies) have a very high dependance on USA for their revenues (73% of their revenue comes from US).

Trump policies such as tariffs on India can lead to margin contraction if they are unable to pass on the tariffs costs fully to their customers. Immigration reform regulation targeting H1B visas can affect their onshore facilities (about 50% of their facilities are onshore) and they have not provided any information about the split between H1B and local employees are their facilities.

(All images sourced from Hexaware’s RHP unless mentioned otherwise in image footnote)

Disc: Not subscribing to IPO, only tracking it for now. Valuation provided is NOT buy/sell advice